Shares of Dada Nexus Limited jumped 30.5% on Friday after China’s on-demand delivery and retail platform provider reported 3Q results, which improved significantly from a year ago.

Dada’s (DADA) 3Q revenues soared 85.5% to RMB1,301.5 million, reflecting higher order volumes and an increase in Gross Merchandise Value (GMV). GMV grew 90.7% year-on-year, driven by an increase in the number of active consumers and average order size.

The company reported an adjusted loss per share of RMB0.36 in 3Q, compared to the year-ago quarter’s loss of RMB1.71 per share.

Dada CEO Philip Kuai said, “We are pleased to report strong performance for the third quarter, with our business continuing to grow and our leading position further strengthening with market share expansion. JDDJ remains the largest local on-demand retail platform in the China supermarket segment with 24% market share in the first nine months of 2020, up from 21% in 2019. Dada Now maintains as the largest open on-demand delivery platform in China with 24% market share in the first nine months of 2020, up from 19% market share in 2019.”

For 4Q, the company forecasts revenues of between RMB2 billion and RMB2.1 billion. (See DADA stock analysis on TipRanks)

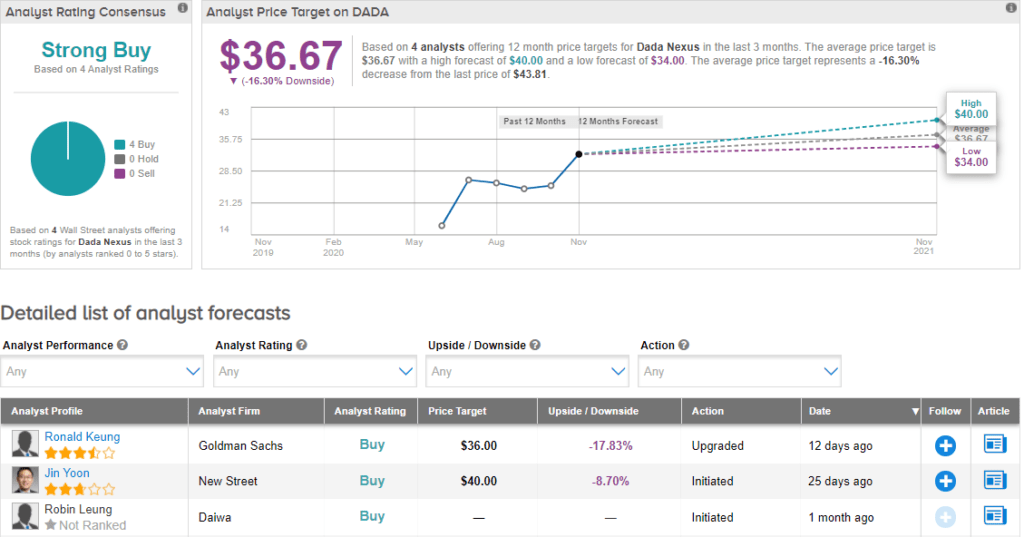

Ahead of its earnings, on Nov. 11, Goldman Sachs analyst Ronald Keung upgraded the stock to Buy from Hold and lifted the price target to $36 (17.8% downside potential) from $28.50. Keung also raised his revenue estimates for 2021 and 2022 on expectations of further growth in store-to-home and on-demand delivery services. The analyst believes that online sales would account for approximately half of China’s total grocery sales by 2025 and Dada’s JD Daojia platform is likely to be the key beneficiary to this consumer shift.

Currently, the Street has a bullish outlook on the stock. The Strong Buy analyst consensus is based on 4 Buys. The average price target stands at $36.67 and implies downside potential of about 16.3% to current levels. Shares have risen by about 174% since its listing on Nasdaq on June 5 this year.

Related News:

Foot Locker Tops 3Q Estimates; Shares Dip 5% On Covid-19 Woes

Williams-Sonoma Pops 7% On Blowout 3Q Earnings; Analyst Raises PT

Hibbett’s 3Q Profit Soars 353%; Analyst Raises PT