Wall Street is sometimes a hard place to please. Case in point: Alphabet (NASDAQ:GOOGL) shares tumbled 5% in Wednesday’s trading session, despite the company delivering a better-than-expected Q2 report.

Don't Miss Our New Year's Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Driven by the Search business and the Cloud segment (which saw year-over-year gains of an impressive 28.8% and crossed the $10 billion threshold for the first time), revenue climbed by 13.6% compared to the same period last year, reaching $84.74 and beating the consensus estimate by $450 million.

Operating income saw a 26% uptick, climbing $27.4 billion, and the operating margin increased by three points to 32%. At the bottom-line, EPS reached $1.89, 4 cents above expectations.

However, despite these strong results, investors found reasons for concern. YouTube revenue growth, although up 13%, fell short of expectations and showed a sequential decline. Perhaps more significantly, Q3 margin expansion is set to be affected by various trends highlighted by the company on top of a possible headcount increase. Additionally, according to President Ruth Porat, there could be higher depreciation and expenses from greater investments in technical infrastructure.

For Goldman Sachs analyst Eric Sheridan, however, despite expecting the Search business’ prospects will continue occupying investors, the bull case remains intact.

“We continue to view Alphabet as well-positioned against both the current (mixture of desktop and mobile utility) and potential future (AI/ML; personalization; lowered friction to applications) computing landscapes,” said the 5-star analyst. “We continue to expect the key investor debates going forward to be centered around the future of search (due to computing and regulatory externalities), the potential for operating margin outcomes (with management balancing investments in long-term opportunities against durably re-engineering the cost structure) and the level of long-term investments needed around data centers and technical infrastructure (capex trajectory).”

Conveying his confidence, Sheridan rates Alphabet shares a Buy, while slightly raising his price target from $211 to $217, implying the stock will post growth of 26% from current levels. (To watch Sheridan’s track record, click here)

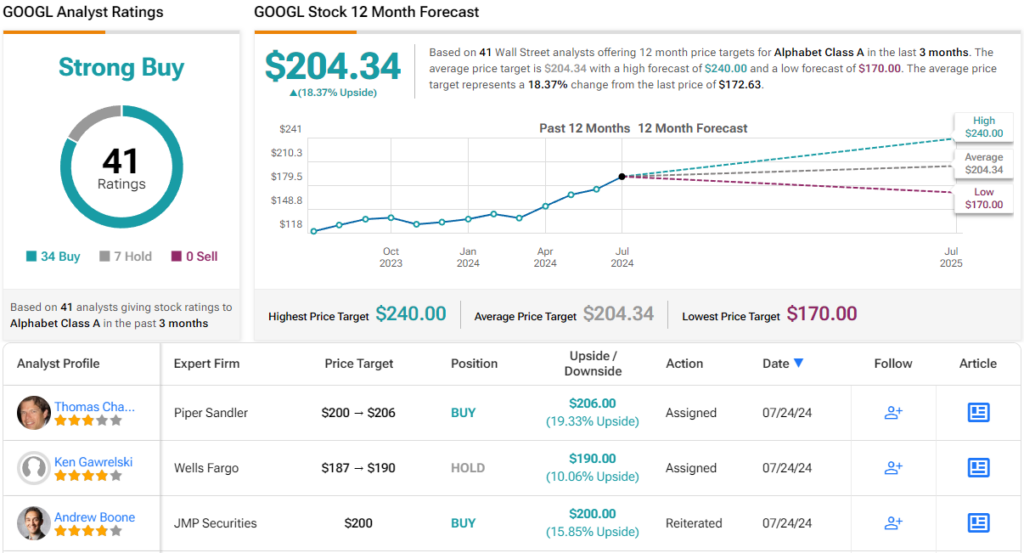

Sheridan’s colleagues largely agree, with a consensus rating of Strong Buy based on 34 Buy recommendations and 7 Holds. The shares are expected to appreciate by 18% over the next 12 months, considering the average target stands at $204.34. (See Alphabet stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.