The electric vehicle (EV) infrastructure company ChargePoint Holdings (CHPT) reported a larger-than-expected loss in Q1. However, revenue came in better-than-expected as the company announced a record number of new customers. CHPT shares rose 7% to close at $28.11 on June 4.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

The company incurred a loss of $0.84 per share in Q1 compared to the $0.10 loss per share estimated by analysts.

Meanwhile, revenue generated in the quarter was $40.5 million, which grew 24% from the year-ago period and beat analysts’ expectations of $35.85 million.

ChargePoint CEO Pasquale Romano said, “We expect an acceleration in our business as EV penetration increases and economies in our key markets reopen. Our strong balance sheet and capital light business model position us to continue leading the EV charging industry.” (See ChargePoint stock analysis on TipRanks)

For Q2, the company expects revenues in the range of $46 – $51 million. The consensus estimate sits at $45.2 million.

For 2021, revenues are expected to land between $195 and $205 million versus the consensus estimate of $203.9 million.

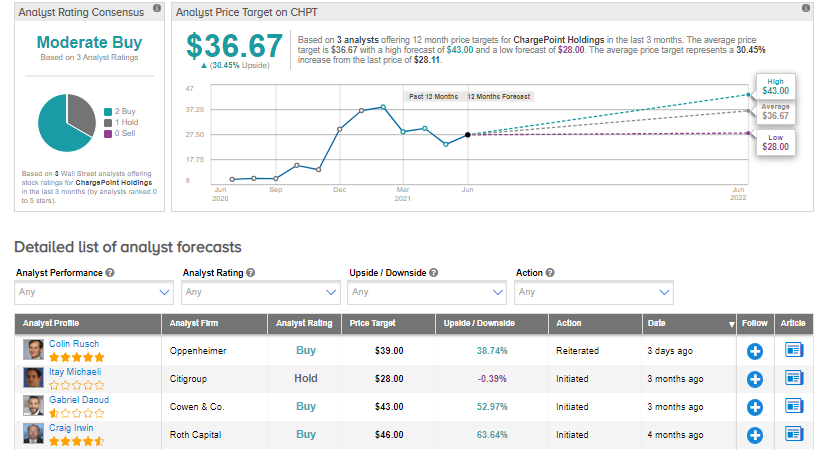

Following the earnings announcement, Oppenheimer analyst Colin Rusch reiterated a Buy rating and a price target of $39 (38.7% upside potential).

Rusch commented, “We are encouraged to see improving sales traction in Europe and with its DC fast charging solution, which we expect to carry advantaged margins as volumes scale up.”

He further added, “We note the company’s customer relationships are growing well with 5K new customers in the quarter and re-buy rates at 60%. We continue to believe the company’s controls and buffering capabilities in its solutions are underappreciated as we believe these functionalities ease permitting, lower balance of systems expense, and optimize performance.”

The rest of the Street is cautiously optimistic about the stock with a Moderate Buy consensus rating based on 2 Buys versus 1 Hold. The average analyst price target of $36.67 implies 30.5% upside potential to current levels. Shares have decreased 22.7% over the past six months.

Related News:

DocuSign Gains on Better-than-Expected Q1 Results

Broadcom Reports Better-than-Expected Q2 Earnings on Solid Chip Demand

MongoDB Reports Smaller-than-Expected Q1 Loss, Revenues Beat Estimates