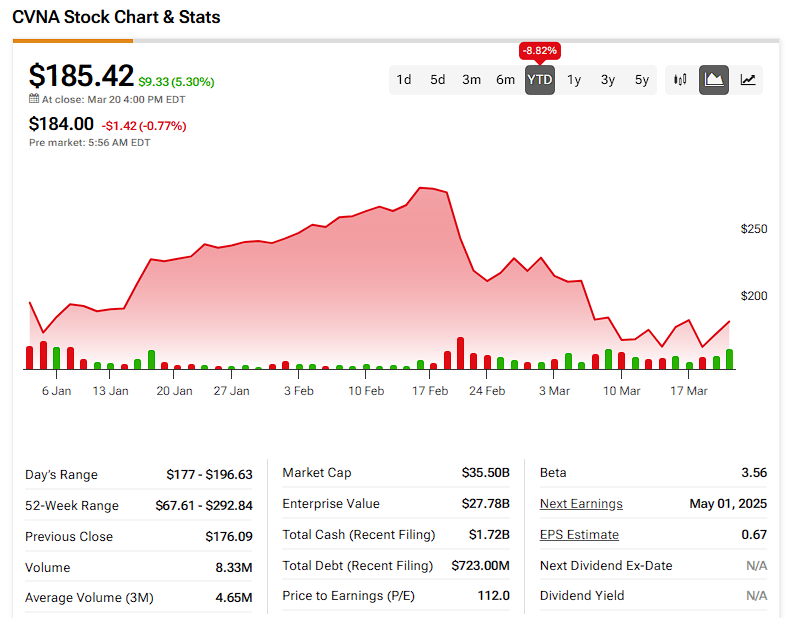

Used car e-commerce platform Carvana Co. (CVNA) staged an almighty bullish run throughout 2024, climbing from lows around $40 to a peak of over $250 per share late last year. However, in 2025, the stock is down 9%, with souring sentiment driven by weaker performance figures. Could this be an early-stage buy-the-dip opportunity for the plucky car reseller?

Just two years ago, CVNA traded in the single digits and was subject to bankruptcy rumors. The online-only used-car retailer, best known for its “car vending machines,” rose from the ashes last year after its revenues and profit margins markedly improved. While Carvana’s Q4 earnings report exceeded revenue and EPS expectations, it wasn’t enough to appease the market. Moreover, company-specific news and macroeconomic factors contributed to volatility and negative sentiment.

While Carvana’s financial situation is far removed from the fears of 2023, a closer look under the hood reveals some challenges ahead, causing me to lean bearish. Far from being a buy-the-dip pickup, CVNA stock has more room to descend, making it a bearish shorting opportunity.

Carvana Delivers Stunning Retail Growth in Q4

Carvana had a strong finish to 2024. In Q4, it sold 114,379 cars, a 50% increase from the previous year. Revenue reached $3.6 billion, up 46% year-over-year. Since Carvana operates in the used-car market, its business is capital-intensive, leading to smaller profit margins. The company’s cost of sales was $2.8 billion, giving it a 21% profit margin—well above the typical 10% to 15% margins in the industry. Operating expenses, including selling, general, and administrative costs (SG&A), totaled $494 million. Despite these expenses, Carvana reported a net income of $159 million for the quarter.

Turning to the balance sheet—a major focus among investors due to the company’s historically high net debt—Carvana continues to deleverage or reduce its debt. Notably, its debt-to-assets ratio has fallen well under 100%. Notably, CVNA’s price-to-cash flow (P/CF) ratio is 147.9, indicating that investors are paying a hefty premium—almost 148 times the amount of cash flow the company generates—for each dollar of the company’s cash flow.

This ratio indicates how much of the assets are financed by creditors. Anyone who’s purchased a new car with a loan knows how heavy the interest can weigh on the monthly payment. So, it’s better to own the car yourself.

Carvana Faces Financial Uncertainty

While the balance sheet has improved, Carvana is not out of the financial woods yet. In Q4, Carvana raised $924 million of equity through its at-the-market (ATM) program. While this helps with its debt situation, it comes at the expense of investors in the form of dilution. Essentially, investors are left with a smaller piece of the pie.

The day following its Q4 earnings report, Carvana amended its ATM program. Although it has no obligation to do so, the agreement allows the company to offer up to $1 billion in equity. This may have spooked investors and reminded them of the long road ahead for Carvana.

Macro Headwinds and Competitive Threats Cloud CVNA’s Outlook

Carvana relies on macroeconomic factors like interest rates, the used car market, and economic headwinds. While used car sales and prices are expected to modestly increase in 2025, high used car loan rates could deter buyers. The Federal Reserve’s decision in March to maintain federal fund rates at 4.5%, signaling a continuation of the pause in rate cuts, didn’t help bring down used car interest rates, which average as high as 14% APR.

Carvana is also very sensitive to consumer spending. The ongoing “trade war” and the projected slowdown in economic growth do not foreshadow heavy wallets.

Lastly, Amazon is interested in expanding its new-car online platform to include used cars, potentially becoming a competitor to Carvana. However, unlike Carvana, Amazon apparently has no intention of providing delivery or reconditioning. As a bullish analyst from BofA notes, such a move is unlikely to be “directly competitive.”

Is Carvana Stock a Buy, Sell, or Hold?

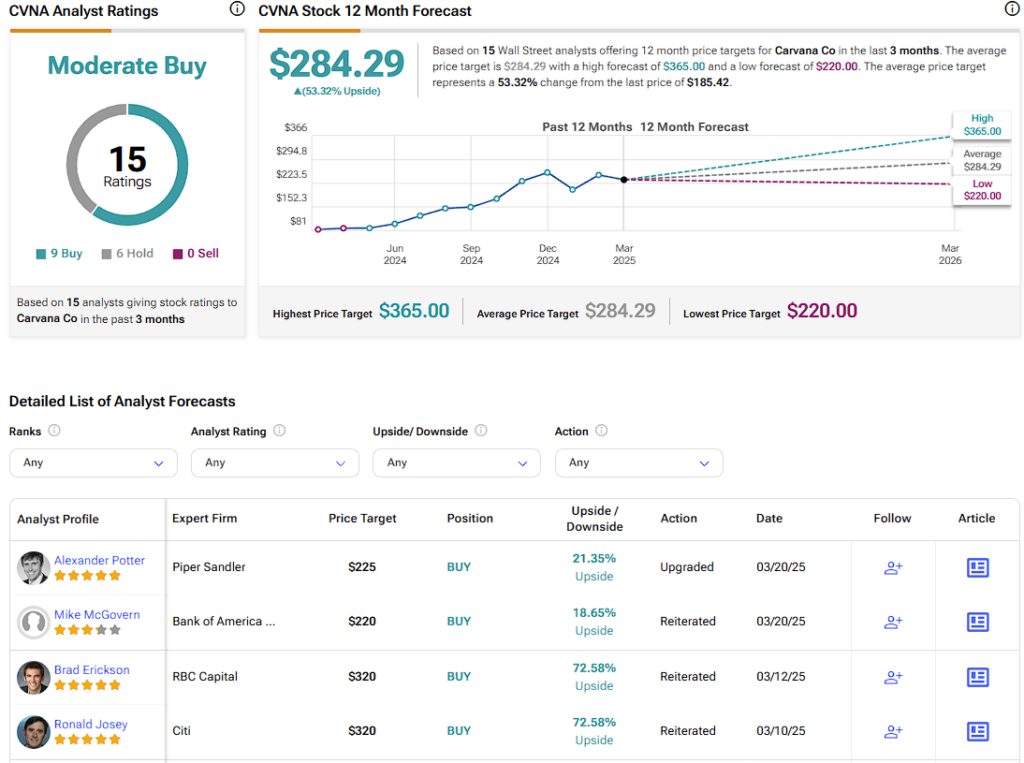

On Wall Street, CVNA stock carries a Moderate Buy consensus rating based on nine Buy, six Hold, and zero Sell ratings over the past three months. CVNA’s average price target of $284.29 per share implies approximately 53% upside potential over the next twelve months.

Following its Q4 earnings last month, analyst David Lantz from Wells Fargo maintained his “Buy” rating and price target of $310 on CNVA stock, citing “strategic moves, such as ADESA site integrations,” as well as “improvements in inventory selection and a reduction in average delivery times.” He noted some challenges, too, like interest rates, market expectations, and “uncertainties around future growth metrics.” This sentiment echoes my own beliefs. However, Carvana’s sky-high valuation and heavy reliance on macroeconomic trends outweigh its operational and financial progress in the past year.

Bullish Fatigue Amid Market Volatility

While Carvana’s 2024 performance was superb, its stock performance following its Q4 earnings implies that the market had irrationally high expectations. While its revenues grew at an impressive clip (27% year-over-year) in 2024, cash generation remains relatively small, and the company still relies on stock offerings to smooth out the balance sheet.

Moreover, Carvana’s performance depends on external factors they cannot control, like interest rates, economic headwinds, and consumer spending habits. Also, remember that Carvana’s stock is extraordinarily sensitive, as evidenced by a stock beta of 3.56. This means that for every 1% move by the market, CVNA rises or falls by approximately 3.56%. So, if there’s one thing certain in 2025 for Carvana, it is volatility, and I’d instead not join along for the ride.

Questions or Comments about the article? Write to editor@tipranks.com