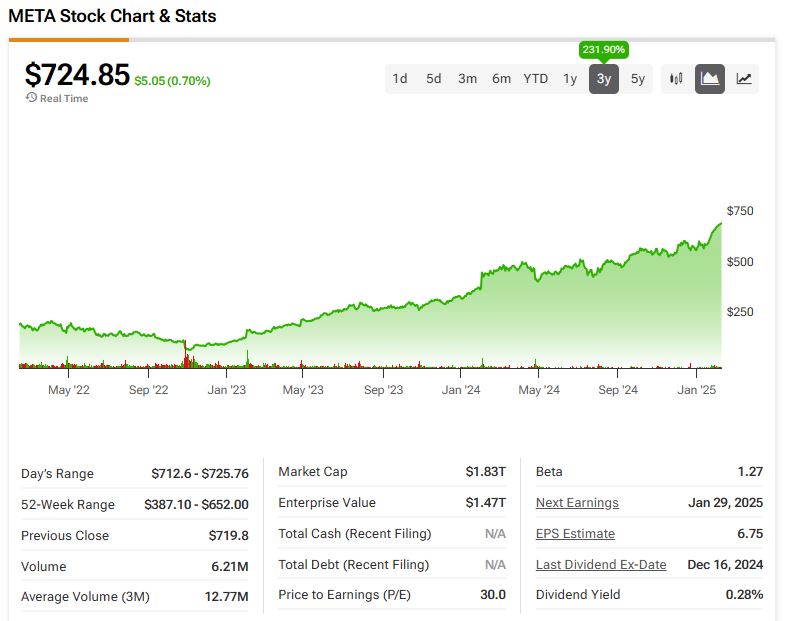

Meta Platforms’ (META) stock is on a major winning streak, and bulls must be thrilled after seeing gains for sixteen consecutive trading sessions. In fact, regardless of which timeframe you choose on a META chart, you will likely see a near-45-degree upward trend line.

As a long-term Meta bull, my positive outlook comes from believing that the current market doesn’t leave much room for the runners-up. Meta, the clear leader in social media, is making solid progress in AI with its Llama model, which should fuel continued growth in an advertising market driven by secular trends. Moreover, the company’s latest results were impressive, especially regarding operating margins.

Although the social media giant’s valuation is fair, it’s not exactly a bargain, especially when compared against its Magnificent 7 peers. Meta’s recent developments, including progress in AI, not only support its current valuation but leave room for further bullish sentiment that could see the stock testing $1,000 per share by the end of 2025.

Advertising Still Powers META’s Growth

Currently, Meta holds second place globally in digital advertising revenue, just behind Alphabet (GOOGL). In late January, Meta Platforms reported strong Q4 2024 results, which were well-received by investors, with the ensuing rally helping META stock to gains of nearly 20% year-to-date and 53% over the past twelve months.

In both the quarterly and annual results, META’s operating profit margin increased by 7 percentage points to 48% in the most recent quarter and 42% for the year. To put that into perspective, great businesses usually aim for operating margins above 20%, and in Meta’s case, they’re now approaching 50%.

What’s even more surprising are Meta’s operating metrics. Despite worries that social media platforms had already captured all possible users, Meta’s total family daily active people (DAPs) grew to 3.35 billion as of December 2024. That’s a 5% year-over-year increase, adding over 150 million new daily active users across Meta’s app family.

With this growth in DAUs, the number of advertising impressions served across Meta’s apps grew by 6% for Q4 and 11% year-over-year for the full year of 2024. This suggests that people are spending more time on the platform, which, in turn, creates more opportunities for ads. To top it off, the average price per ad also increased, rising 14% in Q4 and 10% for the full year.

Meta’s Edge in the AI Race

I believe Meta is one of the companies in the Magnificent 7 group playing their AI cards somewhat differently from the other six.

Take Apple (AAPL), for instance. The iPhone maker didn’t create its own large language models (LLMs) as Meta did. Instead, Apple chose to outsource AI development, relying on innovations from other companies (like OpenAI’s models or others) for its AI services. As the cost of developing LLMs decreases over time, businesses (including Apple) can take advantage of AI without needing to heavily invest in creating the technology themselves.

Meta could have taken the same approach, which isn’t necessarily a bad strategy, but having an inventive CEO like Mark Zuckerberg at the helm makes all the difference. Meta has developed its own open-source LLM, Llama. Being open-source means other developers and companies can use and contribute to Meta’s AI models. This gives Meta a significant advantage in adoption, as they can tap into a larger ecosystem of people (and customers). With Meta having its own AI platform, the company could monetize these advancements much faster than other tech giants. This is especially true when you consider Meta’s massive network of users and advertisers who can integrate AI into their ad ecosystem, improving efficiency and driving further revenue growth.

While Llama might not start generating significant returns in 2025, the potential for AI-driven growth and determining how monetizable it is should become clearer in 2025.

The Magnificent Stand-Off

Compared to the Magnificent 7 peers, Meta trades at earnings multiples of nearly 30x, which is only more stretched than Alphabet at 23x.

If we adjust these metrics for growth, with analysts forecasting Meta’s EPS to grow around 17.8% per year over the next three to five years, it gives Meta a PEG ratio of 1.6x. That’s in line with its five-year average and lower than Nvidia (NVDA) and Alphabet, which have PEGs of 1.2x.

One could argue that Alphabet is probably the best comparison to Meta regarding AI, especially for AI-driven advertising and consumer applications. Alphabet still has a wider AI presence, with everything from search engines to cloud services.

Still, I think Meta’s premium valuation is justified, given the strong momentum the stock has been experiencing. Analysts expect Meta to grow revenue by 16.7% in the next fiscal year, compared to just 12% for Alphabet, and diluted EPS growth of 24.5% versus 20.8% from Alphabet’s. Additionally, while Alphabet has dominated the search engine space for years, it’s been the runner-up in most of its other ventures. I believe this could explain why Alphabet stock has been trading at a historical discount compared to other Big Tech companies, especially Meta, particularly after years of sluggish growth before the AI boom.

What is the Target Price of META?

Wall Street experts are primarily bullish on META shares, but their price targets suggest limited upside given the stock’s substantial recent gains. META stock carries a Strong Buy consensus rating based on 44 Buy, three Hold, and one Sell rating over the past three months. META’s average price target of $764.61 per share implies a 5.5% upside potential compared to current levels.

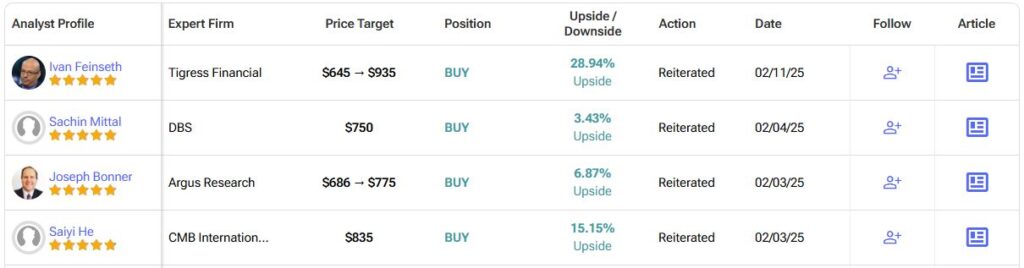

One analyst, Ivan Feinseth from Tigress Financial, recently raised his price target on META from $645 to $935 per share, citing substantial investments in AI and smart wearables as two particular product lines likely to enhance user engagement and content quality across META’s various applications.

AI & Advertising: The Twin Engines of Meta’s Growth

In summary, Meta’s strong Q4 earnings and impressive growth in social media users and AI developments, particularly with Llama, position it for continued success. While the stock has already had a big run-up, its valuation still seems reasonable, especially considering its potential for AI-driven growth. The company’s ability to leverage its massive user base and advertising network gives it a significant edge over its peers.

Meta’s insatiable stock momentum and positive outlook make it an appealing choice for long-term investors, even within the volatile tech sector. The company’s bread-and-butter business (ads) remains solid, while emerging delicacies like AI present additional upside. Although Meta has seen promising early results in AI, these innovations have yet to be fully integrated and monetized. Social media stands out as one of the most transformative spaces for widescale AI applications, so it stands to reason that Meta’s dominance in the sector gives it the power to shape how AI influences what matters most to people: their connections with others.