In the face of falling prices and economic uncertainty, steelmaker Cleveland-Cliffs (CLF) has been strategically positioning itself to weather the storm. While the stock is down 13% over the past year, the company is fortifying its market position through critical maneuvers such as acquiring Stelco Holdings (STLC). This move is projected to amplify Cleveland-Cliffs’ exposure to the flat-rolled steel market and potentially lead to substantial long-term gains.

Also, the company has been focusing on debt reduction and cost-cutting initiatives that could provide further financial resilience. The stock trades at fair value and is subject to inherent cyclical risks that can cause heightened volatility. However, it is a solid choice for investors interested in adding steel industry exposure to their portfolio.

Cleveland-Cliffs Expands Its Footprint

Cleveland-Cliffs is a leading flat-rolled steel producer in North America with a wide range of steel products, including hot-rolled, cold-rolled, electro-galvanized, and advanced high-strength steel. Additionally, it owns five iron ore mines in Minnesota and Michigan. Its vast product line caters to industries such as automotive, infrastructure and manufacturing, distributors and converters, and steel producers.

The company has agreed to acquire Canadian steel producer Stelco Holdings. The transaction, valued at approximately $2.5 billion, will be conducted through a stock-and-cash deal, with Cleveland-Cliffs paying C$70 per share for Stelco. As part of the deal, Stelco will continue to operate as a wholly-owned subsidiary of Cleveland-Cliffs, maintain its headquarters in Ontario, and plan to invest a minimum of C$60 million over the next three years. The United Steelworkers union supports the acquisition.

This strategic acquisition is set to expand Cleveland-Cliffs’ steel-making footprint, doubling its exposure to the flat-rolled spot market with cost advantages in raw materials, energy, healthcare, and currency. It is also expected to enhance earnings immediately while providing Cleveland-Cliffs an estimated $120 million in annual cost savings.

Cleveland-Cliffs’ Recent Financial Results & Outlook

The company recently reported Q2 results. Revenue was $5.1 billion, missing analysts’ expectations of $5.2 billion. Adjusted EBITDA reached $323 million, while the company generated an impressive $362 million free cash flow generation. Earnings per share (EPS) of $0.11 beat consensus expectations of $0.00.

Following second-quarter results, CLF’s management has lowered its capital expenditures guidance for the year to between $650 million and $700 million, down from the previously estimated $675 million-$725 million. Nonetheless, the organization’s ambitious target of slashing year-over-year steel unit cost by around $30/net ton remains a top priority.

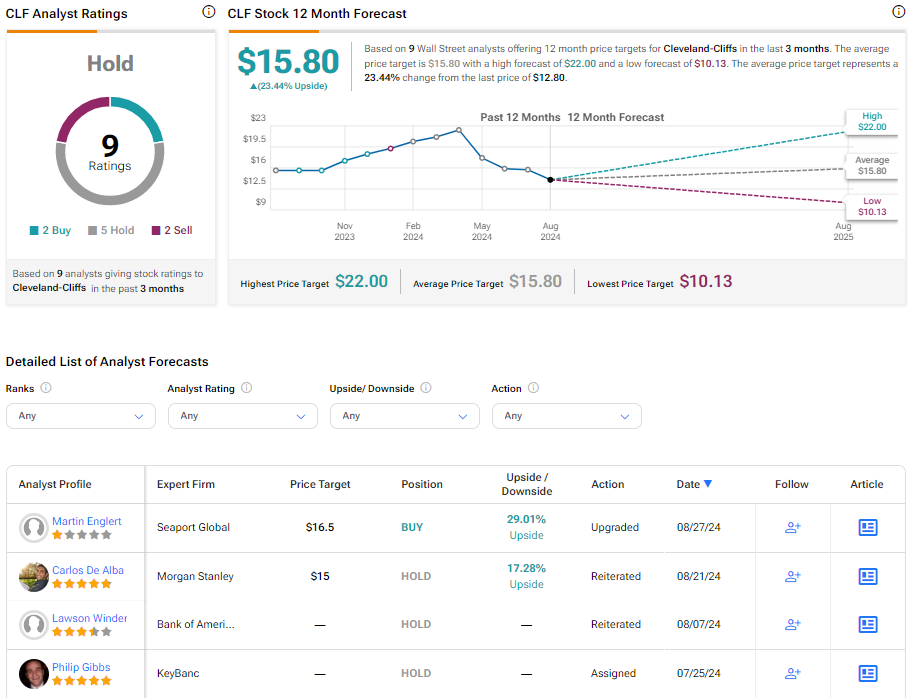

What Is the Price Target for CLF Stock?

The stock has been volatile, sporting a beta of 1.62 while bouncing around the past year, eventually shedding 13%. It trades at the low end of its 52-week price range of $12.39 – $22.97 and shows negative price momentum by trading below the 20-day (13.44) and 50-day (14.35) moving averages. The company’s P/B ratio of 0.86x aligns with the Steel industry average of 0.8x.

Analysts following the company have taken a cautious stance on the stock. For example, Seaport Research analyst Martin Englert recently upgraded the shares to Buy from Neutral with a $16.50 price target, noting the current steel price cycle, mounting supply-side response, and improving sentiment.

Based on the recommendations and price targets nine analysts have recently issued, Cleveland-Cliffs is rated a Hold overall. The average price target for CLF stock is $15.80, representing a potential 23.44% upside from current levels.

Closing Thoughts on CLF

Cleveland-Cliffs has proactively responded to market challenges by strategically amplifying its presence in the flat-rolled steel market, especially with its acquisition of Stelco Holdings. This move is expected to boost earnings while realizing substantial cost savings. The adjustments to capital expenditure guidance and continued commitment towards reducing steel unit costs further display strategic financial management. Trading at a fair value, the stock represents a solid investment opportunity for those seeking exposure to the steel industry.