One of the biggest turnaround stories of the year is reserved for a beaten-down giant. Intel (NASDAQ:INTC) stock had fallen out of favor with investors in recent years, as missteps including delays and bad products decisions paved the way for rival AMD to eat away at its dominance of the CPU market.

That has not been the case this year, however, with the stock having delivered year-to-date returns of 86% against a backdrop of improving fundamentals and the company looking on track to meet its roadmap’s targets.

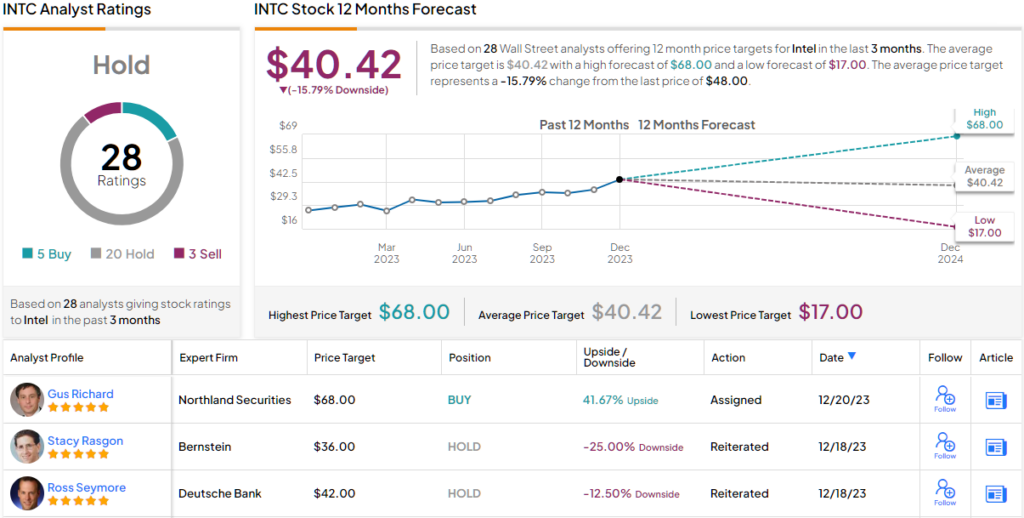

That said, despite the positive sentiment, Northland’s Gus Richard, a 5-star analyst rated in the top 1% of the Street’s stock pros, maintains the opinion that Intel remains undervalued.

“We believe the Company will recapture process technology leadership and stabilize its market share in PCs and servers in CY25, if not grow,” Richard went on to say.

The analyst expects revenue will reach $63 billion in CY24, rising to $72 billion in CY25, amounting to respective growth of 8% and 16%. Strong PC demand should also be on the menu in CY25, given it will be 5 years since the pandemic-driven PC boom, with Richard noting five years is the “typical length for a PC refresh cycle.”

The most meaningful boost to Intel’s earnings power, though, will come in the shape of expanding gross margins. Richard expects Intel’s non-GAAP GM to grow by 9.5% from 43% in CY23 to 52.5% in CY25. “We do not think we are making heroic GM assumptions as we are modeling the gross margin in CY25 to be 10% below INTC’s historical peak,” noted the analyst.

Moving forward, Richard also thinks it’s very likely Intel will split into 5 separate companies – Intel products, Intel Foundry services, Altera, Mobileye, and IMS Nanofabrication. With $20 billion in revenue, the foundry business on its own would be the world’s second-largest foundry while the split into distinct entities should unlock shareholder value.

All in all, Richard reiterated an Outperform (i.e. Buy) rating backed by a Street-high $68 price target. Should the figure be met, investors will be pocketing returns of ~42% a year from now. (To watch Richard’s track record, click here)

Unlike Richard, however, most on the Street remain on the INTC fence. While 4 other analysts join him in the bull camp, with the addition of 20 Holds and 3 Sells, the stock receives a Hold consensus rating. Moreover, most seem to think the shares are overvalued rather than the other way round; the $40.42 average target implies downside of ~16% over the next year. (See Intel stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.