FactSet Research Systems Inc. reported better-than-expected results in the first quarter (ending Nov. 30, 2020) and reiterated its guidance for fiscal 2021. However, shares of the software company fell 4.1% on Monday.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

FactSet Research’s (FDS) 1Q earnings of $2.88 per share exceeded analysts’ estimates of $2.75 and grew 11.6% year-over-year driven by top-line growth and operating margin expansion. The company’s 1Q revenue increased 5.9% to $388.2 million year-over-year, and topped the consensus estimate of $387.4 million. It was mainly driven by sales of analytics and content and technology solutions.

FactSet CEO Phil Snow said, “We have more conviction in our end markets than we did when we started the fiscal year.” He further said, “Our pipeline remains robust, built on the investments we are making in content and technology. The number and depth of conversations we are having with our largest clients around digital transformation, and how we can help streamline their workflows, position us well as we enter our second quarter.”

As for fiscal 2021, the company continues to expect earnings in the range of $10.75-$11.15 per share, compared to the consensus estimates of $11.04 per share. FactSet also maintained its fiscal 2021 revenue guidance of $1.57 billion-$1.585 billion. (See FDS stock analysis on TipRanks)

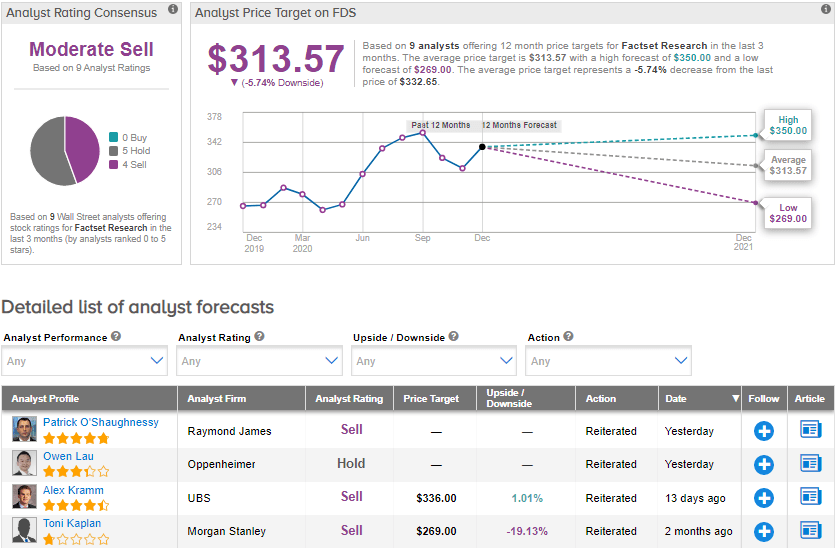

On Dec. 21, Raymond James analyst Patrick O’Shaughnessy maintained a Sell rating on the stock, following “lukewarm” quarter. He said, “FactSet does believe its sales momentum is improving, and management is less cautious about the pipeline today than it had been in F4Q20, but limited revenue visibility and an expense ramp throughout the remainder of FY21 mean no change in management’s full-year guidance.”

Meanwhile, the Street has a cautiously bearish outlook on the stock. The Moderate Sell analyst consensus is based on 5 Holds and 4 Sells. The average price target stands at $313.57 and implies downside potential of about 5.7% to current levels. Shares have gained by 24% year-to-date.

Related News:

Calavo Sinks 16% As 1Q Sales Outlook Lags Street Estimates

Progressive’s Profit Soars 142% in November; Analyst Lifts PT

Shell Updates Q4 Outlook and Writes Down Assets