Canopy Growth Corporation (TSE: WEED) (NASDAQ: CGC) reported disappointing results for its first quarter of Fiscal 2023. Consequently, shares of the stock were down 5.1% on August 5, as investors frowned at the company reporting a wider-than-expected net loss. However, the stock has more than recovered its losses, as it is up over 15% today.

With a market cap of C$1.9 billion, Canopy Growth is a diversified cannabis and cannabinoid-based consumer product company. This Canada-based company is a leading producer and distributor of cannabis and hemp-based products for recreational and medical purposes, primarily in Canada, the United States, and Germany.

Goodwill Impairment Charge Caused CGC’s Large Net Loss

The pot producer saw its net loss coming in at C$5.23 per share in the first quarter of Fiscal 2023 against the earnings of C$0.84 per share in the year-ago period. The metric also compares unfavorably with analysts’ estimates of a C$0.29 per share net loss. Notably, Canopy Growth took a non-cash goodwill impairment charge of C$1,725 million related to its cannabis operations unit, which is already included in the company’s quarterly net loss.

Impairment charges are costs that reflect a decline in the carrying value of any particular asset on a balance sheet.

Net revenues for the June quarter came in at C$110 million, decreasing 19% from the year-ago period. There was a 29% year-over-year decline in total global cannabis net revenues to C$66 million in the reported quarter. The downside was partly caused by sluggishness in value flower sales in Canada’s recreational market, largely due to the company shifting its focus on higher margin and premium products.

Meanwhile, there was a 1% year-over-year rise in net revenues from other consumer products to C$44 million in the reported quarter. Furthermore, after eliminating the impact of acquired businesses and the divestiture of C3, there was a 17% decline in net revenues from the prior year.

During the reported quarter, Canopy Growth increased its share of the combined mainstream flower and pre-rolled joint (PRJ) segment by 35 basis points, to 4.0%.

Canopy Growth witnessed a 169% year-over-year surge in BioSteel sales in the first quarter of Fiscal 2023. The upside was driven by growth in distribution channels, strong sales momentum across North America, and higher global sales.

The company witnessed an outflow of C$143 million in the first-quarter Fiscal 2023. The outflow declined 23% over the prior-year period. CGC exited the June quarter with cash and short-term investments of C$1.2 billion, declining from C$1.4 billion on March 31, 2022.

Canopy Growth Has Mixed Investor Sentiment

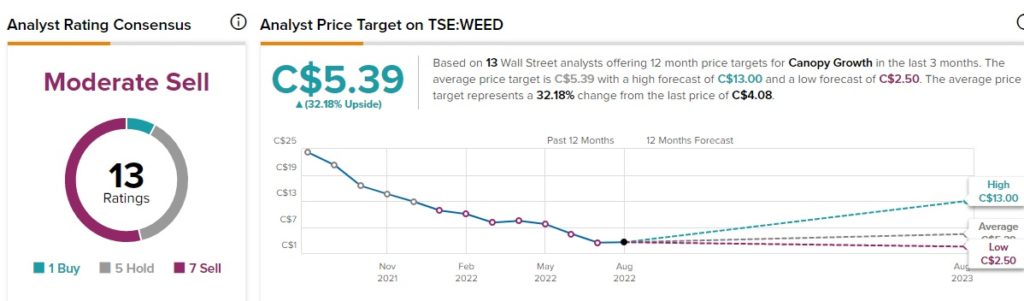

On TipRanks, analysts have a Moderate Sell consensus rating on Canopy Growth, which is based on one Buy, five Holds, and seven Sells. However, Canopy Growth’s average price forecast is C$5.39, which implies that the stock has upside potential of over 32.2% from current levels.

While analysts have mixed feelings about the stock, financial bloggers are 62% Bullish on WEED. Similarly, retail investors on TipRanks are optimistic about the stock, as the number of portfolios with investments in WEED has increased by 2.3% in the last 30 days.

Canopy Growth: Facing Headwinds, but It Can Recover

Canopy Growth has been facing several headwinds like cheaper black-market rates, limited retail stores, regulatory issues, high inflation, and market fragmentation. However, the pot producer has moved its focus to premium products and has adopted some cost-cutting initiatives that can help it achieve profitability.

The company is maintaining its top position in the combined premium flower and PRJ segment, which is a positive sign. Canopy Growth also witnessed growth in its premium Doja and mainstream Tweed brands in the reported quarter, another positive for the stock.