Energy company Chevron (CVX) has faced considerable pressure over the past year, primarily due to weak oil prices. Remarkably, the stock is now trading at roughly the same levels as it did in early 2022, reflecting years of stagnation. However, Chevron has emerged as a compelling dividend growth pick. With a starting yield of 4.4%, promising free cash flow growth, and a valuation that appears quite cheap, CVX stock stands out as a rock-solid investment, in my view, particularly for investors looking for growing income. Therefore, I’m bullish on CVX.

Why CVX Stock Has Been Under Pressure Over the Past Year

Before I discuss CVX’s dividend growth prospects, I think it’s necessary to understand why CVX has been under pressure recently, especially since the company remains a free cash flow powerhouse despite these challenges. Well, no surprise, the main factor has been persistently weak oil prices. Oil prices were rather uninspiring for the better part of 2024, driven by many reasons, including slower-than-expected demand recovery in major economies like China and high production levels from OPEC+, which weighed heavily on crude oil markets. Global economic uncertainty and a surplus of inventory made weak prices even worse.

These conditions inevitably impacted Chevron. With Chevron being an integrated energy behemoth, its performance is, of course, directly tied to oil prices. Lower realizations for oil and gas production, thus, directly suppressed its results, as seen throughout its recent earnings reports. With additional headwinds like weaker refining margins and hurricane impacts reducing output in key regions like the Gulf of Mexico, I think the pressure on CVX stock over the past year was certainly unavoidable.

CVX Remains a Free Cash Flow Machine, Supporting Dividend Growth

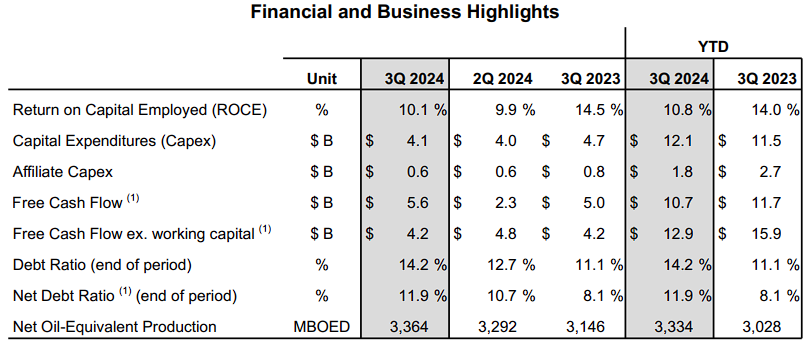

Now, despite weak oil prices, I find it extraordinary how CVX keeps delivering robust free cash flow, which should support its ability to maintain and grow dividends. For context, in Q3 2024, Chevron reported a free cash flow of $5.6 billion, up from $5.0 billion in the prior year, with its upstream production rising by 7% year-over-year. Chevron celebrated record output in the Permian Basin, while new projects in the Gulf of Mexico contributed to this growth.

More importantly, analysts project Chevron’s free cash flow to reach $16.3 billion for FY2024, with further growth anticipated in the following years. In particular, free cash flow is projected to grow to $21.1 billion in 2025 and $26.3 billion in 2026. From what I can gather, this anticipated surge can be likely attributed to the completion of high-return projects, ongoing production efficiencies, and cost controls. It’s also worth noting that Chevron’s portfolio tweaks, like selling off non-core assets such as Canada’s Kaybob Duvernay position (which wasn’t doing too great), should help simplify operations and, indeed, boost free cash flow. In turn, this should support accelerated dividend growth.

CVX’s Potential for Accelerated Dividend Growth

Speaking about Chevron’s dividend, I can’t help but first praise its excellent track record and remind you that the energy giant is a trustworthy dividend payer. In particular, the company has raised its dividend for 37 consecutive years, demonstrating resilience even during some of the harshest times for the sector, like the Great Financial Crisis and the COVID-19 pandemic. Recently, Chevron’s dividend growth has picked up speed. In 2024, it raised its dividend by 7.9%, following increases of 6.3% in 2023, 6% in 2022, and 3.9% in 2021. This trend aligns with Wall Street’s positive free cash flow outlook.

To quantify this, note that Chevron’s annual dividend obligations totaled about $11.7 billion over the past 12 months. Thus, they are well-covered, even with 2024’s weaker projected free cash flow. However, Wall Street’s expected free cash flow growth in subsequent years implies even ampler affordability, suggesting the ongoing acceleration in dividend hikes is likely to endure. In the meantime, Chevron offers a potent entry yield of 4.6%, further boosting its appeal as an attractive asset for growing income. Finally, trading at just 10 times its expected FY2027 free cash flow, I truly believe that CVX is undervalued and offers a relatively wide margin of safety for investors from its current price levels.

Wall Street’s Take on CVX Stock

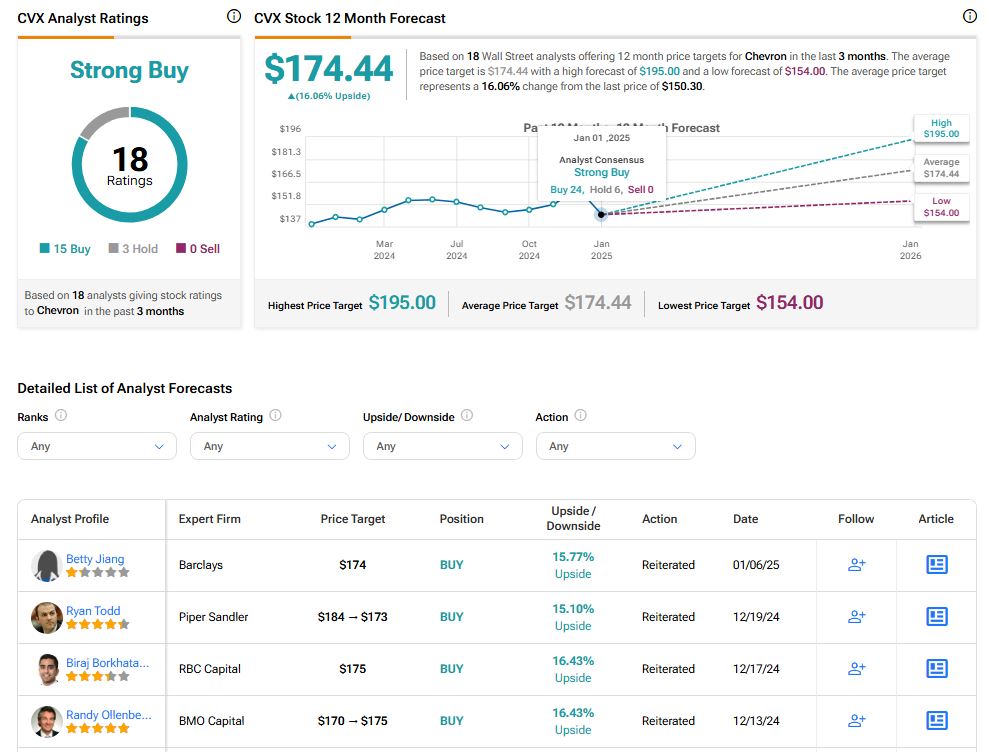

Turning to Wall Street, Chevron features a Strong Buy consensus rating based on 15 Buys and three Holds ratings assigned in the past three months. At $174.44, the average CVX price target implies 16.1% upside potential.

If you’re trying to figure out which analysts to follow for trading CVX stock, Ryan Todd from Piper Sandler is definitely worth a look. Over the past year, he’s been the most profitable analyst covering CVX, with an average return of 11.21% per rating and a 63% success rate.

Conclusion

To wrap up, Chevron has faced some challenges lately, which mirror the broader pressures in the energy sector. Even so, the company’s strong ability to generate free cash flow highlights its resilience. On top of that, its solid track record of growing dividends, a compelling 4.6% yield, and recent increases in payouts make it a suitable option for investors looking for income. At the same time, with the stock trading at a discounted valuation, I think there’s a wide margin of safety in its investment case. Thus, I see Chevron as an appealing choice for a dividend growth portfolio.