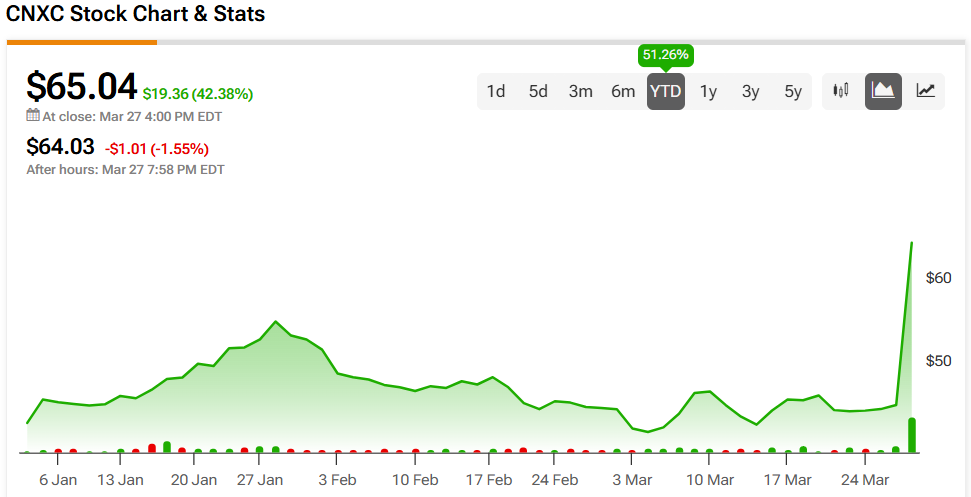

Concentrix’s (CNXC) recent first-quarter performance exceeded Street expectations, resulting in a significant 42% surge in its stock price on Thursday. The company reported revenue and earnings beats, while operating income, cash flow, and shareholder returns also saw improvements. Looking ahead, Concentrix anticipates moderate revenue growth for the remainder of fiscal year 2025, despite currency headwinds, driven by a robust sales pipeline and the introduction of new AI services. Analysts are optimistic about the future, though they maintain a cautious outlook in the near term due to macroeconomic challenges.

Strong Financial Performance

Concentrix is a global provider of customer experience (CX) solutions that integrate technology to enhance service delivery. Their offerings include optimizing CX processes, driving technological innovation, and automating both front- and back-office operations. Its client base spans industries such as consumer electronics, technology, e-commerce, health insurance, global initial public offerings (IPOs), social brands, and banking.

The company reported strong financial performance for the first quarter, with revenue of $2.37 billion, representing 1.3% growth on a constant currency basis. The Non-GAAP operating income was $322 million, resulting in a margin of 13.6%, which marks a 30 basis point improvement from the previous year. Additionally, the company reported an adjusted EBITDA of $374 million, equating to a 15.8% margin. Non-GAAP earnings per share (EPS) beat expectations at $2.79, marking a nearly 9% increase year over year.

Management has issued guidance for the second quarter of fiscal year 2025, projecting revenue between $2.370 billion and $2.390 billion, with an expected negative foreign exchange impact of approximately 90 basis points, suggesting constant currency revenue growth of between 0.50% and 1.25%. Non-GAAP EPS is anticipated to fall between $2.69 and $2.80. For the full fiscal year, the company expects revenue of $9.490 billion to $9.635 billion, reflecting a 135-basis-point impact from foreign exchange. Full-year non-GAAP EPS is expected to be in the range of $11.18 to $11.77.

A Bullish Outlook

Analysts following the company have maintained a generally bullish outlook. For example, Vincent Colicchio from Barrington has reiterated a Buy rating, maintaining a price target of $54.00, based on Concentrix’s solid financial performance and growth prospects. Colicchio foresees sequential revenue growth driven by a strong sales pipeline and the expansion of generative AI services, assuring an optimistic EPS projection for fiscal years 2025 and 2026.

Meanwhile, Ruplu Bhattacharya from Bank of America Securities has reiterated a Hold rating and marginally increased the price target to $59.00. Despite Concentrix’s robust quarter performance, Bhattacharya maintains a conservative view, citing slightly increased revenue guidance for the fiscal year 2025 amidst a challenging operating environment. He acknowledges the potential upsides from AI advancements and synergies from the WebHelp acquisition but also points to macroeconomic uncertainties and initial integration risks that warrant caution.

Concentrix is rated a Strong Buy overall, based on the recent recommendations of four analysts. The average price target for CNXC stock is $64.25, which represents a potential downturn of -1.21% from current levels.