Shares of Cirrus Logic are spiking 8.4% in Tuesday’s pre-market trading session after the fabless semiconductor supplier delivered 2Q earnings of $1.26 per share that soared 137.7% year-over-year and exceeded the consensus estimate of $1.19 per share.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Cirrus’ (CRUS) 2Q sales declined 10.7% year-over-year to $347.3 million and missed the Street estimate of $354 million. However, 2Q sales surpassed the company’s guidance range of $290 – $330 million. The company’s outgoing CEO Jason Rhode said “We experienced solid sales across the breadth of our product portfolio, with particularly strong demand for components shipping in smartphones.”

As for 3Q, the company forecasts revenue in the range of $440 – $480 million, which is above the consensus estimate of $354.4 million. Cirrus anticipates GAAP gross margin in the range of 50%-52% for 3Q. (See CRUS stock analysis on TipRanks).

In addition, the company announced the appointment of John Forsytha as the new CEO of the company, who will replace Rhode effective from Jan. 1, 2021. Forsyth will also continue his role as president.

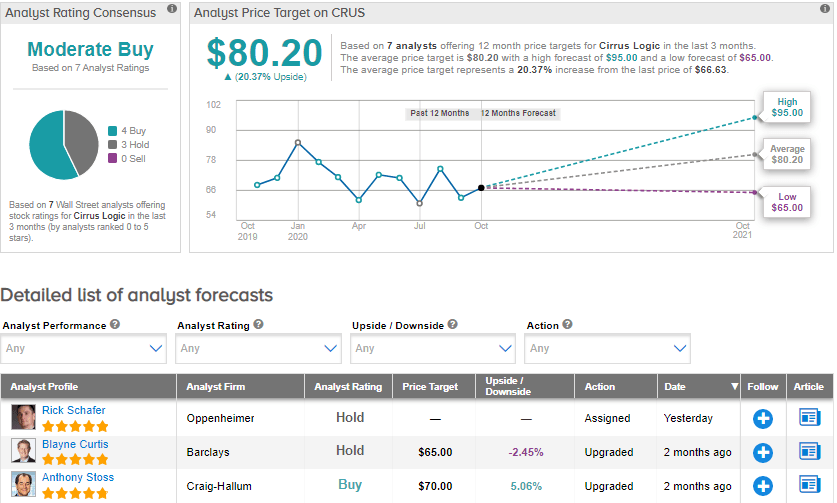

Following the results, Oppenheimer analyst Rick Schafer said that “the strong F3Q outlook reflects delayed iPhone12 launch and could portend a greater than normal seasonal decline in F4Q (Mar).” He added that “Incremental content from closed loop controller (CLC) win and higher units more than offset loss of inbox headset.” Schafer maintained a Hold rating on CRUS, given “customer concentration and limited visibility regarding future content gains.”

Currently, the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is based on 4 Buys and 3 Holds. The average price target of $80.20 implies upside potential of about 20.4% to current levels. Shares have declined 19.2% year-to-date.

Related News:

Skyworks Sees Upbeat 2021 Guidance After A Blowout 4Q

ON Semiconductor Quarterly Profit Beats The Street; Analyst Says Buy

Marvell To Snap Up Inphi In $10B Chip Deal