Shares of Cardinal Health rose almost 3% on Friday to close at $57.35 after the healthcare company announced the sale of its Cordis business to Hellman & Friedman (H&F), a private equity company. The deal is worth $1 billion, and includes the buyer’s assumption of certain liabilities and the seller’s retention of certain working capital accounts.

Cardinal Health (CAH) CEO Mike Kaufmann said, “Our decision to divest Cordis demonstrates our disciplined approach to evaluating our portfolio and focusing our resources in our strategic growth areas where we are an advantaged owner.”

Cordis develops and manufactures interventional vascular technology. The transaction, which awaits regulatory approvals, is expected to close in the first half of the company’s fiscal year 2022.

Upon closure of the deal, most of the assets and liabilities related to the Cordis business will be transferred to H&F. However, Cardinal Health will assume liabilities for lawsuits related to inferior vena cava filters in the US and Canada.

The divestiture of the Cordis business will reduce profits of the medical segment by $60 million to $70 million on an annual run-rate basis. Furthermore, the divestiture is likely to result in a pre-tax loss of around $120 million in the third quarter of the company’s fiscal year 2021. (See Cardinal Health stock analysis on TipRanks)

Additionally, Cardinal Health is expected to incur divestiture costs of up to $125 million, mainly in fiscal years 2021 and 2022.

Following the divestiture announcement, Raymond James analyst John Ransom maintained a Hold rating.

Ransom said, “This is the latest example of the drug wholesalers unwinding assets snatched up as the industry looked to consolidate over the past ~5 years, with the common trend being buying high and selling lower.”

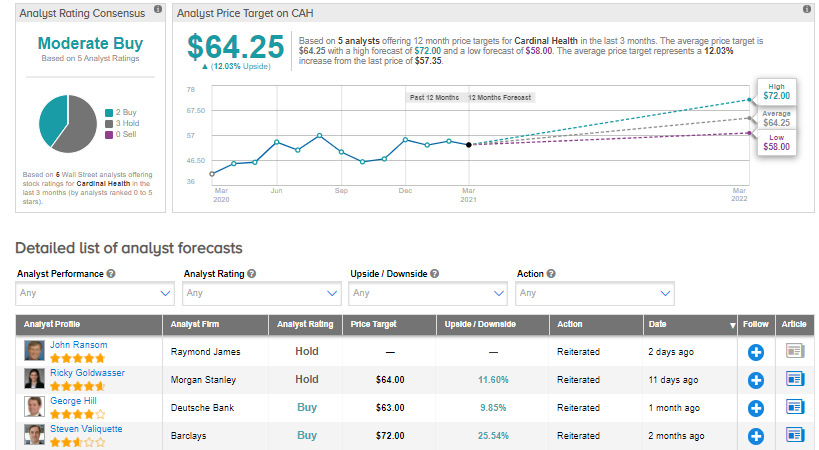

The rest of the Street is cautiously optimistic about the stock with a Moderate Buy consensus rating. That’s based on 2 Buys and 3 Holds. The average analyst price target of $64.25 implies 12% upside potential to current levels. Shares have increased more than 29% over the past year.

Related News:

Dropbox To Snap Up DocSend For $165M; Shares Gain 4%

DuPont Inks $2.3B Deal To Snap Up Laird Performance Materials; Shares Gain

Chevron Inks Deal To Buy Noble Midstream Partners; Shares Gain 4%