Is it finally time for the bears to come out of hibernation for Nvidia (NASDAQ:NVDA)? It’s been almost nothing but upside for the semi giant over the past year, with the stock powering ahead, riding the AI trend at full tilt as the company’s best-in-class chips have sent its sales and profit profile stratospheric.

However, when does the rally become unsustainable? Just about now appears to be the conclusion reached by Barclays credits research analyst Sandeep Gupta, particularly in light of the current state of Nvidia’s bonds.

“While we acknowledge that demand for Nvidia’s advanced GPUs remains unabated, we are taking a view on the long-term sustainability of this demand as well as how the market is pricing this anticipated growth in NVDA bond spreads,” the analyst said. “NVDA bonds are some of the tightest trading in the market, trading tighter than AAA/AA+ rated Microsoft/Apple, leaving little room for further tightening.”

The thing is, while Apple and Microsoft have storied histories that offer proof of ongoing success, Nvidia’s AI tech and demand curve “still needs to be proven beyond doubt.”

Moreover, both those market leading tech giants have asserted their dominance in their respective segments, while Nvidia has shown itself to be the AI leader so far, it is set to face growing competition from several sources. One being hyperscalers’ own silicon endeavors and the other being other chip makers, Namely AMD and possibly Intel too.

Additionally, Gupta also thinks the demand for AI chips is expected to stabilize once the initial training phase is finished. During the inference stage, less computational power will be necessary compared to training. This could lead to high-powered PCs and phones being sufficient for local inference, thereby “reducing the need for growing GPU plants.”

There is also a concern about additional export restrictions to China, which could diminish the usefulness of NVDA’s lower-power product in comparison to the gaming GPUs, thereby creating “substitution risk.” This risk, says Gupta, is already taking place.

As such, based on the above, Gupta thinks “risk to NVDA bonds is to the downside.” To this end, the analyst initiated coverage on Nvidia with an Underweight (i.e., Sell) rating, recommending selling NVDA 3.5% 2050s (54bp, $82) outright or even just swapping and buying AMD 4.393% 2050s (71bp, $93).

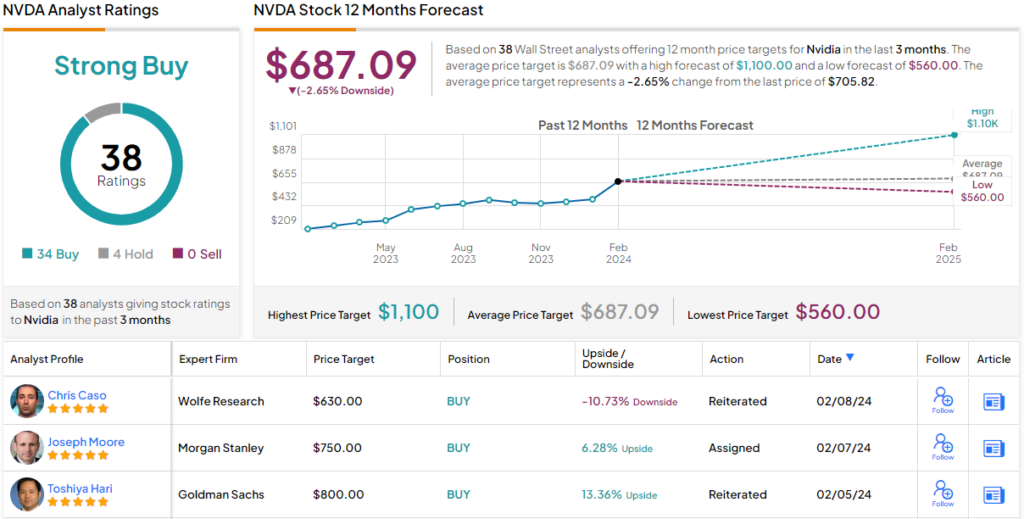

When it comes to shares, however, there are no other Nvidia bears right now. The consensus breakdown reveals a mix of 34 Buys vs. 4 Holds, indicating a Strong Buy consensus rating for the stock. (See Nvidia stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.