Spirit Airlines (SAVE) has seen its shares climb 37% after the airline temporarily avoided potential bankruptcy by exhausting its $300M senior secured revolving credit facility, giving the company a boost until it matures in September 2026. The budget airline is expected to have over $1B in liquidity by the end of 2024, assuming it completes current initiatives such as extending its Card Processing Agreement until December 2024. The carrier is in dialogue with bondholders over its debt maturities, and a recent deal with creditors has allowed them to push a debt restructuring deadline to December 23rd.

Spirit may have bought itself some time with its current financial engineering; however, following a rejected merger with JetBlue Airways and a year-long decline in the share price, it is not out of the woods yet, with the ongoing threat of potential bankruptcy lurking.

Spirit Staves off Bankruptcy

Spirit Airlines is a low-fare airline that serves 93 destinations in 15 countries in the United States, Latin America, and the Caribbean. It operates one of the youngest and most fuel-efficient fleets in the United States.

Shares of the company experienced a sharp drop after the failed merger with JetBlue led to a sizable sell-off. This sell-off has recently accelerated due to a Wall Street Journal report regarding the company’s potential bankruptcy filing, helping to drive the stock down over 90% year-to-date.

Despite the ongoing speculations, the airline has confirmed through a late 8-K filing to the U.S. Securities and Exchange Commission (SEC) that it continues to operate without filing for bankruptcy. With an extension of its existing debt refinancing plan with credit card processors Visa and Mastercard, Spirit has postponed the original deadline to December 23, a subsequent postponement from the first deadline set in September. The airline also reported borrowing the entire $300 million from a revolving credit line, expecting to conclude 2024 with over $1 billion of liquidity.

Despite Spirit’s efforts to stave off bankruptcy, the airline is not yet in a safe zone. It’s grappling with more than $3 billion in debt, mainly due to operating unprofitably since before the COVID-19 pandemic. The financial strain is further aggravated by $1.1 billion in secured bonds set to mature in less than a year. The company has been in talks with bondholders about the terms of a possible bankruptcy filing. Concurrently, Spirit has been looking into potentially restructuring its balance sheet.

Spirit’s Recent Financial Results & Outlook

Spirit Airlines reported disappointing results for Q2 2024, falling short on revenue and earnings per share (EPS). Spirit’s revenue for the period amounted to $1.28 billion, 3.68% below the estimated $1.33 billion, while the company’s EPS was -$1.44, underperforming the analysts’ prediction of -$1.36.

Looking ahead to Q3 2024, Wall Street analysts forecast a further dip in Spirit Airlines’ performance. Revenue is estimated to come in at $1.18 billion, and EPS is expected to be roughly -$2.30.

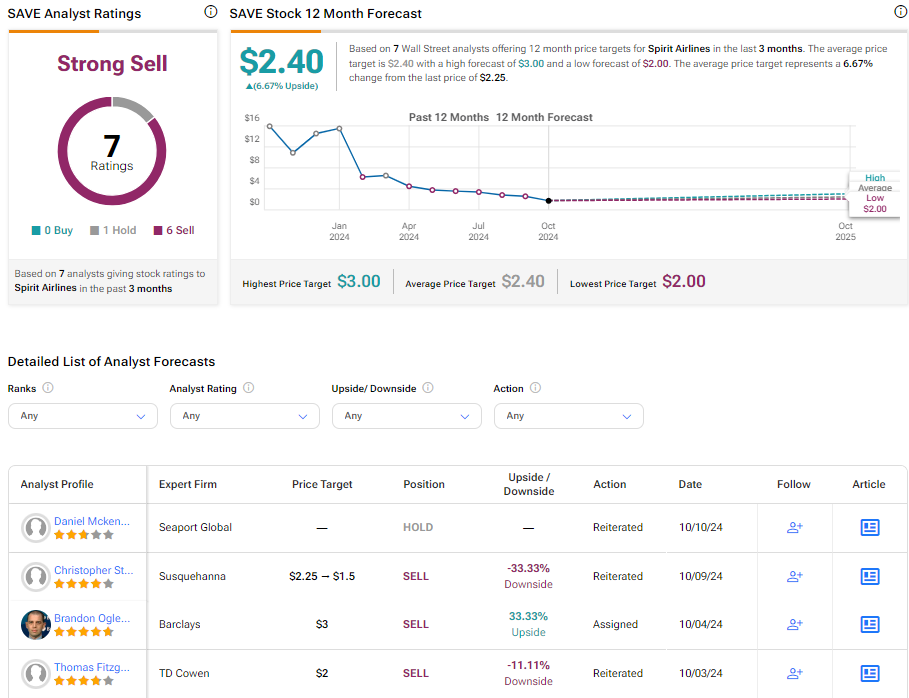

What Is the Price Target for SAVE Stock?

Despite the recent jump in the stock, it has been on an extended decline over the past three years, shedding roughly 93% in that time. The stock trades at the low end of its 52-week price target of $1.40 – $17.49, showing ongoing negative price momentum as it trades below the 20-day (2.28) and 50-day (2.56) moving averages.

Analysts following the company have been bearish on SAVE stock. For instance, Susquehanna has lowered the price target to $1.50 and kept a Negative rating on the shares as part of a Q3 earnings preview for the airlines and aircraft leasing group.

Based on seven analysts’ recent recommendations, Spirit Airlines is rated a Strong Sell overall. The average price target for SAVE stock is $2.40, representing a potential upside of 6.67% from current levels.

SAVE in Summary

Faced with the threat of bankruptcy, Spirit Airlines has bought some time courtesy of a series of financial maneuvers, including exhausting its $300M senior secured revolving credit facility and extending its Card Processing Agreement. While these interventions offer some respite, Spirit’s financial instability is far from over; it struggles with over $3 billion in debt and a lack of profitability. Although the airline expects to amass over $1B in liquidity by 2024 end, unfavorable market sentiment underscored by a sharp sell-off and declining share price points to a rocky financial trajectory for Spirit in the near future.