Intel (NASDAQ:INTC) has seen its newsflow go into overdrive recently. A report from industry blog SemiAccurate speculates that Elon Musk might be a potential M&A contender, while a Bloomberg article suggests government officials have recently considered the possibility of an Intel-GlobalFoundries merger.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Intel stock, which has been on a long losing streak, has reacted positively to these rumors with the shares now showing year-to-date gains of ~10%.

But don’t get too excited about the prospect one of these rumors will turn into something concrete, says Bernstein’s Stacy Rasgon, an analyst ranked in the top 2% of Wall Street stock experts.

“We aren’t holding our breath for either of these,” said the 5-star analyst on the matter.

Regarding the former, while Rasgon doesn’t question SemiAccurate’s sourcing he is “somewhat skeptical of the viability.” As for the latter, Bloomberg notes that the Intel/GlobalFoundries discussions never progressed beyond a “thought experiment.” This makes sense, given that GlobalFoundries lacks the cash and market cap to pursue such a deal, remains approximately 80% owned by Abu Dhabi, and exited the leading-edge semiconductor space years ago.

These stories are further evidence of the swirling speculation around Intel in recent months, and come off the back of reports the board has been hiring advisors to explore strategic options, rumors of a Qualcomm merger, and the abrupt departure of CEO Pat Gelsinger.

There aren’t really any simple solutions to Intel’s predicament. Rasgon expects ongoing efforts like cost-cutting measures and “portfolio rationalizations” to continue as planned. However, the key challenge for whoever steps into the CEO role will likely be determining the future of Intel’s fabs, as all other strategic decisions hinge on that.

Despite the issues, Rasgon thinks Intel isn’t desperate yet – cash reserves look stable for now, thanks to capex and opex cuts, the dividend suspension, government funding, and private equity injections via SCIP deals in Arizona and Ireland. The company also appears confident in its process roadmap, with optimism around 18A progress at CES and “supposedly increasing customer interest” in its foundry services.

“Given all of this,” says Rasgon, “we wonder why they need to consider any drastic options at this point except to respond to the horrible share price performance seen over the last several years (which, while potentially welcome to some, might seem a little short-sighted if there really is light at the end of the tunnel).”

Yet, this makes Rasgon wonder if the recent flurry of news and Gelsinger’s sudden removal are signs that things are “worse than we think they are.”

As for what investors should do with the stock, Rasgon actually admits that he doesn’t really know.

“It’s perhaps a bit of a cop-out but at this point we continue to advocate avoidance,” the analyst summed up.

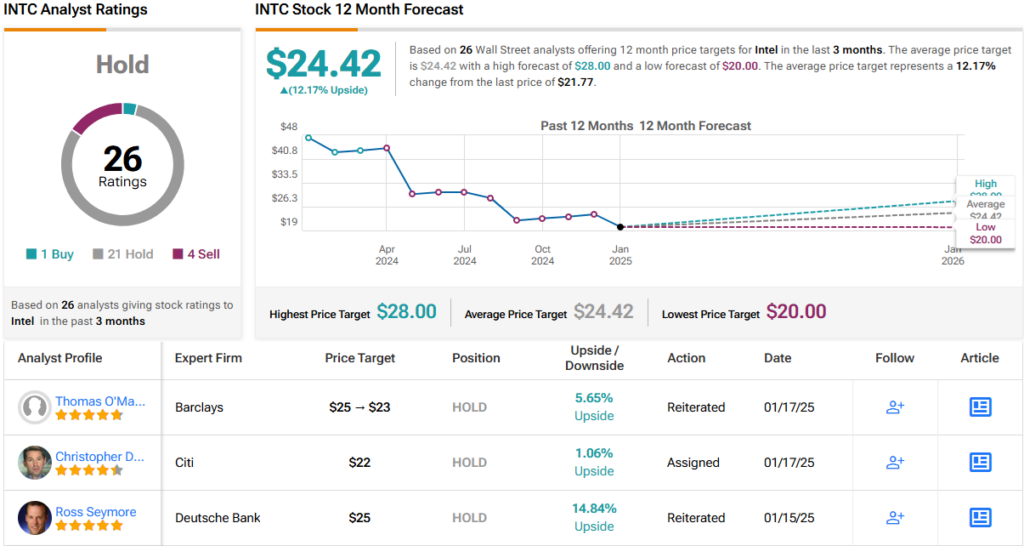

Accordingly, Rasgon assigns a Market Perform (i.e., Neutral) rating for Intel shares along with a $25 price target, suggesting 14% from current levels. (To watch Rasgon’s track record, click here)

Like Rasgon, most analysts think the sidelines are the place to be right now. Based on a mix of 21 Holds, 4 Sells and a lone Buy, the consensus views this stock as a Hold. The average price target stands at $24.42, implying 12% gains are in the cards for the coming year. (See INTC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.