The Q4 2024 earnings report for Apple (NASDAQ:AAPL) came and went late last month, leaving some disappointment in its wake. Though the company beat both top- and bottom-line estimates on its way to setting new revenue and EPS records of $124.3 billion and $2.40, respectively, the market was not thrilled by slowing iPhone sales and weakening China numbers.

Shares have been dropping over the past week–and are down some 4% since the numbers were released–as these concerns are giving rise to the argument that the company stock (trading at 28x FY 2025 EPS) is overvalued.

Nothing could be farther from the truth, says the top investor known by the pseudonym DM Martins Research, who sits in the top 1% of TipRanks’ stock pros.

“Despite bearish views, I believe Apple remains a compelling buy-and-hold stock for long-term investors, even at its current high price,” explains the 5-star investor.

DM acknowledges a number of arguments against Apple shares, and is happy to poke holes in them. For instance, the slower iPhone sales do not cause too much concern for the investor, who notes that historically speaking these sales cycles always tend to attract a fair amount of skepticism.

“I think that trying to time entries and exits into and out of the stock based on the success of the current-year phone model is too speculative and rarely leads to a whole lot of alpha being generated,” the investor adds.

When it comes to China, the company has done a nice job diversifying its supply chain, explains DM. Whereas in 2020 roughly half of Apple’s suppliers were in China, that number has decreased to some 33%.

On the demand side, however, there is plenty of instability with Greater China, which the investor admits is the most volatile region in the company’s portfolio. Still, despite the volatility, growth from Greater China has been consistent with the total company’s since 2019, leading DM to conclude that it is “probably not being a very important driver of the stock’s value.”

As for the valuation, this is a recurring issue with Apple. In other words, this is a feature, not a bug.

“Apple has always traded at rich valuations, at least in the Tim Cook era, which has not prevented the stock from producing 185% cumulative returns in the past 5 years and gains of 630% in the past decade,” notes DM, adding that “I would warn investors against trusting their spreadsheets blindly.”

Instead, DM is banking on Apple’s brand loyalty, its compelling services segment, and strong balance sheet, among other positivies, to continue delivering growth in the year ahead. The investor is therefore rating Apple a Buy. (To watch DM Martins Research’s track record, click here)

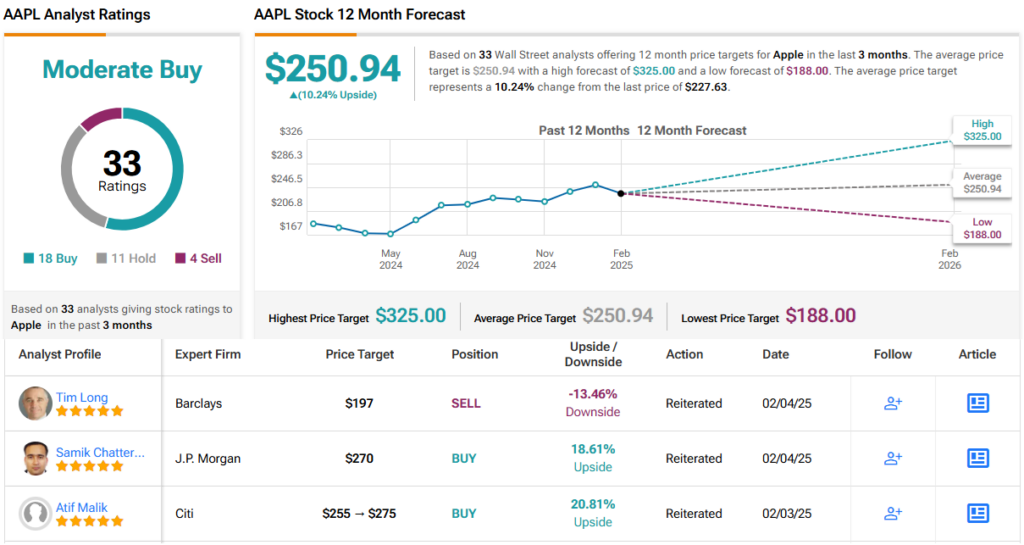

Wall Street by-and-large tends to agree with this conclusion. With 18 Buy, 11 Hold, and 4 Sell ratings, Apple enjoys a Moderate Buy consensus rating. Its 12-month average price target of $250.94 would translate into gains of roughly 10% in the coming year. (See AAPL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com