Foghorn Therapeutics (FHTX), a clinical-stage biotech company with its sights set on revolutionizing oncology, surprised with top-and-bottom-line beats for Q3. The company is making significant strides with promising pipeline candidates and a strategic collaboration with pharmaceutical giant Eli Lilly (LLY), leading to the creation of novel oncology medicines. The company presents a high-risk, high-reward option for investors interested in biotech.

Foghorn Progressing with Promising Pipeline

Foghorn Therapeutics is a clinical-stage biotechnology company that aims to create new oncology treatments by correcting abnormal gene expression. Using its Gene Traffic Control platform, Foghorn is developing a new class of medicines that target genetic dependencies within the chromatin regulatory system. The company has entered into a strategic collaboration with Eli Lilly, focusing on systematically studying, identifying, and verifying potential drug targets, resulting in the development of several oncology product candidates.

One promising candidate is FHD-909, a first-in-class oral SMARCA2 selective inhibitor, launching Phase 1 of the trial for SMARCA4 mutated cancers. It aims to target patients with non-small cell lung cancer (NSCLC), a cancer type in which SMARCA4 mutations are common.

Foghorn is also progressing with its Selective CBP and EP300 degrader programs, which showcase significant tumor growth inhibition in mouse xenograft solid tumor models and promising anti-tumor activity in various cancer types. The Selective ARID1B degrader program, targeting several cancer types, including ovarian, endometrial, colorectal, and bladder, is underway.

Foghorn’s Recent Financial Results

The company recently reported results for the third quarter. Revenue of $7.81 million surpassed analysts’ forecasts by $0.8 million. However, the collaboration revenue dropped from $17.5 million in Q3 2023 to $7.8 million in Q3 2024 due to the termination of a collaboration with Merck (MRK). The revenue in Q3 2024 was primarily generated from the ongoing Lilly Collaboration.

The company’s Research and Development expenses slightly decreased from $26.3 million in Q3 2023 to $24.7 million in Q3 2024, primarily due to the impacts of a $3.3 million increase in Lilly partnered programs. General and Administrative expenses also dropped from $8.3 million to $7.0 million, mainly attributed to reduced personnel costs. The net loss increased to $19.1 million in Q3 2024 from $14.3 million in Q3 2023, despite which GAAP earnings per share (EPS) of -$1.18 missed expectations by $0.24.

Foghorn had a solid cash position of $267.4 million as of the quarter’s end. It projects a cash runway extending into 2027, providing a solid foundation for advancing its clinical and preclinical pipeline.

Is FHTX a Buy?

The stock has been on a volatile (beta of 2.76) upward trajectory, climbing roughly 145% in the past year. It trades near the upper end of its 52-week price range of $2.70 – $10.25 and demonstrates ongoing positive price momentum as it trades above all the major moving averages. Its P/S ratio of 17.2x sits well above the Biotechnology industry average of 9.3x, reflecting a mix of investor enthusiasm and a healthy growth rate priced in.

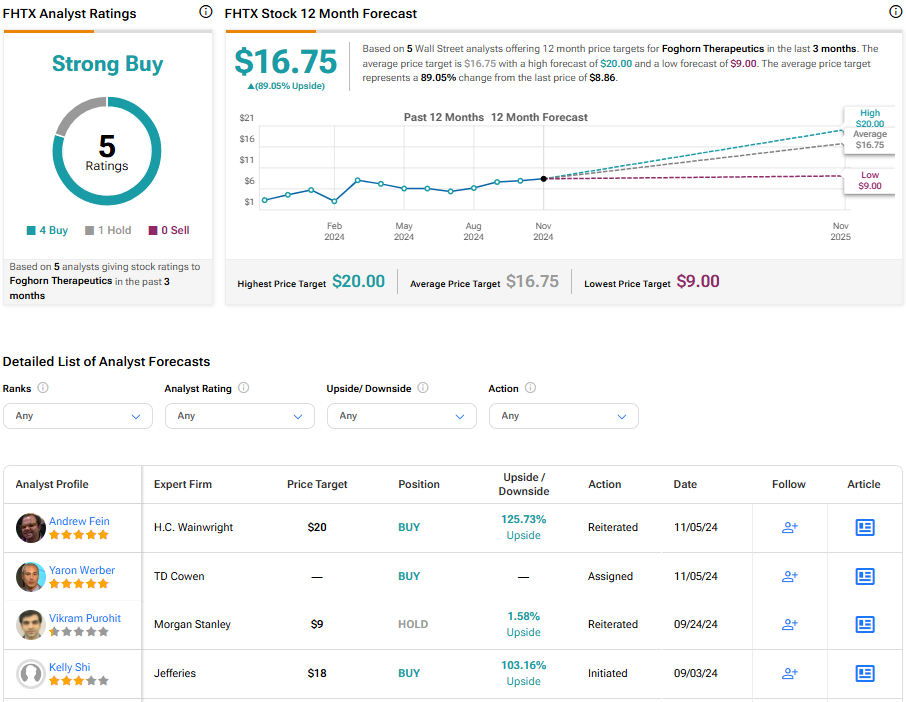

Analysts following the company have been mostly bullish on the stock. Based on five analysts’ recent recommendations, Foghorn Therapeutics is rated a Strong Buy overall. The average price target for FHTX stock is $16.75, representing a potential upside of 89.05% from current levels.

Final Thoughts on Foghorn

Foghorn Therapeutics pipeline suggests a promising future. It has recently surpassed Q3 forecasts for revenue and earnings and boasts a robust financial standing as it navigates through various clinical and preclinical studies. A partnership with Eli Lilly fortifies its progress in this arena. The company’s stock has steadily risen, and analysts project further potential upside. Investors focused on biotech innovation, particularly in oncology, may find this an appealing opportunity.