Altria Group (MO) has seen its stock price soar by 47% over the past year, fueled by growing investor confidence in tobacco stocks. This optimism stems from an improving regulatory landscape and the appeal of high-yield dividends as potential interest rate cuts loom. Now, despite this incredible rally compressing its dividend yield from 10% last year to about 7%, Altria remains a top-notch pick for income investors. Not only is it one of the few names among U.S. large-caps still yielding over 7%, but its robust performance, including Fiscal 2024, set to be another year of record profits, further reinforces it as a compelling investment for income investors. Therefore, I remain bullish on the stock.

What’s Driving Altria’s Bullish Momentum?

Tobacco stocks have been thriving recently, with not just Altria but also peers like Philip Morris (PM) and British American Tobacco (BTI), reinforcing my optimism about Altria’s stock. These companies have benefited from a more favorable regulatory climate and rising investor demand for high-yield investments as potential rate cuts loom.

Specifically, regulatory developments over the past year have boosted confidence in the industry’s future, creating a favorable backdrop for rising share prices. For instance, the FDA has intensified its enforcement actions against illicit e-vapor products, with notable seizures of unauthorized products valued at millions of dollars. These measures, of course, aim to stabilize the legitimate market and, indeed, benefit regulated companies like Altria. Moreover, the FDA proposed a rule requiring tracking numbers for imported vapor products, a measure Altria has long advocated.

Simultaneously, the prospect of interest rate cuts has encouraged income-oriented investors to flock to high-yielding assets. With its yield hovering in the double-digits last year, you can see why many investors jumped into the opportunity and why many more have been chasing the stock since. Altria’s tremendous 54-year record of dividend increases, which has elevated the company’s status into a beacon of reliability, especially for conservative income-seekers, has also contributed to this sentiment.

Setting The Stage for Record-Setting Profits in 2024

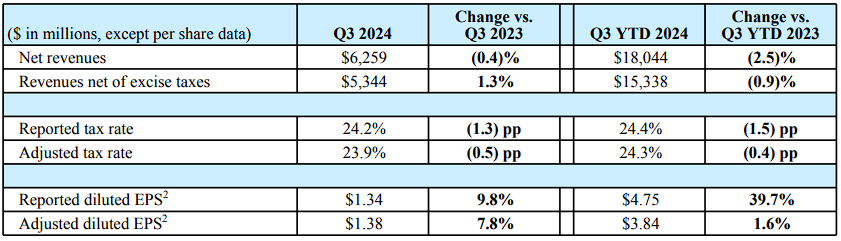

Despite the two catalysts I just noted, Altria is also positioned for record profits this year, which is another reason I remain bullish on the stock. Altria’s Q3 results again showed its resilience, with revenues net of excise taxes rising 1.3% year-over-year. Despite an 8.6% drop in cigarette shipment volumes due to the typical, ongoing decline in the combustible user population, Altria maintained relatively steady sales through price increases and operational efficiencies. As always, Marlboro, its flagship brand, remained dominant in the premium cigarette market.

It’s also worth noting that Altria’s oral tobacco products recorded solid numbers, with net revenues in the segment climbing 5.4% year-over-year. Altria’s oral nicotine pouch brand, on! reported a 46% increase in shipment volumes, reflecting strong consumer adoption too. In the meantime, with higher combustible prices and sales growth in oral tobacco, Altria’s margins expanded. Along with fewer outstanding shares due to continued buybacks, its adjusted EPS grew by 7.8% in Q3. Management, therefore, reaffirmed its guidance for full-year EPS growth of 2.5% to 4%, marking another record-setting year for adjusted EPS.

Is Altria Still an Attractive Pick for Income Investors?

So, returning to the initial question of whether Altria remains a compelling choice for income investors following this past year’s extended rally, I believe the answer is a strong yes. The stock’s dividend yield remains quite lofty, while an improving regulatory environment and growing earnings imply that the tobacco giant is positioned for continued dividend growth for years to come. Additionally, with shares trading at just 10.9 times the expected Fiscal 2024 EPS, Altria doesn’t seem at all overvalued despite the extended rally. Management’s decision to accelerate the buyback program, repurchasing $680 million worth of stock in Q3, should also reinforce investors’ confidence in Altria’s investment case at today’s valuation.

Is Altria Stock a Buy?

Wall Street analysts appear a bit more cautious about Altria’s future prospects. Specifically, Altria stock features a Moderate Buy, with recent analysts ratings of four Buys, one Hold, and two Sell ratings over the past three months. However, at $54, the average MO stock forecast implies a 2.7% downside potential.

For the best guidance on buying and selling MO stock, look to Owen Bennett. He is the most profitable analyst covering the stock (on a one-year timeframe), boasting an average return of 7.83% per rating and a success rate score of 57%.

Summing Up

In conclusion, I believe that Altria remains a compelling investment for income-focused investors. Despite a stretched rally that compressed its dividend yield, the stock’s robust fundamentals, including a favorable regulatory environment, strong earnings growth, and status as one of the highest-yielding U.S. large-caps, reinforce its appeal. With a 54-year history of dividend increases and a forecasted record-setting fiscal 2024, Altria certainly offers both reliability and growth. Finally, trading at a humble valuation, Altria should offer a rather wide margin of safety for investors as well.