It’s no secret Nvidia (NASDAQ:NVDA) rules over the AI chip landscape and the huge strides the semiconductor giant has taken over the past couple of years have cemented its position amongst the world’s biggest companies.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks right to your inbox with TipRanks' Smart Value Newsletter

With the AI opportunity still at play, Citi’s Atif Malik, an analyst ranked in 11th spot amongst the thousands of Wall Street stock experts, has been outlining the main topics on investors’ minds right now.

Gross margin trends remain a major talking point. Since the AI supercycle kicked off midway through last year, GMs had been on an upward trajectory, reaching a high of 78.9% in the April quarter. However, in the July quarter, the margin dropped to 75.7%. Malik sees the figure dropping further, hitting a low 70’s or ~72% trough in the January quarter, although once the Blackwell GPU platform fully ramps, the analyst expects long-term gross margins to “stabilize in the mid-70s%.”

Nvidia has cornered the market for AI chips but the prospect of competitors catching up is another topic being discussed amongst the investor base. On this issue, while Malik notes the importance of performance metrics, the analyst believes data center operators prioritize TCO (total cost of ownership) and ROI (return on investment), both of which depend on throughput, an area where Nvidia excels.

“As NVDA runs various applications including AI, the data center operators rely on NVDA to have the hardware to run multiple applications rather than buying accelerators that are limited in their use cases,” Malik further explained.

Regarding ROI, Nvidia has underscored the advantages its products offer to consumer internet companies in major fields like social media, e-commerce, and search. But with generative AI driving disruptive business models, Malik advises investors to be patient as these opportunities fully develop.

That stance, however, will pay off eventually. “While we are bullish on another strong +40% Y/Y cloud data center capex growth next year, we expect the stock to likely remain range bound through CES January before Blackwell driven Y/Y sales and gross margin inflection in the Apr-Q,” Malik summed up. “Fundamentally, we believe AI adoption remains in 3rd/4th innings as enterprise AI demand takes off next with AI agents.”

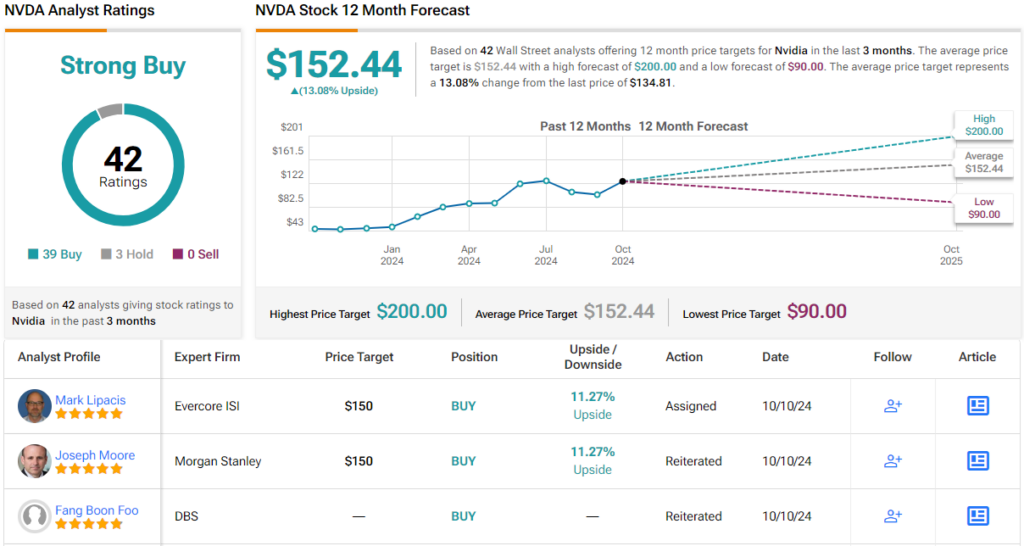

To this end, Malik rates NVDA shares a Buy while his $150 price target implies shares will climb 17.5% higher over the coming months. (To watch Malik’s track record, click here)

Looking at the broader analyst consensus, aside from three holdouts, all 38 other analysts covering Nvidia are bullish, resulting in a Strong Buy consensus. With an average price target of $152.44, analysts expect the stock to trade at a 13% premium in a year. (See Nvidia stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Looking for a trading platform? Check out TipRanks' Best Online Brokers , and find the ideal broker for your trades.

Report an Issue