Entertainment is big business, encompassing everything from Hollywood to computer games to professional sports to live concerts. But perhaps the most ubiquitous entertainment is just beamed into our homes, in the form of old-school TV and cable broadcasts.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

With so much for consumers to choose from, it would seem that media and entertainment should provide a large enough field for plenty of companies to find their niches – but the competition is fierce. The media landscape is in a state of flux, as traditional movies, TV, and music give way to content creators and streaming channels, and the most successful media companies will get their hands on as many of those streams, old and new, as they can.

Goldman Sachs analyst Michael Ng, watching the media sector, describes the lay of this land and points out his firm’s strategy for media stocks.

“The US media industry is in a state of transition given increasing content competition (e.g., streaming, social, mega tech) and technology disruptions in distribution. Accordingly, we prefer US media stocks with deep competitive moats that should provide better visibility into growth,” Ng noted.

With this in mind, Ng has picked out two media stocks as the best to buy right now. Using the TipRanks platform, we’ve pulled up the details on his choices – Disney (NYSE:DIS) and Fox (NYSE:FOXA), two well-known names in modern media. Let’s give them a closer look.

The Walt Disney Company

The first company we’ll look at needs no introduction. The Walt Disney Company is one of the entertainment industry’s legendary names, founded in the early 1920s, during the days of silent movies. The company quickly became a leading innovator in the field of animation, and developed a sterling reputation for its cartoons, beloved by children and adults alike. The company introduced its iconic Mickey Mouse in 1928.

Today, Disney is best known as a major film studio, producing traditional and computer animation features as well as live-action movies, but it is also known for its network of resorts and theme parks, its cruise line, and its online and TV streaming content, including the rights to the ESPN sports network. Derived from this, Disney has its lines of merchandise, based on its characters and films.

The company’s single most valuable asset remains its film library. The company retains the rights to the films it has produced in a century of movie making, and also has acquired many valuable film franchises – the Marvel Cinematic Universe, the Star Wars films, and Indiana Jones. This movie library is one of the world’s great media archives, and provides Disney with an unmatchable asset for its streaming service. In fact, the company at times uses its archive as a promotional tool, releasing films or special editions on notable dates. Coming up later this year, from July through October, Disney will release 27 of its classic animated short films, newly remastered, on its Disney+ streaming service to celebrate the company’s 100th anniversary.

Turning to the financials, we can look at Disney’s release for fiscal 2Q24, the quarter that ended on March 30 of this year. The company showed total revenues in the fiscal quarter of $22.1 billion. That figure represented a year-over-year gain of just 1.3%, and missed the forecast by $50 million. The revenue total included $5.6 billion brought in from Disney’s streaming content services, an increase of 13% from the prior year.

At the bottom line, Disney reported a non-GAAP earnings-per-share of $1.21, well above the 93-cent EPS reported in fiscal 2Q23, and 10 cents per share better than had been expected.

For Goldman analyst Ng, all of this points to a solid investment choice. Ng is particularly impressed by Disney’s ability to continue generating solid earnings, saying of the company, “Disney is a high quality EPS compounder, which should deliver a 14% EPS CAGR (F2024E-2030E) driven by 6% revenue growth, 9% EBIT growth, and contributions from share buybacks & other income. This mid-term growth is supported by its content, which is underpinned by world-class storytelling and a portfolio of long-term marquee sports rights at ESPN.”

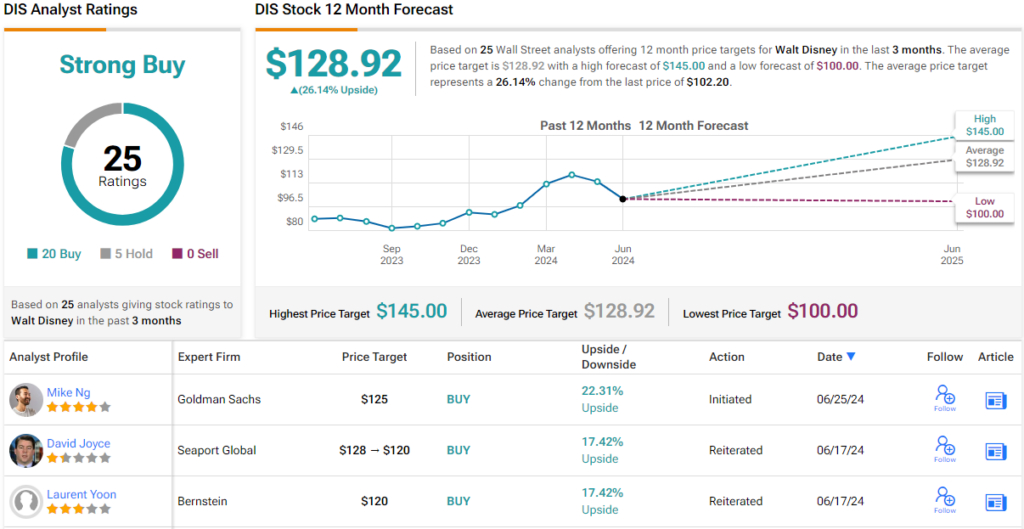

The analyst goes on to put a Buy rating on Disney’s stock, along with a price target of $125, pointing toward a 22% upside in the next 12 months. (To watch Ng’s track record, click here)

The upbeat Goldman view is no outlier on Disney. The stock has 25 recent analyst reviews, with a 20 to 5 breakdown favoring Buys over Holds. The stock’s $102.20 current trading price and its $128.92 average price target together suggest a one-year upside of ~26%. (See Disney stock forecast)

Fox Corporation

Based in Manhattan, Fox is the media empire of Rupert Murdoch and his family. The company operates several brands under the Fox name, including Fox News Media, Fox Entertainment, and Fox Sports, as well as a network of Fox TV stations. The company also owns the Tubi Media Group, a leader in innovating media technology, including ad tech, data analytics, and consumer media streaming. Fox produces and distributes its own original content and also develops content through a diverse range of creators.

Fox has built a place for itself in the global media culture, and in an industry known for a politically leftward tilt, Fox stands out for its more conservative bent. At the same time, the company keeps its focus on the production and distribution of compelling media products – news, sports, and entertainment. The company’s brands have become culturally significant, and the name FOX, with its all-caps styling, is immediately recognizable, a fact that can be attributed to Fox’s success in creating a solid track record in creating news, sports, and entertainment media that audiences want to see.

Last month, Fox released its quarterly report for fiscal 3Q24, and the results beat the forecasts at both the top and bottom lines. The company’s total revenue, while down 15% year-over-year, came in at $3.45 billion and beat expectations by a modest $10 million. The company’s earnings figure, of $1.09 per share based on $520 million in non-GAAP income, was 13 cents per share better than had been anticipated.

Writing up the Goldman view on Fox, Ng notes both headwinds and tailwinds affecting the company, but comes down in favor of the tailwinds: “Although FOXA faces EBITDA headwinds due to cord cutting and declining linear viewership (GSe EBITDA CAGR of -3% F2024E-28E), we see the stock as attractively valued reflecting an under appreciation of the durability of FOXA’s cable network and Television EBITDA, the value of FOXA’s strategic and unconsolidated assets (e.g., FanDuel option, Flutter stake, value of tax shield, Fox studio lot), and near-term upside to consensus estimates in F2025.”

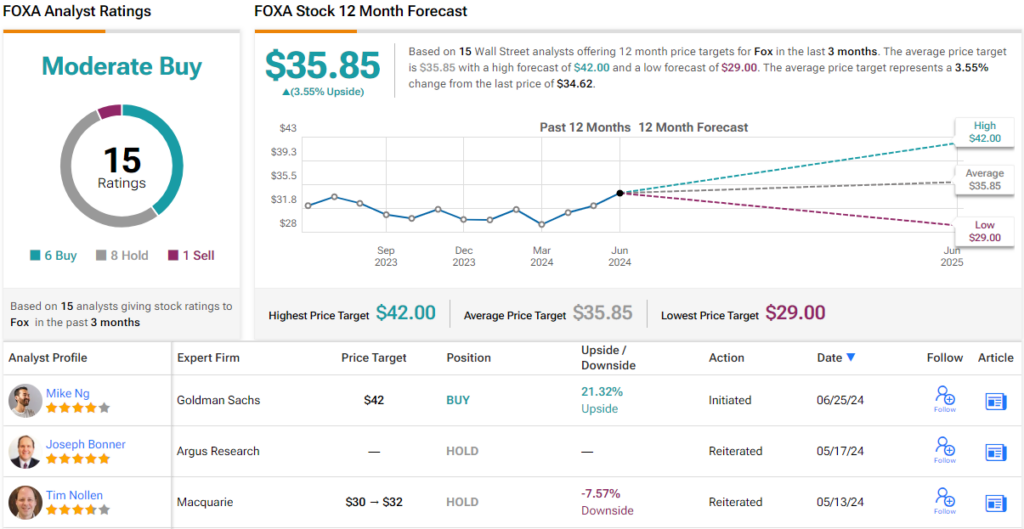

Getting down to the brass tacks, Ng puts a Buy on FOXA shares with a $42 price target to imply a one-year potential gain of ~21%.

Overall, Fox’s stock has a Moderate Buy consensus rating, based on 15 recent analyst reviews that include 6 Buy recommendations, 8 Holds, and a single Sell. The stock’s $34.62 selling price and $35.85 average target price together suggest a modest 3.5% share appreciation. (See Fox stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.