Foot Locker (FL) has reported disappointing first quarter results, causing shares to pullback 6% in Friday’s pre-market trading. First quarter non-GAAP EPS of -$0.67 missed Street estimates by $0.44 while GAAP EPS of -$0.93 fell short of expectations by $0.74.

Notably revenue for the athletic retailer of $1.18B plunged 43% year-over-year and fell $130M below consensus estimates. The company’s gross margin rate decreased to 23% from 33.2% a year ago and the SG&A expense rate increased to 26.9% from 20% in the first quarter of 2019. Foot Locker cited Covid-19 related store closures as behind the significant decline in sales.

“We have taken full advantage of the investments we have made in technology in recent years in order to stay connected with our customers and serve them online, worked aggressively to protect our financial position and flexibility, and taken actions to ensure we are well positioned to drive our business forward,” said Richard Johnson, CEO of Foot Locker.

These actions include borrowing $330 million under the company’s $400 million credit facility; limiting capital expenditures to essential projects and reducing the 2020 capital expenditure forecast by 50% to $138 million; minimizing non-essential spending; and reducing salaries for the CEO and senior executives.

Additionally, the board decided to temporarily suspend the cash dividend beginning with the 2Q payment- and has already suspended its share repurchase program.

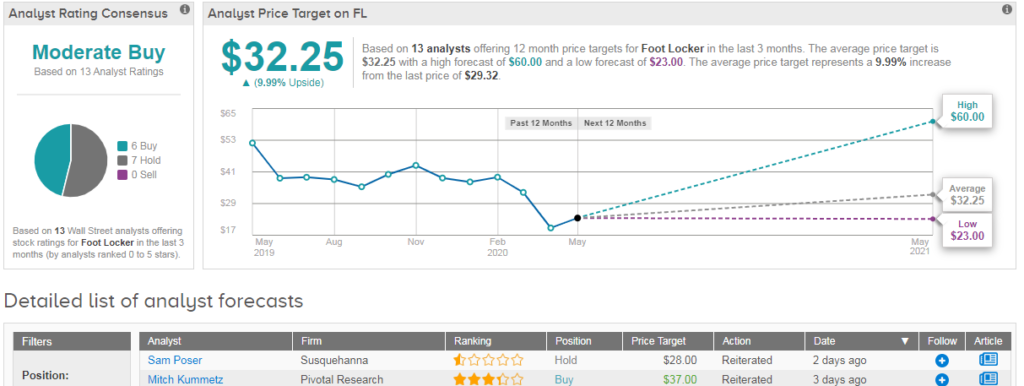

Susquehanna analyst Sam Poser recently reiterated his hold rating on the stock, while ramping up his price target. “We are raising our price target from $20 to $28 due to the cost-cutting initiatives, which we believe will benefit FL over the long-term. Our $28 price target reflects a P/E of 5.7x our FY21 EPS estimate, up from our prior multiple of 4.1x” he explained.

The much lower than average FY2 multiple remains, says Poser, due to uncertainty around both the timing of mall reopenings and the degree to which consumers will return to malls. Although FL’s e-commerce business is expected to improve, FY19 e-commerce sales only represented ~16% total revenue. “It’s unclear if FL’s digital sales will increase rapidly enough to offset weak store traffic” Poser concludes.

Overall the stock shows a Moderate Buy analyst consensus, with 6 buy ratings offset by 7 hold ratings. The average analyst price target stands at $32 (10% upside potential). Shares are trading down 25% on a year-to-date basis. (See FL stock analysis on TipRanks)

Related News:

Nvidia Sinks Despite Stellar Earnings; Top Analyst Says Buy On Any Weakness

Starbucks Regains Almost Two-Thirds Of U.S. Same-Store Sales As Stores Reopen

Shopify Reveals Multiple New Features At Virtual Reunite Event, Stock Now Up 95% YTD