Chewy reported better-than-expected 3Q results. However, shares of the online pet-products retailer dropped 1.3% in Tuesday’s extended trading session after closing 5.8% higher on the day.

Chewy (CHWY) posted a 3Q loss of $0.08 per share, smaller than analysts’ projections of a loss of $0.13 and the year-ago loss of $0.20. The company’s 3Q revenues rose 45% to $1.78 billion and exceeded the consensus estimates of $1.72 billion. That compared with a guidance range of $1.70 billion – $1.72 billion. Chewy added 1.2 million net active customers in 3Q, ending the quarter with 17.8 million active customers.

Further, the company raised its sales guidance for the full year, reflecting accelerated demand and increased spending by customers. Chewy expects to generate 2020 revenues of between $7.04 billion – $7.06 billion, which represents year-over-year growth of 45% – 46%. Previously, the company had projected revenues to be $6.775 billion and $6.825 billion. As for 4Q, the company anticipates revenues in the range of $1.94 billion – $1.96 billion, which implies year-over-year growth of 43% to 45%.

Chewy’s CFO Mario Marte said during the earnings call, “While some potential cost headwinds remain, these mostly reflects short-term impacts directly related to COVID or it’s temporary effects on areas like labor and logistics.” (See CHWY stock analysis on TipRanks)

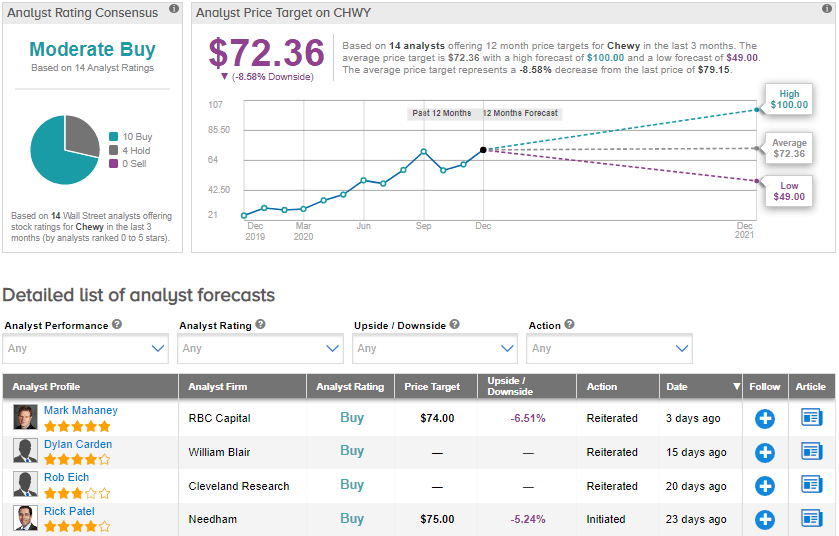

On Nov. 16, Needham analyst Rick Patel initiated his coverage on the stock with a Buy rating and a price target of $75 (5.2% downside potential). The analyst said, “CHWY is strongly positioned to gain new customers, drive retention through subscription, and capture wallet share as newer cohorts mature and spend more. The result is a growing base of customers who drive compounding growth.”

He added that, “The pandemic undoubtedly accelerated CHWY’s growth and margin progress, but we believe the backdrop will remain favorable post-Covid given the growing TAM [total addressable market] for the pet product & services market and ongoing digital adoption.”

Meanwhile, the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is based on 10 Buys and 4 Holds. With shares up 172.9% year-to-date, the average price target stands at $72.36 and implies downside potential of about 8.6% to current levels.

Related News:

Smartsheet Soars 17% On 4Q Guidance Beat After 3Q Win; Needham Raises PT

Coupa Lifts FY21 Outlook After 3Q Beat; Analyst Raises PT

Sumo Logic Jumps 6% On 4Q Outlook; BTIG Says Buy