Coca-Cola European Partners Plc, the world’s largest independent bottler of the storied soft drink, is in negotiations to snap up Australia’s Coca-Cola Amatil Ltd. in move to expand its footprint in Asia Pacific, Bloomberg reported.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Talks between Coca-Cola European Partners (CCEP) and Sidney-based Coca-Cola Amatil are at an advanced stage and a deal announcement could be imminent within the next few days, according to the report. At the same time though, the deal structure has not yet been finalized and the transaction could still fall apart.

A deal between the two bottlers would be the largest involving an Australian company so far this year, according to data compiled by Bloomberg. Coca-Cola Amatil has a market value of about A$7.8 billion ($5.6 billion) with 32 production facilities in Australia, New Zealand, Fiji, Indonesia and Papua New Guinea, according to its website. UK-based Coca-Cola European Partners has a market value of about $17.7 billion.

Back in 2015, Coca-Cola European Partners was created from the three-way merger of Coca-Cola Enterprises Inc., Coca-Cola Iberian Partners and Germany’s Coca-Cola Erfrischungsgetranke. According to Bloomberg data, the largest shareholder is Cobega, an investment vehicle belonging to Spain’s Daurella family, followed by the US-based soda maker Coca-Cola Co. (KO).

The report of a potential deal for consolidation comes as soft drink bottlers are grappling with a decline in global demand for sugary drinks due to the impact of the coronavirus pandemic, which has increased the appetite for more healthy drinks and nutrition in general.

Earlier this year, Coca-Cola European Partners withdrew its buyback program and deferred a dividend to preserve cash. The soft drinks bottler’s shares have dropped 23% so far this year. (See CCEP stock analysis on TipRanks)

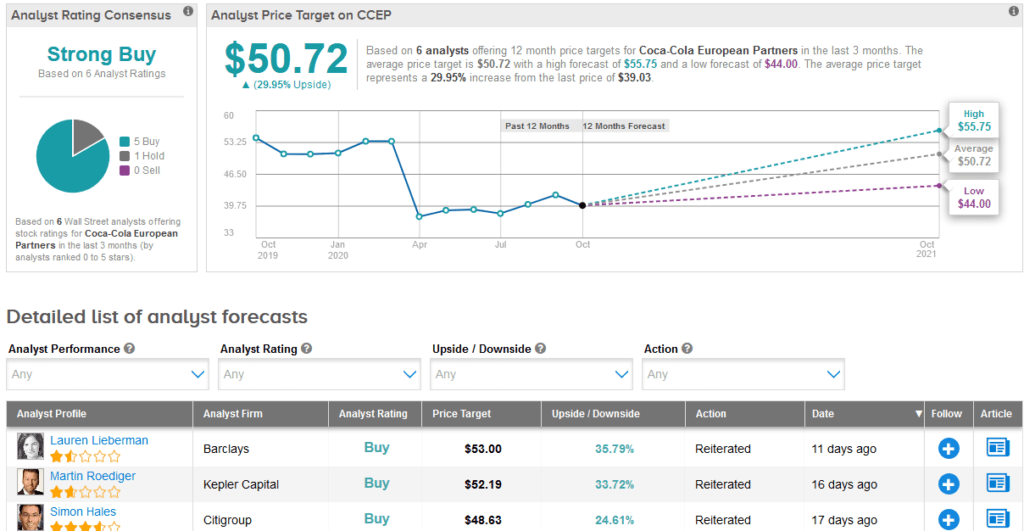

Meanwhile, the stock scores a bullish Strong Buy analyst consensus based on 5 Buy ratings versus only 1 Hold rating. That’s with a $50.72 average analyst price target, implying 30% upside potential lies ahead.

Related News:

American Express Hit With 40% Profit Slump; Shares Fall 3.6%

BJ’s Restaurants Shares Drop Despite 3Q Revenue Beat

Chipotle Falls 4% As Delivery Costs Drag Down 3Q Earnings