Activist investor Elliott Investment Management is miffed by Southwest Airlines’ (LUV) revenue-boosting strategy. Elliott explicitly expressed its displeasure in an open letter following LUV’s Q2 FY24 results yesterday and strategy announcement. The activist investor believes that LUV’s revenue-enhancing initiatives, such as offering assigned seats and seats with extra legroom and adding overnight flights, are not good enough to boost revenue.

Elliot Unconvinced With LUV’s Strategies

According to LUV’s research, about 80% of existing customers and 86% of potential customers preferred assigned seating and called the open seating option a big factor in driving customers away. Elliott thinks that LUV was very late in undertaking the research and in implementing the assigned seat option.

The activist investor’s letter further stated that these policies are framed by the same management team that has been repeatedly unsuccessful in improving the air carrier’s performance and operational results. Furthermore, Elliott contends that the airline needed a more drastic change of leadership to navigate through the current woes.

Interestingly, Elliot snapped up about a $2 billion stake in Southwest in June, with an aim to bring major changes to improve its financial and stock price performance. It is pushing for a massive overhaul of Southwest Airlines’ board. Interestingly, the board adopted a “Poison Pill” to prohibit Elliott from taking a more than 12.5% stake in the carrier. Meanwhile, Elliott Management has not laid out specific measures it hopes to take to revive Southwest’s fortunes.

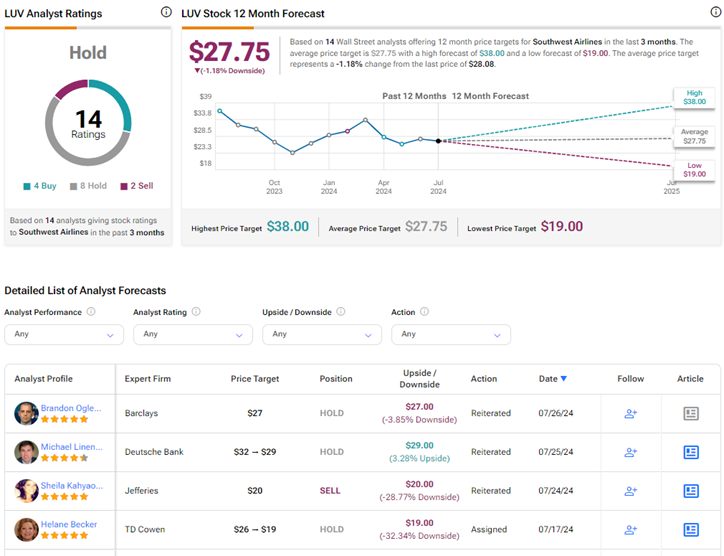

Is Southwest a Good Investment?

Analysts prefer remaining on the sidelines on LUV stock. On TipRanks, LUV has a Hold consensus rating based on four Buys, eight Holds, and two Sell ratings. The average Southwest Airlines price target of $27.75 implies 1.2% downside potential from current levels.