DISH Network (DISH) plans to raise $1.25 billion in a debt offering through its broadcast division DISH DBS Corporation. Dish primarily operates a satellite pay-TV service, but also entered the wireless business last year, when it acquired Boost Mobile.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

In a recent winning move, Amazon (AMZN) chose Dish to provide infrastructure for its cloud-based 5G network.

The debt offering will be subject to market conditions and will involve the sale of senior notes. Dish will sell the notes only to qualified institutional investors, the company said in a press release. More details on Dish’s debt offering plan are expected as the company hasn’t yet revealed the notes’ maturities.

Dish’s broadcast subsidiary intends to use the money from the debt offering to fund general corporate needs, including repayment of some of its existing debts.

The tapping of the debt market now comes at a time when borrowing is cheap because of low interest rates. Companies can borrow cheaply now to replace expensive debts taken earlier.

Notably, the debt offering plan follows a strong first-quarter performance. Profit and revenue jumped from a year ago despite Dish’s loss of pay-TV and wireless subscribers. The company reported revenue totaling $4.50 billion for the quarter ending March 31, 2021, compared to $3.22 billion for the corresponding period in 2020. (See Dish Network stock analysis on TipRanks)

On the back of Dish’s strong Q1 earnings results, Pivotal Research analyst Jeffrey Wlodarczak reiterated a Hold rating but lifted the price target on the stock to $50 from $34. Wlodarczak’s new price target indicates 7.62% upside potential to the current price.

The analyst noted that discussions by Dish management about the company’s wireless efforts are encouraging, supporting the price upgrade. However, he maintained the Hold rating is preserved due to two factors. For one, the stock has already had a substantial run. Additionally, launches of new products are likely to be hit by delays.

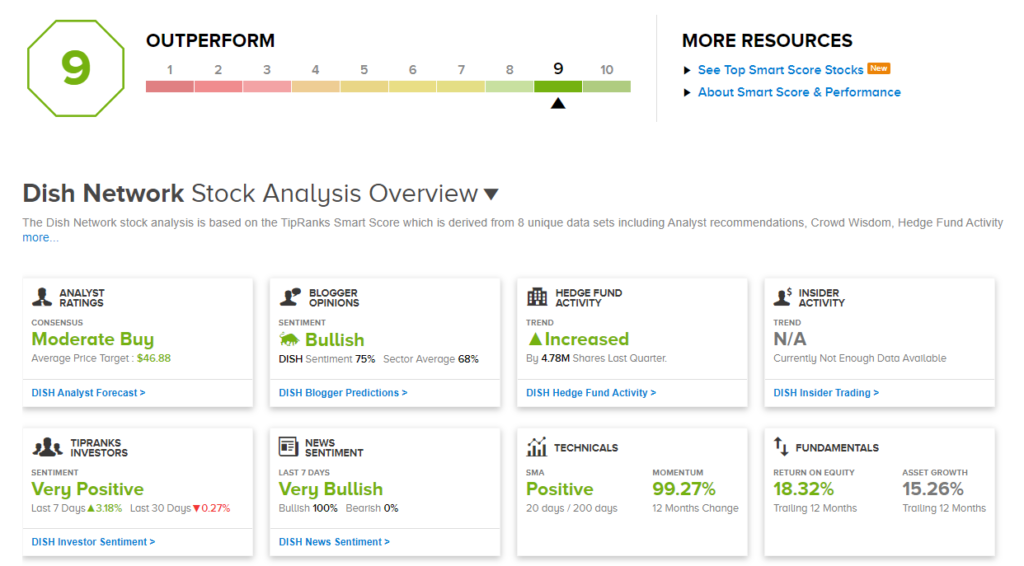

Consensus among analysts on Wall Street is a Moderate Buy based on 3 Buy, 4 Hold, and 1 Sell ratings. The average analyst price target of $46.88 implies 0.90% upside potential to current levels.

DISH scores a 9 out of 10 on TipRanks’ Smart Score rating system, indicating the stock is likely to outperform the market.

Related News:

CGI Wins Public Sector Tender Worth C$576M In Finland

Leidos Completes Acquisition Of Gibbs & Cox Acquisition; Ups Guidance For FY21

GoPro Transition Pays Off Delivers Revenue And Profit Growth in 1Q