CrowdStrike Holdings exceeded quarterly sales expectations mainly driven by demand for cloud-based security solutions amid the COVID-19 pandemic-led remote working trend.

However, the outperformance wasn’t enough to win investors’ confidence for more gains, at least for now, as the stock dropped 6.4% in the extended market session after closing 1.1% lower on Wednesday. It looks like some investors are taking profits after shares rallied 185% this year.

CrowdStrike’s (CRWD) 2Q revenues soared 84% to $199 million year-over-year, surpassing analysts’ expectations of $188.5 million. Adjusted EPS of $0.03 compared favorably with the year-ago quarter’s loss of $0.18 per share as well as the Street consensus of a loss of $0.01. The cybersecurity solution provider added 969 net new subscription customers during the quarter, reflecting 91% year-over-year growth.

Furthermore, CrowdStrike raised its outlook for fiscal 2021. The company now anticipates revenues between $809.1 million and $826.7 million, up from its earlier projection of $761.2-$772.6 million. It now forecasts to report adjusted EPS in the range of $0.02-$0.08 compared with the previous expectation of a loss of $0.05-$0.08. (See CRWD stock analysis on TipRanks).

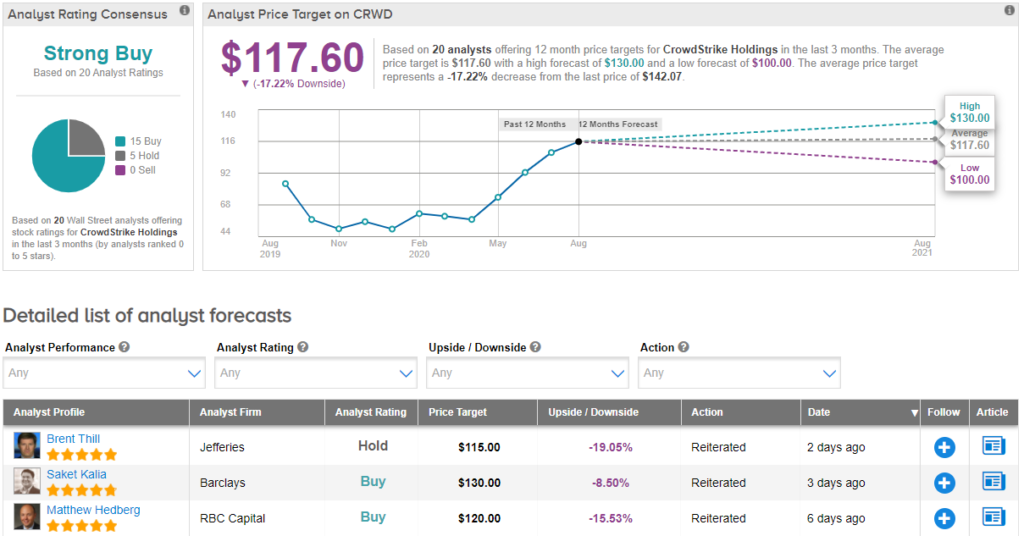

Ahead of the earnings, Jefferies analyst Brent Thill had said that CrowdStrike is “one of the biggest beneficiaries” of the remote working trend. However, Thill is concerned about its hefty valuation given a spectacular year-to-date rise in the stock price. Therefore, he reiterated his Hold rating and a price target of $115 (19% downside potential).

Overall, the Street has a Strong Buy analyst consensus. Meanwhile, the average price target of $117.60 implies downside potential of 17.2% to current levels.

Related News:

Yext Earnings Preview: RBC Sticks To Buy Call, Sees Revenue Beat

Roth Lifts Gogo’s PT After Commercial Aviation Unit Sale

Can Qualcomm Keep Up Its Outstanding Performance? This Top Analyst Says Yes