Docusign, Inc. (DOCU), one of the world’s largest electronic signature solutions providers, seems attractively valued amid its AI push, which aims to revitalize its revenue growth. Despite a 54% gain in the past 12 months, Docusign stock is still trading at a 70% discount to the highs of over $300 registered in late 2021.

Based on the recent success of DocuSign’s Intelligent Agreement Management platform, which was launched in April 2024 by bringing several unique products such as e-signature, contract lifecycle management, and DocuSign Maestro to a single platform, the company seems to be headed in the right direction to dominate the cloud agreement management industry in the long run. I am bullish on Docusign, as the current valuation offers an attractive entry point.

DocuSign’s Comeback is Centered on AI

One key factor behind my bullish stance on Docusign is how the company has aggressively integrated AI features into its existing products while launching new products to capture new markets. These new features include agreement summarization, AI-assisted data extraction, risk assessment, and AI-powered agreement reviewing.

According to Docusign CEO Allan Thygesen, these AI-powered contract management features have helped some enterprise-level customers reduce the duration of their contracting cycles by a staggering 75%.

Encouragingly, DocuSign’s AI investments are already yielding attractive results. For instance, in Q4, the company reported a 9% YoY growth in revenue, an 11% YoY increase in billings, and a 200-basis point quarterly improvement in dollar net retention rate to 101%.

After growing its customer base by 10% YoY, Docusign ended the quarter with almost 1.7 million customers, suggesting that its AI-powered products attract new customers while retaining existing ones. In the Q3 FY2025, IAM deals grew more than 1,000% compared to the previous quarter, which is a testament to how customers are aggressively embracing AI-powered contract management solutions the company offers.

DocuSign’s Impressive Diversification Efforts

My bullish stance on Docusign is further strengthened by the revenue and product diversification benefits Docusign enjoys due to the rapid growth of the AI-powered IAM product suite. First, the growth of the IAM platform has enabled Docusign to enjoy a high-margin SaaS revenue stream, which positively impacts the business’s operating margins. In Q4, DocuSign’s operating margin increased to 29% from just 25% in the corresponding quarter last year, highlighting this positive impact.

Second, the new product suite has created upsell opportunities for the company, paving the way for higher total contract values in the long run as some of DocuSign’s e-signature customers eventually embrace contract automation products.

The IAM platform has also helped DocuSign attract customers from new business sectors such as finance, healthcare, and legal, expanding the company’s presence across highly regulated industries. Historically, the company has failed to replicate the success it enjoyed in the HR and supply chain automation industries in highly regulated industries. Still, the tide seems to be turning in favor of DocuSign today, thanks to the capabilities of the IAM platform.

AI Success Primes DocuSign for Big Gains

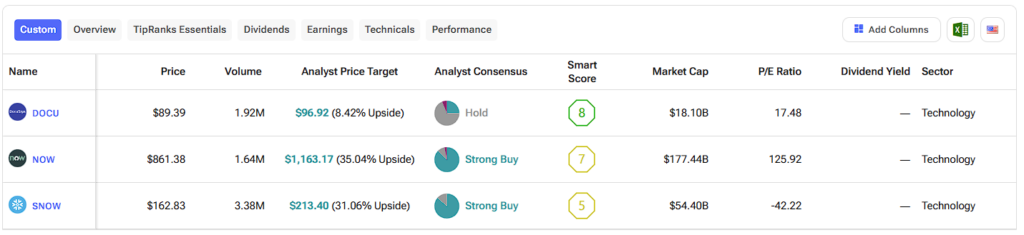

In addition, DocuSign’s early success in AI integration positions the company to enjoy an expansion in market valuation multiples in the long term. So far, DocuSign has been valued as a pure-play e-signature solutions provider, evident from the current forward P/E multiple of 25.

In contrast, enterprise software companies that generate the most revenue from AI-integrated products are valued at lofty valuation multiples. For example, ServiceNow, Inc. (NOW) is valued at a forward P/E of 52, and Snowflake Inc. (SNOW) is valued at a forward P/E of 142. Although it would not be reasonable to expect Docusign stock to trade at similar valuation multiples in the foreseeable future, AI success will lead to a meaningful multiple expansion in the long run.

In addition, the success of the IAM platform will also increase customer stickiness in the long term, as contract management products are much more difficult to replace than standalone e-signature products.

Is DocuSign a Buy, Hold, or Sell?

DocuSign’s AI efforts have not gone unnoticed among Wall Street analysts. Last week, William Blair analysts upgraded DocuSign, citing the momentum behind the IAM platform and the potential of these AI-powered features to revive revenue growth back into double digits.

According to William Blair analysts, the growth of the IAM platform will allow the company to successfully diversify beyond its core e-signature business, opening new doors to growth. Citi analysts also boosted their DocuSign price target after digesting the recent earnings report, citing that an acceleration in billings growth is likely in the current fiscal year.

Based on the ratings of 16 Wall Street analysts, the average DocuSign price target is $96.92 per share, which implies an upside of 8.4% from the current market price.

Ultimately, I think Docusign is not currently valued as an AI-first enterprise software business, which leaves ample room for capital gains in the next few years as AI-related revenue starts accounting for the lion’s share of total revenue.

Signing Off on Bullish Sentiment Fueled by Valuation

DocuSign stock has surged in the past 12 months but remains far from the highs seen a few years ago. The company is aggressively pursuing a future as an AI-first business, and the recent financial performance suggests this is the right strategic move for the long term. The impressive growth of the IAM platform has well-positioned the company to enjoy several diversification benefits, and I believe the company’s current valuation fails to accurately represent DocuSign’s potential to emerge as a large-scale AI-first enterprise software solutions business.