When online file storage solution Dropbox (NASDAQ:DBX) posted its earnings, things were looking pretty good. It was a matter of beats all around. That should have been a winning recipe for investors, but instead, they spewed the end product from their mouths and ran for the hills, taking over 20% of Dropbox’s market cap with them at one point.

Admittedly, the beats Dropbox posted weren’t amazing, but they were there. Earnings per share came in at $0.50 per share, ahead of $0.48 per share analysts were looking for. Revenue fared a little better, coming in at $635 million against analyst projections of $631.68 million. Revenue also beat the fourth quarter of 2022’s figures by 6%. However, annual recurring revenue (ARR) came in at $2.523 billion, up just 0.3% against 2022’s fourth quarter. The beats were present, if somewhat muted, but the big problem seemed to be a slowdown in overall growth rates.

More Competition

Dropbox may be seeing its growth waning, though that’s not too great a surprise. Growth eventually slows for any company, especially one that needs to figure out its next move. It doesn’t help that Dropbox is starting to see more competition emerge; just recently, Internxt Cloud Storage took to the web with a President’s Day special, packing in two terabytes of storage and some high-end privacy protection for a one-time cost of $149.97. Storage goes up from there, and conversely, so do Dropbox’s troubles by extension.

Is Dropbox a Buy, Sell or Hold?

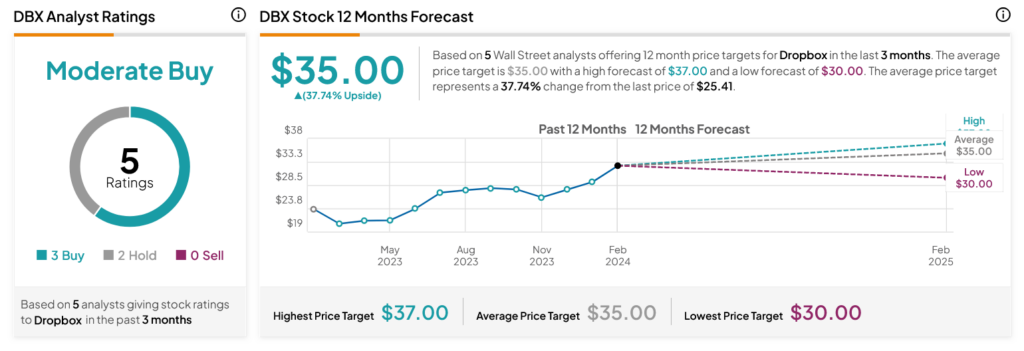

Turning to Wall Street, analysts have a Moderate Buy consensus rating on DBX stock based on three Buys and two Holds assigned in the past three months, as indicated by the graphic below. After a 22.36% rally in its share price over the past year, the average DBX price target of $35 per share implies 37.74% upside potential.

Questions or Comments about the article? Write to editor@tipranks.com