Advanced Micro Devices (NASDAQ:AMD) has faced a series of downgrades on Wall Street recently, as analysts increasingly believe the company is unlikely to make a significant impact in the AI chip market or capture a meaningful share of segment leader Nvidia’s dominance.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

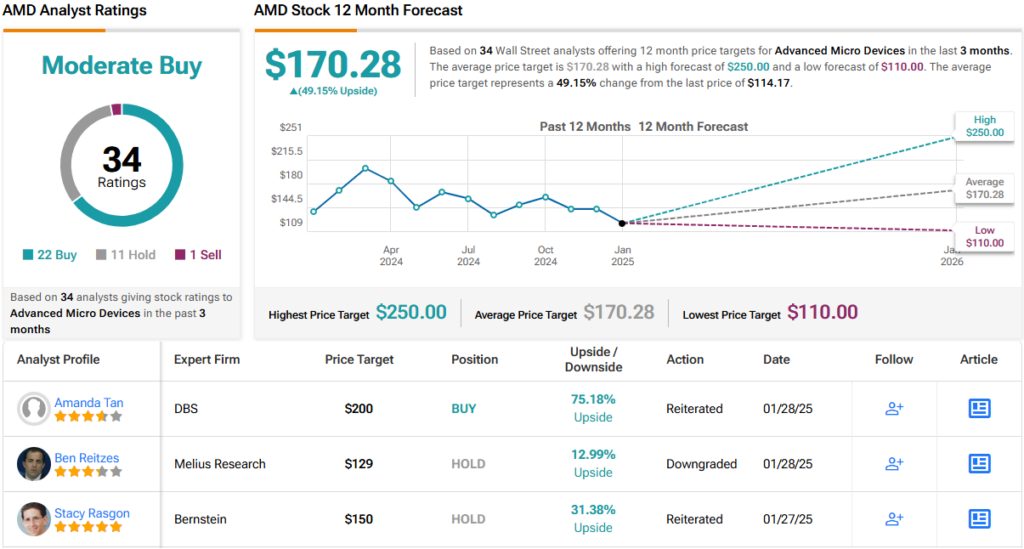

Now another analyst has turned from bull to skeptic. Melius Research’s Ben Reitzes has downgraded his AMD rating from Buy to Hold (i.e., Neutral), while also cutting his price target from $160 to $129. (To watch Reitzes’ track record, click here)

But is this just another case of dampened GPU prospects? Not exactly. While Nvidia’s shadow certainly plays a role, Reitzes had already tempered his GPU outlook earlier this year.

“We are now more cautious on x86 server and PC as well over the long-term for AMD,” Reitzes explained. “The reason? We think Nvidia is going to increasingly ‘come for them’ in both markets with their Arm-based CPUs that are optimized for ‘accelerated PCs.’”

Additionally, the analyst is becoming more worried that custom CPUs and Nvidia CPUs will “cannibalize even more” of the x86 server market in the long run, despite AMD’s current chip, Turin, performing well.

Reitzes says it makes sense for Nvidia to “accelerate its disruption” of the PC and even x86 server markets. PCs, in particular, will increasingly rely on GPUs to securely run AI applications at the edge. Which begs an obvious question: why not handle both the CPU and GPU? With the rise of DeepSeek and more affordable models that can run on PCs, the demand for AI-optimized PCs is likely to grow. This creates a need for more integrated Nvidia-based solutions capable of running AI apps more efficiently. Servers are already being overtaken by Nvidia and custom accelerators, driving fleet consolidation.

“If you are Nvidia,” says Reitzes, “why not accelerate these pushes and make it so the AMD and Intel CPU profit pools get hit so they can’t win in data center GPUs?”

It’s not only Nvidia that is getting in the way of AMD’s success. Although 2025 is expected to be a strong growth year for server CPUs, Reitzes is convinced that major cloud providers will adopt custom CPUs more and more over the long term, similar to AWS’s Graviton. AMD is also facing rising competition in the server CPU segment from new players, with even Qualcomm setting its sights on the market.

“While AMD is likely seeing upside to traditional server CPU sales with its next-generation chip Turin’ right now, the investment community is likely to grow increasingly concerned that this market will be threatened beyond 2025,” Reitzes said on the matter.

Turning now to the rest of the Street, 10 other analysts join Reitzes in taking a neutral stance on AMD. However, with 22 Buy ratings and just 1 Sell, the stock retains a Moderate Buy consensus rating. The average price target remains optimistic at $170.28, suggesting a potential one-year upside of 49%. (See AMD stock forecast)

To find good ideas for AI stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.