American air carrier Delta Air Lines (DAL) delivered outstanding third-quarter results, posting its first quarterly profit since the beginning of the pandemic as travel demand picked up pace through the summer. However, shares sank 5.8% to close at $41.03 on October 13 as the company warned of rising fuel prices.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Adjusted earnings of $0.30 per share significantly beat analyst estimates of $0.17 per share. In Q3FY20, Delta posted a huge quarterly adjusted loss of $8.47 per share. The company warned that the current rise in fuel prices will hamper its ability to profit in the fourth quarter.

Revenue stood at $9.15 billion and outpaced the Street’s estimate of $8.39 billion. In the same quarter last year, the company posted revenue of $2.6 billion. Notably, Delta recorded a combined completion factor of 99.72 for both the mainline and Delta Connection segments in August. (See Insiders’ Hot Stocks on TipRanks)

Commenting on the solid results, Ed Bastian, CEO of Delta, said, “While demand continues to improve, the recent rise in fuel prices will pressure our ability to remain profitable for the December quarter. As the recovery progresses, I am confident in our path to sustained profitability as we continue to provide best-in-class service to our customers, strengthen preference for our brand, while creating a simpler, more efficient airline.”

Based on current flying demand and the upcoming holiday season, Delta expects its Q4 revenue to recover to a low 70% compared to Q4FY19, with 80% capacity. Additionally, the company announced the acquisition of two used A350 aircraft, which will start deliveries in the December quarter.

In response to Delta’s quarterly performance, Citigroup analyst Stephen Trent reiterated a Buy rating on the stock with a price target of $58, implying 41.4% upside potential to current levels.

Trent believes that the company’s warning of rising fuel prices is based on the current oil price scenario, which may or may not play out in the medium term. He expects Delta’s revenue to recover slowly but steadily into 2022 and is not worried about the future oil price scenario.

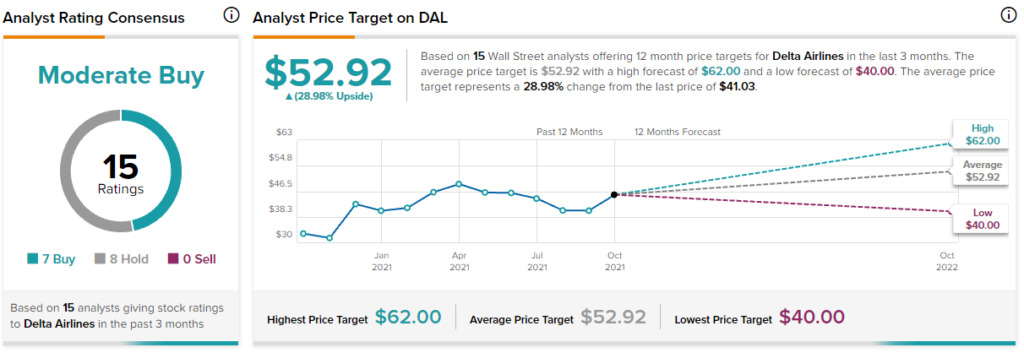

Overall, the stock has a Moderate Buy consensus rating based on 7 Buys and 8 Holds. The average Delta Air Lines price target of $52.92 implies 29% upside potential to current levels. Shares have gained 29.2% over the past year.

Related News:

IBM Board Approves Kyndryl Separation

Boeing Announces Q3 Jet Deliveries; Shares Fall

International Paper Increases Share Buyback Program by 2B, Slashes Quarterly Dividend