Delta Air Lines Inc (DAL) stock has been facing some turbulence in 2025, shedding more than a quarter of its value in the past three months. The air transportation giant lowered its revenue and margin guidance for Q1 2025 earlier this month, citing a recent decline in consumer and corporate confidence due to macroeconomic uncertainty. In parallel, Delta hopes that continued efforts to improve its premium services and customer loyalty program will pay dividends.

In my view, tempered expectations signal more trouble ahead. While this makes me cautiously neutral about the stock as the year passes, Delta seems strategically positioned to withstand the pressure over the long term. The company’s fledgling stock dividend is another factor that could buoy long-term DAL bulls.

Macroeconomic Headwinds Buffeting DAL

Some plane rides are unavoidable. People travel for business or family emergencies. Other plane rides are recreational and, therefore, expendable. This is the issue with carriers like Delta during trying economic times. Vacations aren’t as appealing with lower disposable incomes. While there are always rumors of recessions and economic slowdowns, the latest is gathering steam.

A recent Deutsche Bank survey estimated a 50% chance of a recession sometime this year. Some consumer trends also support this narrative. For instance, The Conference Board’s headline consumer confidence index dropped 9.6 points to 65.2—the lowest level in over a decade. The index is based on “consumers’ short-term outlook for income, business, and labor market conditions. “ A value under 80 is usually a good signal of impending recession.

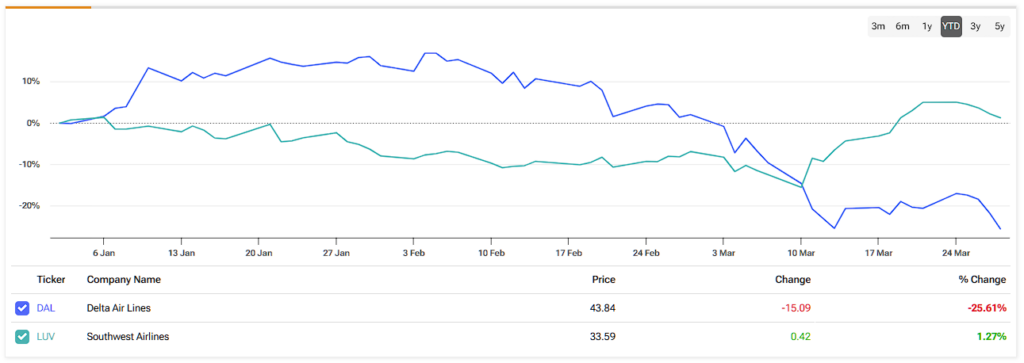

In addition, Delta’s website traffic has been down in recent months. This signals the obvious: decreased interest in plane tickets. However, Delta looks more resilient than its peers like Southwest Airlines (LUV). Southwest’s own website, which has very similar traffic numbers to Delta’s, saw traffic dip under 40 million visits last Fall, with a far less prominent bounce in traffic thereafter.

Delta’s Premium Strategy

Delta positions itself as a premium airline. For example, it offers premium cabins, including flatbeds for long international flights. Delta even provides specific revenue performance from its premium products during its earnings reports. In the quarter ending December 31, its premium products segment generated $5.2 billion in revenue (up 8% year-over-year). Its main cabin still packs the biggest punch with $6 billion in Q4 revenue (up just 2%).

Given the numbers, it makes sense that the company is focusing on its most promising segment, which is also the most profitable one. However, this could be a double-edged sword. Delta’s premium products could also be vulnerable to economic woes. Remember people traveling for business? While the need may remain in a recession, people may opt for more affordable travel solutions. Delta’s focus on its loyalty program ($1 billion in Q4 revenue, up 8%) will be key to keeping its customers.

DAL’s Financial Performance and Revised Expectations

Looking closely at its revised expectations for Q1, Delta now expects EPS of $0.30-0.50 compared to a consensus estimate of $0.85. Revenue growth projections dropped from 7%-9% to 3%-4%. These are not minor adjustments. Delta did attribute the changes to softness in domestic demand. So, contrary to my concerns, its premium, international, and loyalty segments appear somewhat unaffected so far. To play devil’s advocate, it is also possible that its premium segments are slower to respond to whispers of economic uncertainty.

Zooming out, Delta had a strong 2024. Total revenues were $61.64 billion, representing 8% year-over-year growth and highlighting steady demand post-pandemic. After accounting for expenses, its operating income was $6 billion, or 9.7% of revenues, which is pretty good for an airline. Net income was $3.46 billion, which is about six cents per dollar in profit.

Also, Delta continues to pay down its debt. Net debt dropped from $24.54 billion at the end of 2023 to $19.7 billion. This is pretty aggressive deleveraging. Recall that airlines were highly leveraged coming out of the pandemic. Delta’s strong cash flow generation enables it to reduce its reliance on debt, which is suitable for its long-term financial flexibility and credit profile.

Is Delta Airlines a Good Stock to Buy Now?

Wall Street is unanimously bullish on Delta Airlines. DAL stock carries a Strong Buy consensus rating based on 15 Buy, zero Hold, and zero Sell ratings over the past three months. DAL’s average price target of $79.07 per share implies more than 80% upside potential over the next twelve months.

Following Delta’s updated Q1 guidance earlier this month, Goldman Sachs analyst Catherine O’Brien reiterated her Buy rating on DAL and set a price target of $83 per share. So, apparently, while Wall Street recognizes some short-term headwinds for Delta, they seem confident that the airliner is well-positioned to withstand economic uncertainty and ultimately prevail.

Judging by the information above, I, too, believe this to be the case. However, I remain neutral in the short term and plan to turn bullish in the medium-long term, subject to the airline achieving various performance milestones. The upcoming earnings call on April 9th is a key date for DAL stock watchers.

Delta Airlines on the Runway for Future Takeoff

To summarize, Delta’s lowered expectations for Q1 signal economic trouble ahead. With this in mind, its recent stock performance is unsurprising, primarily as airline stocks are known for greater volatility. For example, Delta’s stock beta is 1.25. This implies its stock is 25% more volatile than the broader market. While a storm is ahead, Delta’s diversified revenue streams may provide a shield to take on some hail without causing too much structural damage in the long run.

In the past, stock dips like the one we’re seeing now would be the optimal opportunity to buy DAL. While this may very well be the case, I think we are still a ways away from the true impact of an economic slowdown, which leaves me cautiously neutral on DAL stock.