Gabelli downgraded Zoetis to Hold from Buy based citing the stock’s valuation. Shares in the animal health company have already advanced more than 20% so far this year.

Gabelli analyst Kevin Kedra stated that Zoetis’ (ZTS) “performance and leadership appear to be fairly reflected in the stock price”. Following 2Q results on Aug. 6, Kedra raised his 2020 EPS estimate “to $3.60 from $3.40 based on an improved outlook for Zoetis’ companion animal business.”

Zoetis’ 2Q earnings of $0.89 per share beat analysts’ estimates of $0.64. Its revenues of $1.55 billion surpassed Street estimates of $1.36 billion. Overall, while revenues remain flat on a year-over-year basis, earnings declined by 2%.

Meanwhile, on Aug. 7, Stifel analyst Jonathan Block raised the stock’s price target to $170 (6.7% upside potential) from $155 and reiterated a Buy rating, saying that Zoetis “continues to be his top pick in the Animal Health industry.” Block noted that “the stock reaction was somewhat muted due to Zoetis’ impressive year-to-date outperformance.”

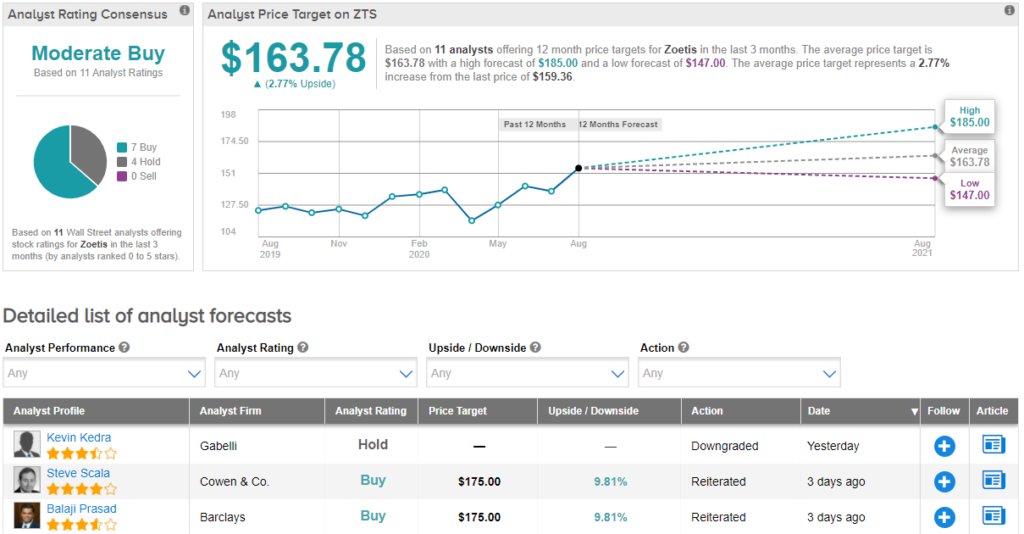

Currently, the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is based on 7 Buys versus 4 Holds. The average price target of $163.78 implies modest upside potential of about 2.8%. (See ZTS stock analysis on TipRanks).

Related News:

Mesoblast Tanks 35% Ahead Of FDA Meeting; Analyst Sees 85% Stock Upside

ASOS: ‘100% Profit Beat’ Cheers RBC Capital On Trading Update

Truist Securities Ramps Up Wayfair’s PT On Improving Profitability