In recent years, a few companies have exploded onto the scene, like Robin Hood (HOOD). As a new generation of investors emerged, the glossy and gamified platform for trading and investing without paying the previous commission levels excited plenty of new users. Of course, it’s not been a smooth road, with plenty of volatility for the share price. Still, I see an enormous opportunity for the company going forward, as management aims to target sectors such as sports betting. Even after a rally that has seen shares rise by over 225%, I’m incredibly bullish on the company’s prospects.

Catering for a New Type of Investor

What makes me most excited about the company’s future is the alignment to the latest investor style and the market dynamics in general. Gone are the days of dealing with financial advisors by telephone, checking balances once a year, and monitoring news in today’s paper. This generation of investors are able to trade complex and volatile instruments on glossy interfaces and with to-the-minute information from a diverse range of online sources. The recent meme stock influence and widespread distrust of large institutions from online forums have given investors new influence, with communities now able to move the needle of share prices in ways previously considered impossible.

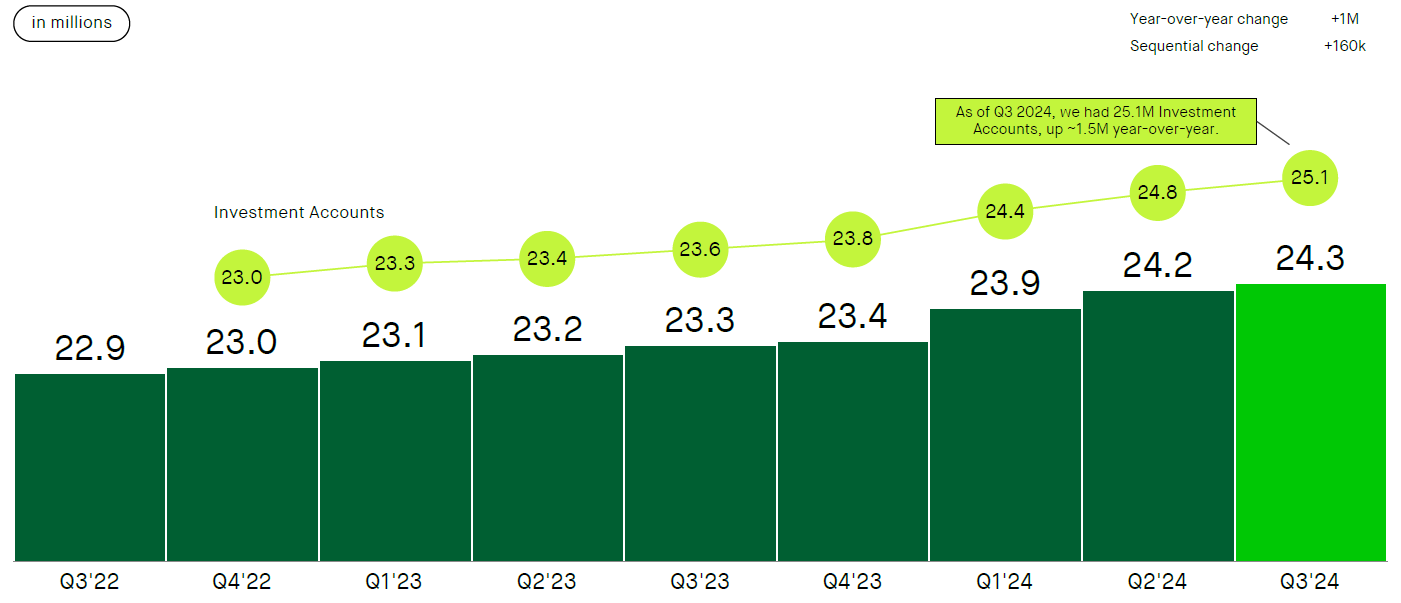

RobinHood now hosts a whopping 25.1 million accounts. In addition to standard investing and trading accounts, the platform now supports cryptocurrencies, retirement accounts, and access to IPOs.

Entering Sports and Events Betting

The company has significant opportunities to expand, especially with the increasing legalization of sports betting. My bullish position has been enhanced after CEO Vlad Tenev recently hinted at this potential move. The platform’s user-friendly interface positions it well to enter the market without the extensive payment and regulatory infrastructure that other companies require. This first-mover advantage could attract users and integrate sports betting with investing services. With the market poised for growth, established players like DraftKings (DKNG) also want to expand as regulations evolve.

But it’s not just sports that the company has identified as a potential growth area. The recent U.S. election was listed as an event that app users could speculate on, setting the stage for further “event contracts” that users can trade on in a peer-to-peer marketplace. Such markets are well known in other countries, with many speculating about the outcome of elections, TV shows, and other events. I feel that this new cross-promotion offering aligns well with the platform’s style of investors looking for opportunities and the latest event to build a thesis on.

I’d also suggest that the market is not yet pricing in the monetization potential of building a database of live investor opinions and intentions. Polling data and general consumer information is big business for marketing and user research firms, and RobinHood could quickly become an enormous player in the market. Further, personalized betting promotions, incentives, and features could easily push the lifetime value of customers even higher over the coming years.

Robust Financials to Build On

I’m bullish on this latest hint from management, but it needs a resilient balance sheet to enable it. I’m encouraged to see just that from the company’s latest earnings. The strategy clearly works with a 36% revenue increase over the last year, now hitting $637 million. Net deposits from users total over $10 billion, providing impressive signs that users are loyal to the platform and remain engaged with new offerings and features. With an average asset of $6,300 per customer under custody (AUC), there is a genuine opportunity to be the ‘everything platform for finance’, capturing users for the rest of their financial lives and subsequently taking enormous market share from the traditional financial institutions and pension providers.

I’m also encouraged to see the company’s balance sheet steadily improving, with $10.1 billion in cash roughly offsetting the risk from the $11 billion of debt held. History has shown that when a profitable company can build scale with a robust balance sheet behind it, there can be enormous potential for investors.

I’m slightly surprised to see Wall Street analysts so cautious about this one. Admittedly, it’s been a controversial stock at times and hasn’t been easy to predict since the IPO, but there is clearly a lot more to like about the company than in recent years. Analysts have an average price target of $41.40.

Assessing RobinHood’s Catalysts

I’m increasingly bullish on the opportunities for the company, but of course, there are a few risks I’m keeping an eye on. After a 250% rally, the P/E ratio of the firm is now at a premium of 71.0 times. If management slips up, as the GameStop (GME) debacle has shown us can happen, investors could easily see another steep sell-off. However, by diversifying the product offering into more stable revenues, especially if sports betting can enter the mix, I feel the company is moving towards more predictable growth paths.

The chief concern I have is regulation. The incoming administration has promised a ‘remaking’ of many major institutions, and I’d be surprised if the financial world was spared from some degree of shake-up. I’d think this may help the relative newcomers to the sector, but uncertainty helps nobody. If aggressive changes are proposed to how payment for order flow (PFOF) or the market functions in general, many fintech stocks could see near-term or sustained disruption. There are also potential regulatory hurdles to consider if sports betting becomes a target, with enormous levels of competition and potential legal challenges from existing giants in these areas.

One to Watch

Overall, I see RobinHood as a huge winner over the next few years. There is likely to be a lot of change in the market as consumer trends evolve, but activity is money in this market, and the newest generation of investors is as active as we’ve seen in recent memory. If management can continue to build upon the firm’s robust fundamentals and build a presence in new markets, I think there are tremendous opportunities for the company and for investors ahead. There are plenty of risks, but with all the company’s metrics moving in the right direction and building a loyal user base in such a huge potential market, I see this as one to watch closely over the coming years.