What does it take to move a stock price from $0.29 to $15.81 — an increase of 5,350% — in just 18 days?

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Coronavirus, of course. Or more precisely, a vaccine to fight it.

An unprofitable biotech that focused on commercializing therapies to cure blindness prior to the present pandemic, Ocugen (OCGN) stock took on a new life on December 22, when it announced plans to co-develop Indian Bharat Biotech’s “Covaxin” vaccine against the SARS-CoV-2 coronavirus.

Ever since that announcement, the stock has been on a tear, leaving Chardan analyst Keay Nakae‘s previous $0.70-per-share price target in the dust.

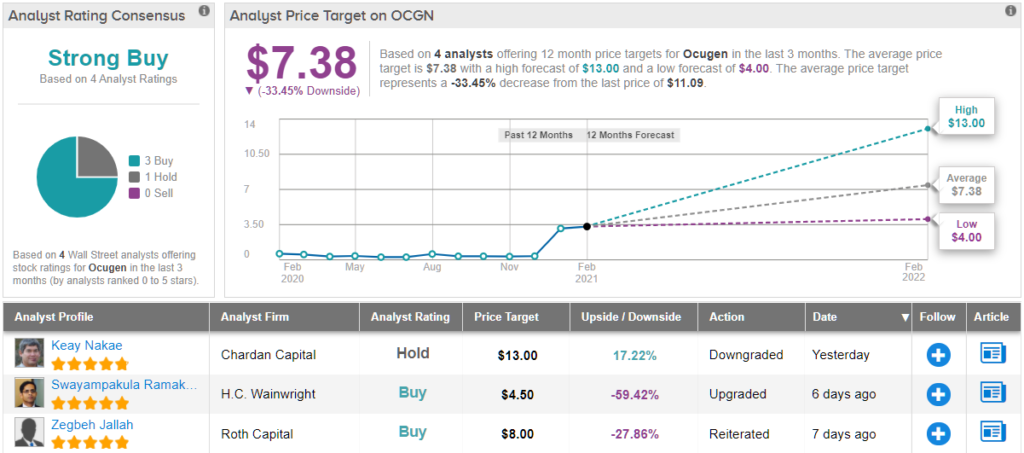

Yesterday, Nakae took another look at Ocugen at its present share price, and declared it overpriced, downgrading the shares to Neutral (i.e. Hold). However, the analyst did raise his price target to $13 (to account for the stock’s astounding run-up in price), which implies a 17% upside from current levels. (To watch Nakae’s track record, click here)

Why is Nakae having second thoughts about Ocugen now? Valuation is obviously a concern, and certainly the primary one. After all, hype aside, Ocugen stock is a company almost entirely devoid of revenues. In all the past year, its sales haven’t exceeded $50,000 (It almost goes without saying, then, that Ocugen has no profits). At its current market capitalization, therefore, Ocugen stock sells for a mind-numbing 40,000 times trailing sales, which is kind of a lot.

Now, what must Ocugen do to justify this valuation — one that’s not just “sky high” above fair value, but more orbiting somewhere out past Saturn?

First and foremost, notes Nakae, the company has to win Emergency Use Authorization for Covaxin from the FDA, which will be no easy trick. Although Covaxin has an ongoing Phase III clinical trial, that’s happening in India, and Nakae thinks that even after initial results are in (probably in March), the company may need to conduct an additional study in the U.S. to win FDA approval.

Next, Ocugen will need to set up manufacturing operations to produce the vaccine in the U.S. This will of course cost money, and this is probably one reason why Nakae predicts the company “will likely need to raise debt or equity funds in the future.” (After all, Ocugen “does not have any products that generate revenue” currently, and the $19 million it has in the bank probably won’t cover all the bills needed to set up manufacturing operations). Finally, once manufacturing has been set up and the vaccine goes on sale, the company will have to compete with multiple other vaccines already on the market — and then split any profits that do result with its partner Bharat.

And of course, all of this only happens if the vaccine proves effective, and safe enough to convince the FDA to issue the EUA.

So how long will all of this take? How long before Ocugen turns into something resembling a business, as opposed to just a “coronavirus play?” Nakae doesn’t say, but he also forecast Ocugen collecting any revenues at all this year, so it won’t be soon.

So, that’s Chardan’s view, what does the Street of the Street have in mind? The current outlook offers a conundrum. On the one hand, based on 3 Buys and 1 Hold, the stock has a Strong Buy consensus rating. However, after surging so high this year, the average price target, at $7.38, implies ~34% downside over the coming months. It will be interesting to see whether the analysts downgrade their ratings or upgrade price targets over the coming months. (See OCGN stock analysis on TipRanks)

To find good ideas for coronavirus stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.