Children’s Place surpassed Street expectations both on the revenue and earnings front on the back of robust digital sales in 4Q. Shares of the children’s specialty apparel retailer closed about 3% higher on Tuesday.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The Children’s Place (PLCE) reported 4Q earnings of $1.01 per share, significantly higher than analysts’ expectations of a loss of $0.23 per share. However, earnings declined 45.4% year-over-year due to lower sales and a fall in gross and operating profits.

Sales decreased 7.8% to $472.9 million but exceeded consensus estimates of $421 million. Digital sales increased 38% and accounted for 46% of total sales in 4Q.

During the quarter, the company closed 60 stores, bringing total store closures to 178 in 2020. Furthermore, the company plans to close an additional 122 stores in 2021, with 25 store closures planned in 1Q. (See Children’s Place stock analysis on TipRanks)

The company’s CEO, Jane Elfers, said, “With no significant COVID-19 temporary U.S. store closures during the quarter, U.S. store sales were better than expected at 81% of last year’s levels with traffic down approximately 35%.”

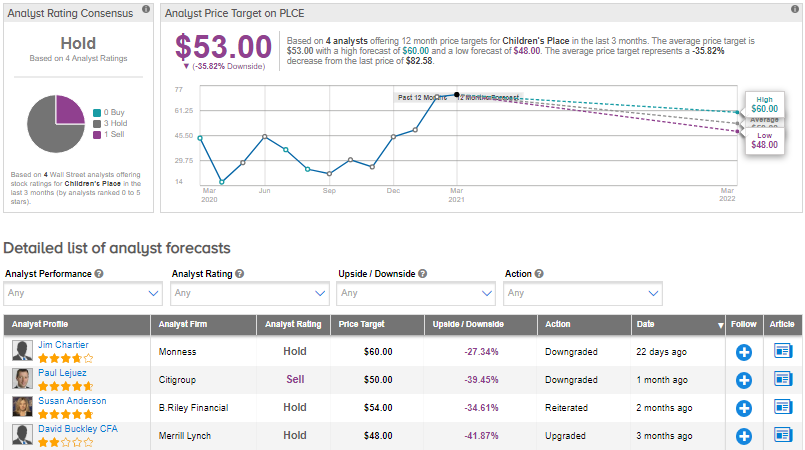

On Feb. 16, Monness analyst Jim Chartier downgraded Children’s Place stock to Hold from Buy explaining that it has exceeded his price target of $60 (27.3% downside potential). However, the analyst sees “meaningful earnings power.”

Turning now to the rest of the Wall Street community, Children’s Place has a Hold consensus rating based on 3 Holds and 1 Sell. The average analyst price target of $53 implies downside potential of about 36% to current levels. Shares have gained around 76% in value over the past year.

Related News:

Stitch Fix Plummets 22% In Pre-Market On Softer FY21 Revenue Outlook

Waitr Disappoints With 4Q Results; Shares Slide 15%

ContextLogic’s 1Q Revenue Outlook Exceeds Expectations After 4Q Beat; Shares Rise