Expedia (EXPE) stock surged 17.3% on Friday and hit a new 52-week high of $205.12. This rise came after the company’s strong fourth-quarter results that beat Wall Street estimates, thanks to high travel demand. However, opinions of Top-rated analysts on EXPE stock remain divided. While some analysts are optimistic about strong bookings growth and reinstatement of its dividend, others remain cautious over potential macro challenges.

Following the earnings release, seven Top analysts recommend buying Expedia stock, while 10 have reiterated a Hold rating. It is worth noting that most of these analysts have raised their price target for the stock.

A Quick Look at EXPE’s Q4 Results

In Q4 FY24, Expedia’s revenue rose 10% year-over-year to $3.1 billion, driven by a 21% jump in the B2B (business-to-business) segment’s revenue and a 25% increase in advertising income. Also, global active membership in the loyalty program grew by 7% year-over-year, and gross bookings jumped 13%. Moreover, Expedia saw significant growth in Europe and the Asia Pacific regions, which signals a recovery in international travel.

Looking ahead, Expedia expects gross bookings growth between 4% and 6%, while revenue growth is projected at 4% to 6%. Nevertheless, Expedia anticipates a slowdown in bookings and revenue growth in Q1 FY25, citing foreign exchange (FX) pressures.

Wall Street’s Mixed Views on Expedia

Wall Street remains divided on Expedia after its Q4 results. Among the bullish analysts, B.Riley Financial analyst Naved Khan raised the price target to $235 (16.1% upside) from $220. The analyst said the company’s Q4 results were driven by “broad-based strength” in the business. Further, Khan believes Expedia is benefiting from growing demand and effective execution.

Similarly, a five-star analyst, Justin Post from Bank of America Securities, boosted the price target to $250 (23.5% upside) from $221, citing improved brand execution under new leadership. In addition, the analyst expects revenue and EBITDA (earnings before interest taxes, depreciation, and amortization) to continue to outperform estimates in 2025. Given the recovery in the B2C (business-to-consumer) unit and signs of ongoing improvement in U.S. travel, the analyst is hopeful about potential gains in 2025.

Meanwhile, a five-star analyst, Nicholas Jones, CFA, from JMP Securities, kept a Hold rating on EXPE. He acknowledged the strong Q4 results but noted that full-year guidance is slightly below expectations. Going ahead, Jones expects that strong momentum in travel demand could boost revenue growth, stabilize U.S. market share, and improve adjusted EBITDA margins.

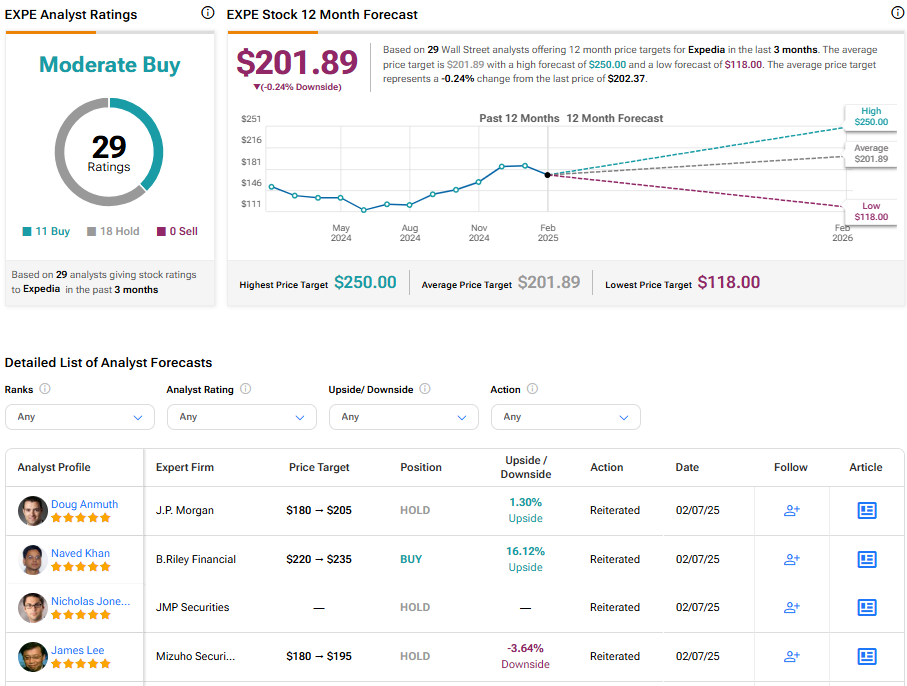

Is EXPE a Buy or Sell?

Turning to Wall Street, EXPE stock has a Moderate Buy consensus rating based on 11 Buys and 18 Holds assigned in the last three months. At $201.89, the average Expedia price target implies a 0.24% downside potential.