Meta Platforms (NASDAQ:META) fans had plenty to savor on Wednesday at Meta Connect, the social media giant’s annual developer conference.

Among the highlights, Meta unveiled the Orion AR glasses prototype, showcasing neural hand gesture controls and lightweight design. The company also introduced the Quest 3S mixed-reality headset, priced competitively at $299.99. Moreover, Meta announced substantial enhancements to its AI offerings, including celebrity-voiced AI chatbots and upgraded AI-powered tools for Instagram and WhatsApp. Not to be outdone, the Ray-Ban smart glasses received exciting updates as well, featuring language translation and deeper AI integration.

Meta also introduced Llama 3.2, its latest large language model with significant enhancements. Llama 3.2 marks a major advancement by being the first Llama model with multimodal capabilities, meaning it can process and analyze both text and images. This allows it to interpret visual data, such as identifying objects in photos, making it a direct competitor to models like OpenAI’s GPT-4 and Anthropic’s Claude 3.

Taking it all in, Baird’s Colin Sebastian, a 5-star analyst rated in the top 4% of the Street’s stock pros, thinks the Llama update “further distinguishes Meta’s LLMs from closed competitors (e.g., Claude, Chat-GPT, Gemini).”

While Sebastian thinks the event offered “more of an incremental update,” he believes it showed the company’s “substantial progress” within Reality Labs and AI/GenAI.

“Understandably,” the top analyst went on to say, “Meta focuses on product and usability before monetization, although we continue to see a variety of monetization options, including search-based advertising, subscriptions, micro-transactions, and content sales, beyond higher engagement levels and better overall ad performance.”

Meanwhile, driven by generally positive trends in social media advertising, with September showing some improvement after a slight dip in August, Sebastian has raised his META estimates. He now sees 2025 revenue reaching $184.4 billion (amounting to 13.9% year-over-year growth vs. 13% beforehand) while his 2024 and 2025 EPS estimates are also increased to $21.28 and $23.23, respectively, compared to the prior $20.98 and $22.46.

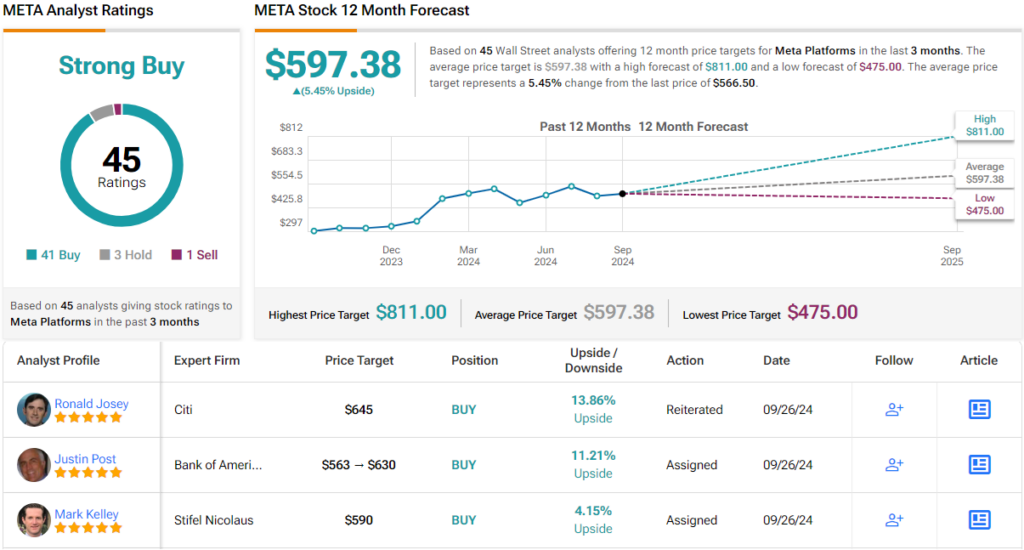

Factoring in the “significant opportunities” ahead, Sebastian has also raised his price target for Meta from $530 to $605. Sebastian’s rating stays an Outperform (i.e., Buy). (To watch Sebastian’s track record, click here)

Other analysts are similarly optimistic. The consensus rating for Meta is a Strong Buy, based on 41 Buys, 3 Holds, and 1 Sell. However, considering the shares’ outperformance – up by 61% year-to-date – the average price target of $597.38 implies a modest upside of ~5% from current levels. (See Meta stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.