Chewy (CHWY), the online pet product retailer, saw its stock jump over 7% after its chief financial officer highlighted the company’s low reliance on Chinese imports. Speaking at a Morgan Stanley investor event, CFO David Reeder said Chewy sources most of its products domestically, keeping the company safe from rising tariffs.

Meanwhile, Bank of America echoed this sentiment, naming Chewy as one of the e-commerce companies least exposed to tariff risks. “Our top stocks for least tariff exposure are Chewy,” with less than 10% from China, analysts led by Justin Post wrote. The firm kept its “Buy” rating and a $40 price target on Chewy, signaling more room for gains.

Premium Pet Products Fuel CHWY’s Growth

Reeder also pointed to the booming “premiumization” trend as a major growth driver. He noted that pets are like family, which makes people more willing to spend on higher-quality products. He added, this “humanization” of pets is not only continuing but picking up speed, providing a clear boost for Chewy.

Moreover, pet owners are willing to pay more for safety and quality, especially when it comes to food. Past recalls linked to Chinese suppliers have made shoppers more cautious, giving Chewy’s mostly domestic supply chain a clear edge.

Limited China Exposure Shields Chewy from Tariff Risks

Chewy’s minimal reliance on China offers an added layer of protection. Reeder previously told analysts that only a small portion of their products, mainly hard goods, come from China, while most pet food and other top-selling items are sourced locally.

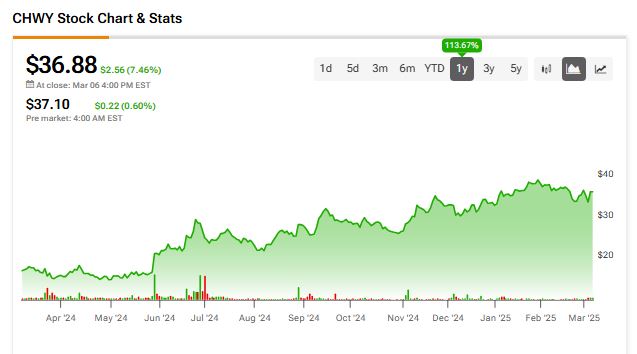

With steady consumer demand and limited tariff risks, Chewy remains well-positioned in the e-commerce space. Notably, the stock has climbed 113.7% over the past year and is up 10% year-to-date, reflecting investor confidence in its growth potential.

Is CHWY a Good Stock to Buy?

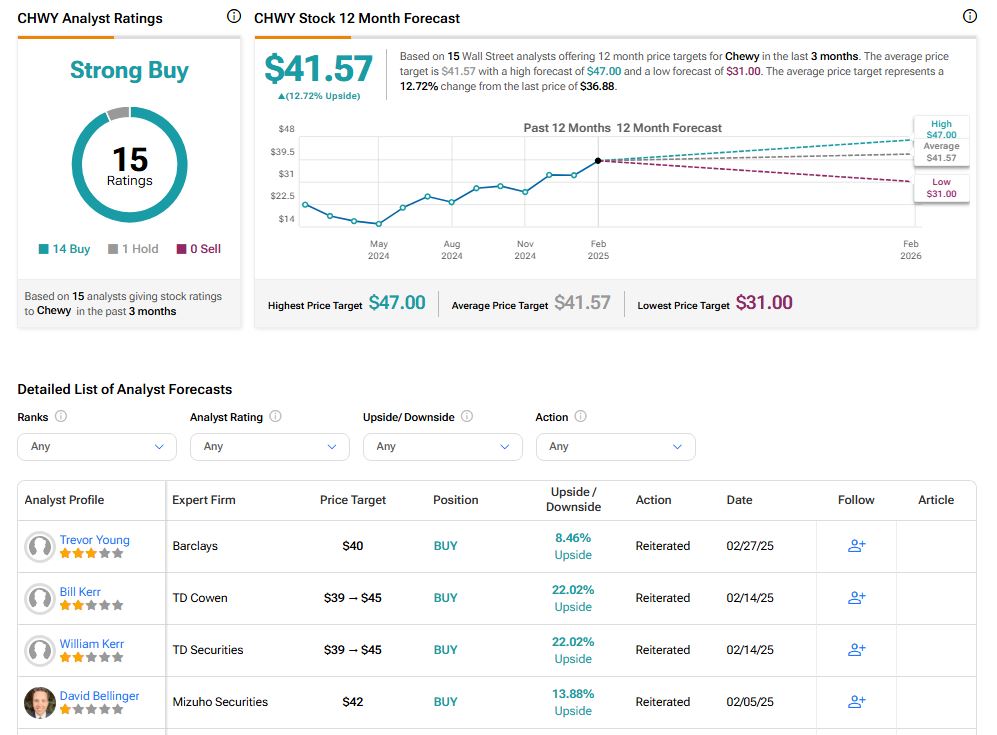

Turning to Wall Street, CHWY has a Strong Buy consensus rating based on 18 Buys and four Holds assigned in the last three months. At $41.57, the average Chewy price target implies 12.72% upside potential.