Citigroup’s 1Q results topped analysts’ expectations, reflecting a release of allowance for credit loss (ACL) reserves, which resulted in lower costs of credit.

Citigroup’s (C) 1Q earnings more than tripled to $3.62 per share on a year-over-year basis and easily beat the Street estimates of $2.60 per share by a wide margin. Revenues decreased 7% to $19.3 billion but came in well ahead of analysts’ expectations of $18.82 billion.

The company’s Global Consumer Banking segment recorded revenues of $7 billion, down 14% year-over-year, impacted by reduction in card volumes and lower interest rates. Furthermore, revenues at the Institutional Clients Group segment fell 2% to $12.2 billion, as growth in Banking and Markets and Securities Services revenue was mostly offset by the lack of mark-to-market gains on loan hedges. (See Citigroup stock analysis on TipRanks)

The company reported total loans of $666 billion, down 8% from the prior-year quarter. Meanwhile, total deposits grew 10% to $1.3 trillion.

Citigroup CEO Jane Fraser commented, “As a result of the ongoing refresh of our strategy, we have decided that we are going to double down on wealth. We will operate our consumer banking franchise in Asia and EMEA solely from four wealth centers, Singapore, Hong Kong, UAE and London. This positions us to capture the strong growth and attractive returns the wealth management business offers through these important hubs. While the other 13 markets have excellent businesses, we don’t have the scale we need to compete.”

Following the 1Q results, Oppenheimer analyst Chris Kotowski increased the stock’s price target to $123 (69.6% upside potential) from $117 and maintained a Buy rating.

Kotowski said, “Citi’s 1Q21 results were solidly in line with our expectations; and on balance, trends were broadly in line with what we have seen from the other reporting banks. The bigger event, in our view, was Citi’s announcement that it would exit 13 consumer markets (mainly in Asia) to focus on wealth management in four—Hong Kong, Singapore, London, and the UAE.”

Furthermore, “We did not meaningfully change our model as near-term trends were generally as expected and the restructuring will likely take some time before impacting results. We continue to think the shares are deeply undervalued, and our $123 price target (up $6 from prior) is based on a 70% relative P/E, which should be attainable in any case, and we think there is upside to that over time,” the analyst added.

The rest of the Street is cautiously optimistic about the stock with a Moderate Buy consensus rating. That’s based on 9 analysts suggesting a Buy and 5 analysts recommending a Hold. The average analyst price target of $83.77 implies 15.5% upside potential to current levels. Shares have jumped 79% over the past year.

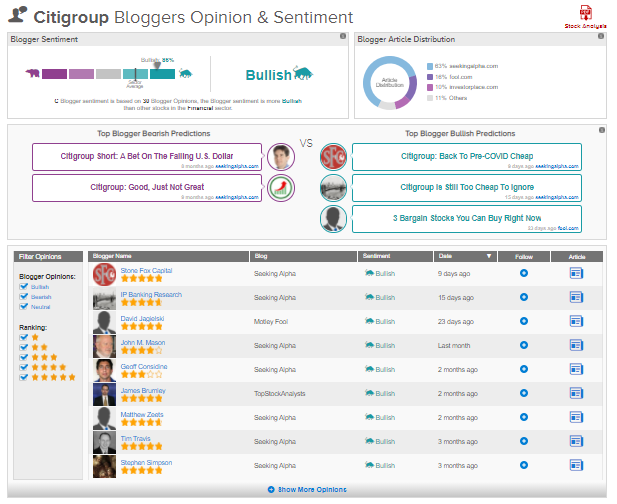

TipRanks data shows that financial blogger opinions are 86% Bullish on Citigroup, compared to a sector average of 70%.

Related News:

Goldman’s 1Q Results Exceed Expectations As Revenues Outperform; Shares Gain

JPMorgan’s 1Q Results Beat Estimates On Strong Revenues

Wells Fargo Jumps 5.5% After A Blowout Quarter, Fee Revenue Escalates