Curaleaf Holdings (CURA) reported higher revenues in the third quarter of 2021, but its loss widened from a year ago.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The giant cannabis company sells a wide range of products including cannabis-infused beverages, edibles, dried flowers, and vapes. (See Insiders’ Hot Stocks on TipRanks)

Revenue & Earnings

Total revenue came in at $131 million for Q3 2021, an increase of 74% from Q3 2021. Retail turnover revenue was $225 million, representing growth of 66% year-over-year. Retail turnover represented 71% of total turnover. During the third quarter, the Company opened two new dispensaries including one in Bordentown, New Jersey and one in Wells, Maine, reaching 109 dispensaries at the end of the quarter. Wholesale revenue increased 105% year-over-year to $92 million.

Net loss attributable to Curaleaf Holdings was $57 million, compared to a net loss of $9 million in the third quarter of 2020. Adjusted EBITDA was $71 million for the quarter ended September 30, 2021. The company generated $52 million of positive operating cash flow.

On Track to Achieve Revenue Guidance

Boris Jordan, executive chairman of Curaleaf, said, ” While we faced some transient headwinds during the quarter, we continued to execute well against our strategic initiatives, prioritizing growth and gaining market share.

“As a result, we remain on track to achieve our $1.2 to $1.3 billion annual revenue guidance, albeit at the lower end of the range, representing growth of over 90%. Strategic M&A remains a key pillar our growth plan.”

Curaleaf closed its Los Sueños Farms acquisition in October. On November 8, the company announced a deal to acquire Tryke Companies, a vertically integrated MSO which bolsters its leadership position in Nevada, Arizona, and Utah. This acquisition will be immediately accretive to Curaleaf’s margins and cash flow.

On November 8, Craig-Hallum analyst Eric Des Lauriers kept a Buy rating on CURA but lowered its price target to $16 (C$19.92). This implies 55.6% upside potential.

Des Lauriers believes Curaleaf could face above-average pricing headwinds in the near term in decelerating markets like Florida and Pennsylvania, given its brand focuses on distillate-derived products over premium flower, and strategic focus on growth rather than profit, leading him to lower estimates.

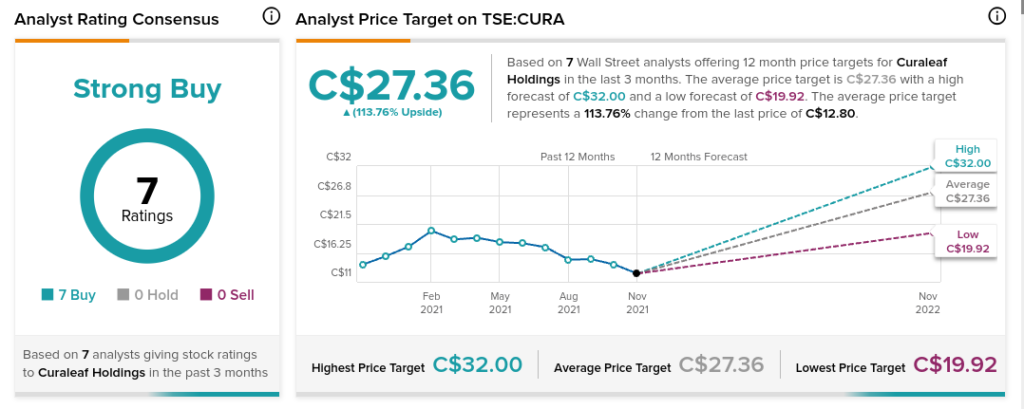

The rest of the Street is bullish on CURA with a Strong Buy consensus rating, based on seven Buys. The average Curaleaf Holdings price target of C$27.36 implies 113.8% upside potential to current levels.

Related News:

Aurora Cannabis Buys Stake in Growery; Shares Pop

Canopy Growth Posts Narrower Q2 Loss; Shares Plunge

Curaleaf Expands Select Brand, Rolling Stone Partnership