Tesla (NASDAQ:TSLA) left many investors disappointed last week as hopes for a boost from its robotaxi unveiling failed to materialize. In fact, not only did the stock fail to rise, but it also took a hit, with critics pointing to a lack of substance at the flashy Hollywood-based event.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

For his part, Piper Sandler analyst Alexander Potter was hoping the unveiling would “yield an excuse to boost estimates.” In this regard, says the analyst, “optimism is fading.”

“On the other hand,” Potter goes on to say, “there’s no need for estimate cuts, because we had always assumed that revenue from full self-driving (FSD) software wouldn’t begin ramping until 2027/2028.”

So, it’s basically back to square one. And in Tesla’s case, square one means selling cars, and that, says the analyst, might just be a “good thing.”

Prior to the hype-fueled robotaxi event, sentiment around Tesla was already not great after investors were left unimpressed with the Q3 delivery haul. Not Potter, however, who expected a lower volume than the 463,000 units the EV leader delivered in the quarter. As such, driven by strong seasonal demand in China and the ongoing ramp of Cybertruck production, Potter is comfortable on his Q4 forecast of 465,586 units. Additionally, Potter highlights the fact that Q4 always represents Tesla’s best delivery quarter, so the usual end-of-year surge should also be forthcoming.

Looking forward to next year, the analyst thinks 2025 deliveries will reach ~1.9 million units, amounting to year-over-year growth of around 8%. Fueled by lower interest rates and “greater penetration in new regions,” legacy models (S, 3, X, and Y) will account for about half of the growth. Another “key assumption” for 2025 is that the Cybertruck will notch 100,000 deliveries. Potter is also hopeful that a Model 2 will be unveiled in time to have an impact on the 2025 forecast, although he says it’s uncertain whether that will actually happen.

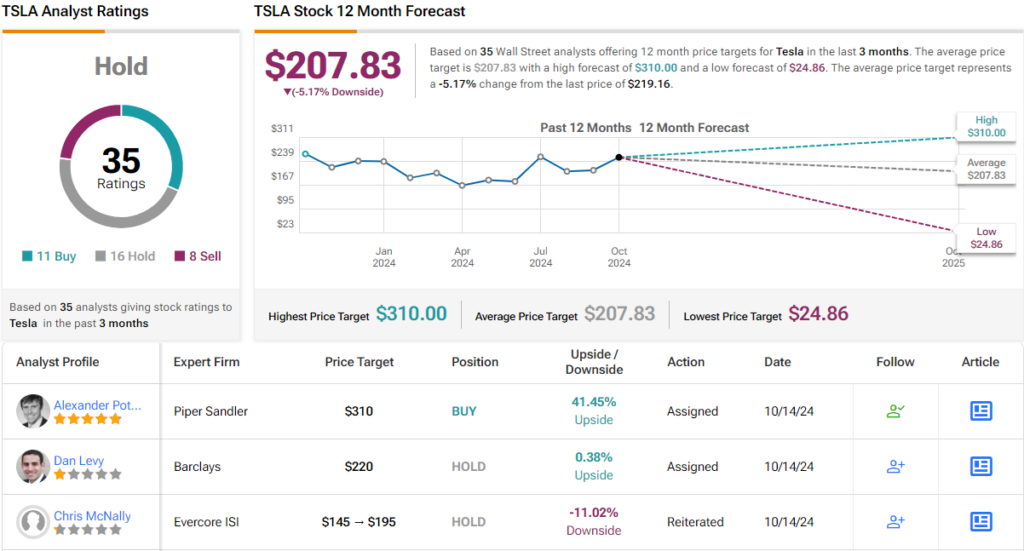

Bottom line, Potter rates Tesla shares an Overweight (i.e., Buy), while his $310 price target makes room for ~42% gains in the months ahead. (To watch Potter’s track record, click here)

Bulls will like that, but the majority of Potter’s colleagues aren’t quite as convinced. Overall, the analyst consensus rates the stock a Hold (i.e. Neutral), based on 16 Holds, 11 Buys and 8 Sells. Meanwhile, given the average target stands at $207.83, the shares are anticipated to shed 5% of their value by this time next year. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.