Chegg, reported better-than-expected 2Q earnings on Monday, as the technology-based learning platform, benefited from stronger demand due to the coronavirus-led stay-at-home directives.

Chegg’s (CHGG) adjusted EPS jumped 61% to $0.37 year-on-year and beat analysts’ expectations of $0.32. Its 2Q revenues soared 63% to $153 million year-over-year and surpassed Street estimates of $136.6 million. Further, its subscriber base increased by 67% to 3.7 million year-over-year.

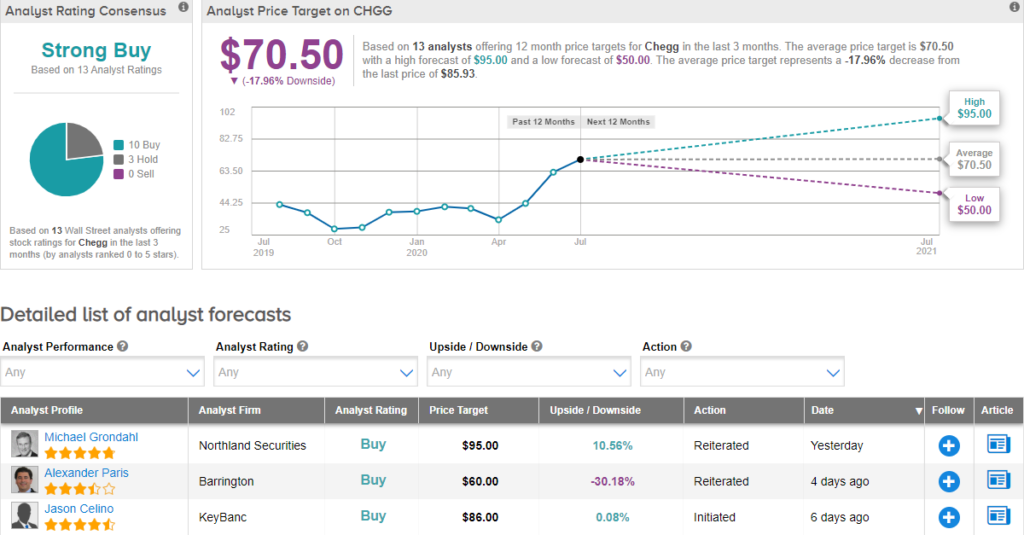

Five-start analyst Michael Grondahl of Northland Securities said, “Chegg saw increased engagement with students going online and renewals were up and cancellations down with a record number of questions and subjects in the quarter”. He added, “CHGG’s efforts to restrict password sharing is still a multi-quarter benefit.” Grondahl maintains his Buy rating on CHGG with a price target of $95 (10.6% upside potential).

Currently, CHGG has a Strong Buy analyst consensus. Its stock has surged nearly 127% year-to-date, so it is not surprising that the average price target of $70.50 implies downside potential of 18%. (See CHGG stock analysis on TipRanks)

Related News:

Sorrento’s New COVID-19 Test Could Be a Game Changer, Says 5-Star Analyst

After Amazon Trounces 2Q Estimates, 5-Star Analyst Says There’s More to Come

Challenges Ahead, but Facebook Stock Will March On, Says 5-Star Analyst