Network and communication infrastructure firm Ciena Corp. (CIEN) holds a clear advantage over rivals in the industry. The company beat top-and-bottom-line estimates thanks to continued growth in bandwidth and cloud demand, its dominant WaveLogic 6 Nano (WL6n), and its shift toward fiber access services in recent quarters. For those reasons, I am bullish on CIEN stock despite management lowering its revenue guidance for the remainder of 2024.

The networking systems industry has struggled post-COVID with a backlog of inventory. However, Ciena’s strong market share and new venture into fiber access have helped mitigate this issue, setting it up for potential success in the near term at a time when peers are still seeking stabilization.

These are some of the reasons why analysts on Wall Street predominantly view CIEN shares as a Buy. I echo this sentiment, even as the company’s share price has fallen substantially since its high above $62 in March of this year. Below, we look in more detail at the factors driving analysts’ optimism about Ciena.

Demand Growth and Strong Set of Products

As stated above, I am bullish on Ciena. It is well-positioned to capitalize on the rapid growth in demand for cloud and bandwidth, which is expected to continue for years. The global cloud infrastructure market was estimated to be $233.91 billion last year and is predicted to grow at a CAGR of over 12.10% through 2032.

In addition, Morgan Stanley analyst Meta Marshall expects cloud segment growth to contribute significantly to Ciena’s performance in fiscal 2025. Moreover, due to surging demand, Ciena enjoys a substantial market share in the niche communication infrastructure space, and Marshall sees room for additional market share gains going forward.

A big factor in my bullishness is Ciena’s WaveLogic 6 optical technology product, which the company launched early in 2023 and could continue to bolster its market share. It provides industry-leading wavelengths of 1.6 Terabits and a reach of up to 1,000 km for 800G pluggable.

This product likely has more untapped potential even a year and a half after its launch. For example, the JUNO submarine cable system operators, which provides network connectivity between the U.S. and Japan, announced in June this year that they would deploy WaveLogic 6 to the project to boost network capacity.

Ciena’s Foray Into Fiber Access

Another important consideration is Ciena’s aggressive expansion into the fiber access business. Following the National Telecommunications and Information Administration’s rollout of the Broadband Equity, Access, and Deployment Program (BEAD) in 2022, BEAD provides more than $42 billion to expand high-speed internet access nationwide. Ciena has forecasted that the fiber broadband access market will grow at a massive 55% CAGR to reach $7 billion by 2027, largely thanks to public funding support.

Although well-established in other communications infrastructure areas, Ciena is new to the fiber access space. In 2022, it accelerated its expansion into this market by acquiring two related companies, Tibit Communications and Benu Networks.

With these acquisitions and given its pre-existing work in long-haul networks, Ciena could be positioned to benefit from its participation in the BEAD program in the near term. One advantage it has over more established competitors is its pluggable optical line terminal (OLT) products. While OLTs are typically installed in central offices or remote cabinets, Ciena has developed a smaller product to hang on telephone pole strands.

Ciena’s micro-OLTs are well-suited to rural locations and do not face the same excess inventory issues plaguing long-standing competitors because they were newly developed post-COVID.

Ciena’s Earnings Beat

How the continued deployment of Ciena’s fiber access business will impact the company’s top-and-bottom-lines remains to be seen. In June, the company reported fiscal second-quarter profit and revenue that each came in below the prior year. Also, Ciena lowered its full-year Fiscal 2024 revenue guidance to $1 billion from $4-4.3 billion.

While this is a sizable downgrade, it does not consider the potential upside from increased data center business or the benefits of Ciena’s new fiber access efforts described above. Furthermore, the company’s second-quarter profit and revenue still beat consensus estimates.

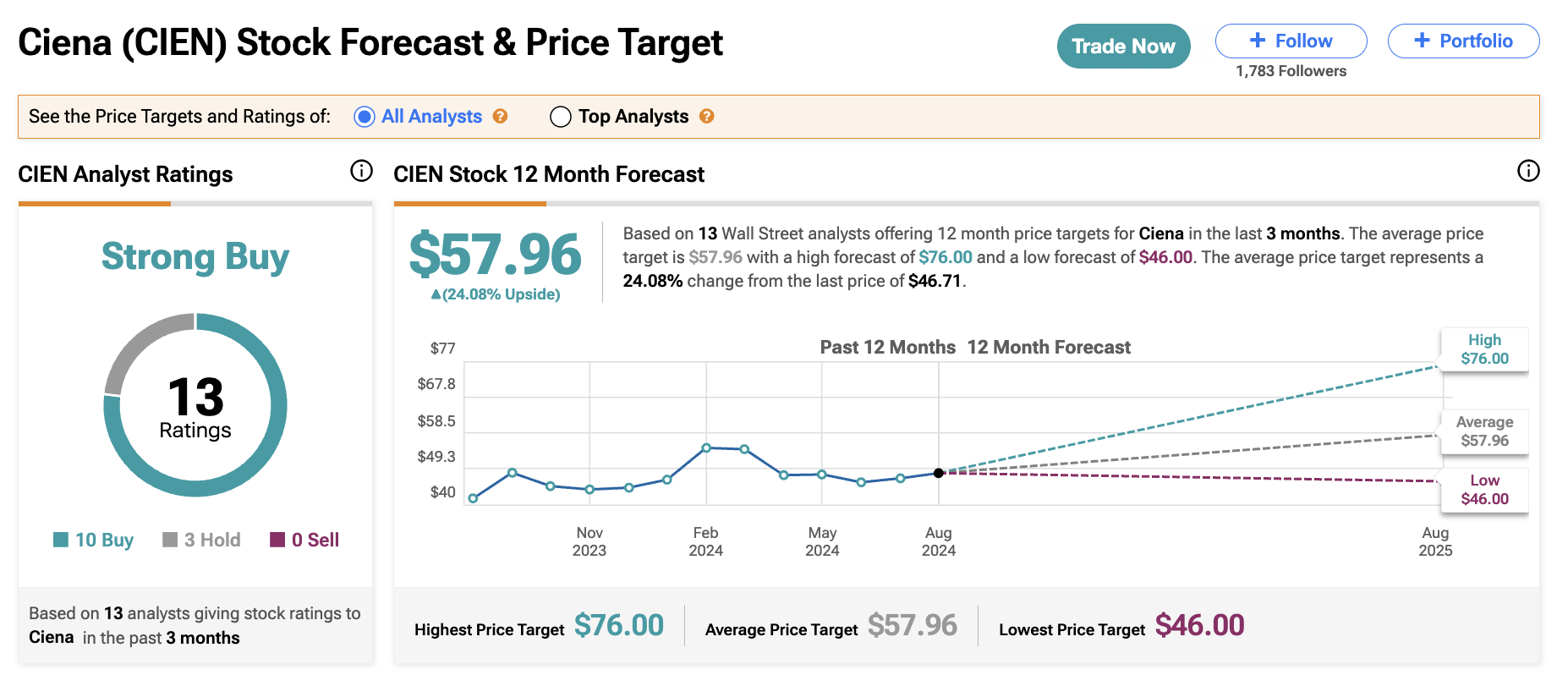

For these reasons, I feel strongly about CIEN stock, as do Wall Street analysts who recommend Ciena and indicate that the stock is a Strong Buy. This is based on 10 Buy ratings, three Hold Ratings, and zero Sell Ratings. Analysts see an upside potential of 24% based on an average price target of $57.96. Ciena shares are up just over 14% in the last year.

Conclusion: Room for Growth

In conclusion, Ciena’s strong position in the industry will benefit the company from the expected blossoming of the future data center and fiber access markets. The company’s relatively recent venture in fiber access has given it advantages over long-standing competitors in the space. Its dominant WaveLogic 6 product and micro OLTs also help to differentiate it from rivals. Although the company has lowered its guidance for the rest of 2024, it does not consider the potential upside of its new access to the fiber business. That is why I am bullish on CIEN stock.