E-commerce has become more dominant than ever as consumers are cautious about shopping in stores due to the COVID-19 pandemic. It is not just groceries and home merchandise that are being increasingly purchased online. More US consumers are buying cars on digital platforms since the pandemic. Notably, the demand for used cars has increased considerably as many people are avoiding public transportation due to COVID fears. Also, high unemployment and challenging macro conditions are driving the demand for used cars in comparison to new cars.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

There are two categories of companies involved in online car sales. Companies like Cars.com and CarGurus provide an online marketplace that connects buyers and sellers of new and used cars. On the other hand, Carvana and Vroom remove the dealer from the picture and deal directly with the customer.

Against this backdrop of the growing demand for the online car market, we will use the TipRanks Stock Comparison tool to place Cars.com and Carvana alongside each other and see which online car stock offers a better investment opportunity.

Cars.com (CARS)

Cars.com is a digital marketplace and solutions platform that connects car shoppers with sellers. The company also has other platforms including DealerRater (car dealer review and reputation management platform) and Fuel (a digital video solution for dealers that helps them target Cars.com’s in-market car shoppers).

CARS is benefiting from the consumers’ growing need to connect with dealers digitally amid the pandemic. Last week, the company announced better-than-expected preliminary numbers for 3Q, projecting revenue between $142 million and $144 million, Y/Y growth in adjusted EBITDA and an adjusted EBITDA margin between 33% and 34%.

Currently, CARS expects net loss between $10 and $12 million in 3Q, primarily reflecting a non-cash charge of $31 million for the correction of an error related to the calculation of the valuation allowance for income taxes in connection with an impairment recorded in 1Q.

Meanwhile, the midpoint of the company’s revenue guidance reflects top-line growth of 40% in 3Q compared to the second quarter but a Y/Y decline of 6%. The company also disclosed that it is working on reducing its leverage and had $598 million in outstanding debt at the end of 3Q after paying down $48 million in the quarter.

In 2Q, CARS’ revenue declined 31% Y/Y to $102 million and monthly average revenue per dealer or ARPD fell 33% to $1,442 due to the financial relief given to dealer customers as a result of COVID-19. Adjusted EBITDA fell about 47% to $23.2 million. (See CARS stock analysis on TipRanks)

In reaction to the 3Q preliminary numbers, B. Riley Securities analyst Lee Krowl increased the price target on Cars.com stock to $11 from $9 and upgraded it to Buy from Hold due to better-than-expected net dealer growth and proactive debt repayments.

Craig-Hallum analyst Steven Dyer also upgraded the stock to Buy from Hold and raised the price target to $14 from $12. The analyst noted that the company reported EBITDA growth for the first time since 2016 and added about 100 net dealers in 3Q giving him more confidence in the forward business fundamentals. Dyer also feels that the valuation is attractive.

Looking ahead, the company intends to ramp up it’s marketing efforts to capture the growing demand. It also expects its FUEL platform to positively contribute to revenue and profitability with ARPD rates that are multiples higher than the company’s overall ARPD.

The Street is cautiously optimistic about Cars.com with 4 Buys and 2 Holds adding to a Moderate Buy consensus. Shares have declined 30% so far but could rise about 37% in the coming months as indicated by the average analyst price target of $11.67.

Carvana (CVNA)

Leading used-car online seller Carvana is witnessing robust growth due to strong demand for used cars during the pandemic and the growing adoption of online shopping for cars. It struggled in mid-March when the pandemic started spreading rapidly and faced inventory issues as well. However, the top-line began to rebound in late April and the company’s 2Q revenue grew 13% Y/Y to $1.12 billion. Carvana sold 55,098 retail units in 2Q, reflecting a 25% Y/Y increase.

However, the company’s EBITDA loss widened to $69 million in 2Q20 from $35.9 million in 2Q19. Meanwhile, Carvana expanded to 100 new markets in the quarter, thus increasing the total percentage of the US population it serves in its 261 markets to 73.2% from 68.7% at the end of 1Q20.

Carvana buys, reconditions and sells used cars. The company recently launched its ninth Inspection and Reconditioning Center or IRC near Columbus, Ohio. This facility increases the company’s annual production capacity to nearly 500,000. Carvana expects to open two more IRCs by the end of this year, which will boost its capacity by 100,000. Over the long-term, the company aims to have an annual production capacity of over 2 million.

In June, the company launched CarvanaACCESS, a direct-purchase platform that gives wholesale buyers access to Carvana’s inventory.

Last month, Carvana provided a business update and stated that it expects to deliver record performance in 3Q in key metrics, including retail units sold, total revenue, total gross profit per unit, and EBITDA margin. Moreover, the company expects to generate breakeven EBITDA in 3Q.

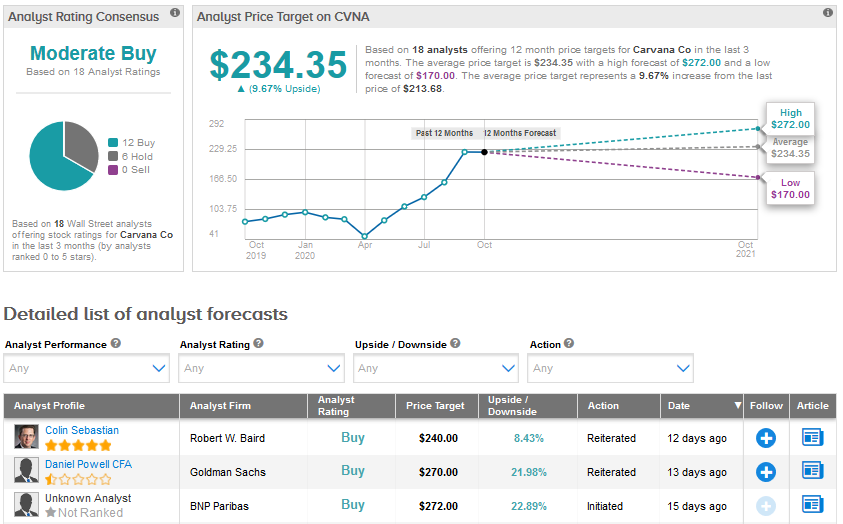

Recently, Robert W. Baird analyst Colin Sebastian reiterated a Buy rating for Carvana with a price target of $240. The analyst said the recent debt offering and the company’s expanded inventory facility provide a further runway for growth. Sebastian continues to believe that the company is well positioned to drive further share gains within the growing online used auto market.

However, the analyst feels that the near-term upside for Carvana may be limited despite strong demand trends. (See CVNA stock analysis on TipRanks)

The Street also has a Moderate Buy consensus for Carvana based on 12 Buys versus 6 Holds and no Sell ratings. With shares rising a whopping 132% year-to-date, the average analyst price target of $234.35 implies an upside potential of 9.7% in the months ahead.

Bottom line

Carvana and Cars.com will continue to benefit from the growing adoption of digital platforms for buying and selling cars. Coming to the recent operational results, Carvana outperformed Cars.com and is poised to deliver robust numbers for 3Q. Also, year-to-date, Carvana stock has delivered impressive returns, unlike Cars.com stock. However, the higher upside potential in Cars.com stock could make it a better pick than Carvana right now.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment