Caterpillar (NYSE:CAT) stock appears poised to achieve record profits in FY2024, which is likely to power a bullish rally from its current levels. Although shares have experienced a modest decline since early April, likely due to investors capitalizing on last year’s substantial gains, the recent dip presents a compelling entry point. The company’s solid sales and growing earnings indicate that Caterpillar is likely undervalued, forming an attractive opportunity for prospective investors. Consequently, I am bullish on the stock.

Q1-2024: Starting the Year on a High Note

At first glance, Caterpillar’s Q1 results may seem mixed. Nevertheless, I believe they are quite impressive with proper context, especially given the explosive growth in recent years. Specifically, in FY2021, FY2022, and FY2023, Caterpillar achieved revenue growth of 22.1%, 16.6%, and 12.8%, respectively. While the lack of growth at the start of FY2024 might appear concerning, the company’s ability to sustain revenues near record levels is remarkable despite its cyclical nature. Let’s take a deeper look.

In its Q1 results, Caterpillar reported revenues that displayed growth and contraction across its various segments, which ultimately offset each other. Total sales came in at $15.8 billion, relatively flat compared to the same period last year but still near record levels.

Specifically, the Construction Industries segment saw a 5% decrease in sales, amounting to $6.4 billion. This decline was primarily driven by lower sales volumes, although favorable price realizations partially offset the drop. While North America was a bright spot within this segment, posting 6% growth, this was more than offset by Europe and Asia Pacific posting notable declines of 25% and 14%, respectively.

The Resource Industries segment also experienced a decline in sales, which slipped by 7% to $3.2 billion, largely due to reduced equipment sales to end users. Nevertheless, the Energy & Transportation segment demonstrated robust growth, with sales increasing by 7% to $6.7 billion. This growth was driven by higher sales volumes and favorable pricing, particularly in Power Generation, which surged by 26%, and Oil & Gas, which rose by 19%.

Margins, Profitability, Valuation

Despite the somewhat flat sales in Q1, Caterpillar’s report showcased exceptional progress in margins and profitability. Smart cost management and favorable market conditions resulted in Caterpillar’s adjusted operating profit landing at 22.2% (or 22.3% on a GAAP basis), up 110 basis points compared to last year, with positive contributions across every segment. This led to a substantial increase in operating profits.

Let’s break it down:

- The Construction Industries segment reported a margin of 27.5%, a 100-basis-point improvement from the previous year, primarily due to favorable manufacturing costs and pricing strategies.

- Similarly, the Resource Industries segment saw its margin increase by 60 basis points to 22.9%, driven by favorable pricing and lower freight costs.

- Finally, the Energy & Transportation segment posted a margin of 19.5%, up 260 basis points from Q1 of 2023.

Caterpillar’s operating profit growth in Q1 drove net earnings growth despite the fairly flat sales. Along with the continuous repurchases, which lowered its share count, Caterpillar’s adjusted earnings per share (EPS) increased by 14.1% to $5.60. Thus, you can see why Caterpillar has set the stage for another year of record profits.

Wall Street is more cautious, predicting a modest 2.2% increase in EPS to $21.68 for FY2024, suggesting slightly softer margins in the upcoming quarters. Nevertheless, Caterpillar’s ability to consistently elevate EPS to new records year after year, despite its cyclical nature, is quite commendable and exposes the fact that the stock is still trading at a rather cheap valuation.

At a forward price-to-earnings (P/E) ratio of 15.2 times, according to this year’s expected EPS, Caterpillar appears to be attractively priced. This is especially true considering its overall qualities, market-leading positions, and the fact that Wall Street expects further EPS growth in the coming years.

Is CAT Stock a Buy, According to Analysts?

Looking at Wall Street’s view on the stock, Caterpillar has a Moderate Buy consensus rating based on nine Buys, six Holds, and one Sell assigned in the past three months. At $371.57, the average Caterpillar price target suggests 12.4% upside potential.

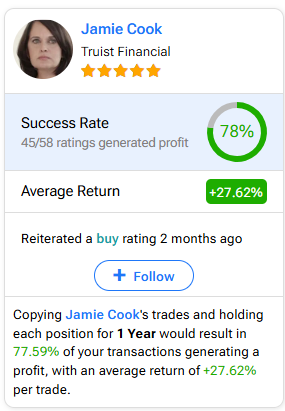

If you’re unsure which analyst you should follow if you want to trade CAT stock, the most profitable analyst covering the stock (on a one-year timeframe) is Jamie Cook from Credit Suisse, with an average return of 27.62% per rating and a 78% success rate. Click on the image below to learn more.

The Takeaway

Despite what seems to be a mixed start to FY2024 revenues-wise, Caterpillar managed to sustain near-record revenues following three years of outsized growth. In the meantime, the company continued to expand its margins, driving double-digit earnings growth. Even if margins contract later in the year, FY2024 is likely to achieve another year of record EPS. This bolsters the stock’s investment case following its recent dip. The chance of a bullish rally from its current levels, in fact, seems rather strong.