Disney Stock Still Holding Strong, Trading Volume Exploding

Last Updated 10:50AM EST

DIS is still maintaining its strength today as traders digest its earnings report. The stock is up 7%, similar to its action in after-hours trading yesterday. However, at one point today, the stock was up 9.64% when it hit an intra-day high of $123.27 within the first few minutes of trading. Trading volume is also coming in hot, as it has already reached 23.8 million compared to the average daily volume of 11.8 million.

Original Post

After market close today, Disney (DIS) reported its Fiscal Q3 earnings results along with its results for the past nine months. The company beat both earnings and revenue estimates for the quarter, and it also beat Disney+ subscriber growth expectations. Shares are up almost 7% in after-hours trading.

Here are the key highlights:

- Non-GAAP EPS came in at $1.09, beating the consensus estimate of $0.98 and growing 36.3% compared to Q1. Nine-month adjusted EPS grew to $3.22 from $1.91 in the same period last year.

- Revenue of $21.5 billion beat expectations by $490 million; it grew over 26% year-over-year. Nine-month revenue grew 28%.

- Disney will raise its Disney+ prices by 38% to $10.99/month starting in December. An ad-supported version will be released at the current non-ad pricing ($7.99/month).

- 14 million Disney+ subscribers were added in Fiscal Q3, beating estimates by 5.1 million, bringing total subscribers across all of Disney’s platforms to 221 million.

- Domestic paid subscribers to Disney+ brought in $6.27 per month on average, down from $6.62 due to more subscribers opting for multi-product offerings. This was somewhat offset by an increase in retail pricing.

Overall, the earnings results look promising for Disney, as it handily beat analyst estimates. Also, while domestic Disney+ monthly revenue per subscriber has come down, international Disney+ monthly revenue per subscriber increased to $6.31 from $5.52 last year.

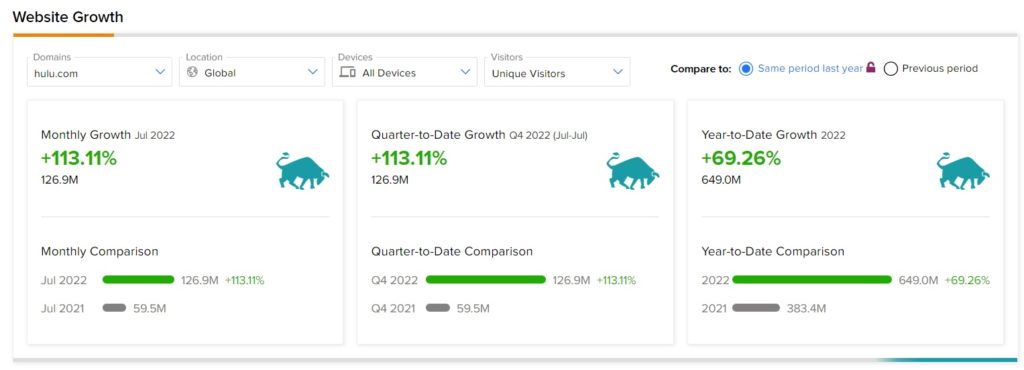

Website Traffic Data is Encouraging

Disney’s rising website traffic acted as a timely precursor to the company’s solid results for the quarter.

TipRanks’ Website Traffic Tool, which uses data from SEMrush Holdings (SEMR), the world’s biggest website usage monitoring service, offers insight into Disney’s performance this quarter.

According to the tool, the Disney website recorded a 113.11% monthly rise in global visits in July, compared to the same period last year. Moreover, year-to-date, Disney website traffic increased by 69.26%, compared to the previous year.

Learn how Website Traffic can help you research your favorite stocks.

Is Disney Stock Expected to Rise?

Turning to Wall Street, analysts sure do think that Disney stock can rise. DIS stock has a Moderate Buy consensus rating based on 17 Buys and eight Holds assigned in the past three months. The average Disney price target of $135 implies 20.1% upside potential.

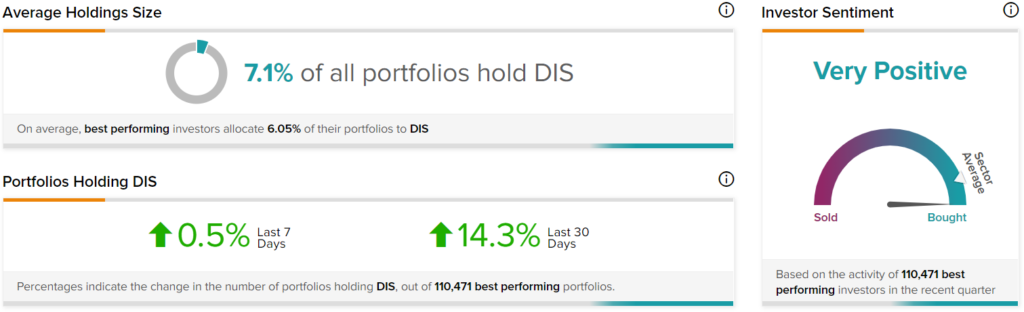

Top Retail Investors are Very Bullish on Disney Stock

TipRanks currently tracks 552,359 investor portfolios that use the Smart Portfolio tool. The top investors, which amount to 110,471 portfolios, appear highly bullish on DIS stock.

In the past 30 days, the number of top-performing TipRanks portfolios holding DIS stock increased by 14.3%, leading to 7.1% of portfolios holding the stock. In the past seven days, this number increased by 0.5%. Disney has very positive investor sentiment, above the sector average, as shown in the image below:

Conclusion: Is DIS Stock a Good Buy?

Disney’s Q3 results beat estimates on every front, causing the stock to rally about 7% in after-hours trading. Its Disney+ segment is performing much better than Netflix (NFLX) in terms of subscriber growth, which has been shedding subscribers. Both analysts and retail investors on TipRanks believe that the stock should be bought.

DIS stock is now about 33% off its lows of around $90 per share. Whether it maintains this momentum remains to be seen. However, if the company keeps beating earnings results in the future (it has done so in eight of the past nine quarters), then the bounce may be sustainable.