The apparel scene seems to be ripe for disruption these days, with some industry juggernauts falling at the hands of smaller, less dominant, and, in some cases, nascent rivals. Undoubtedly, even the bluest blue chips in apparel can get rocked as times and consumer preferences fluctuate. In this piece, we’ll examine three Strong-Buy-rated apparel retail plays—BOOT, SKX, and TJX. These firms seem well-equipped to continue thriving as they seek to take share and benefit from consumers recovering from inflation.

Therefore, let’s check in with TipRanks’ Comparison Tool to determine which Strong-Buy-rated retail name has the most room to run for the year ahead.

Boot Barn (NYSE:BOOT)

Shares of Western wear retailer Boot Barn have been rounding up for decent gains in 2024, now up 66% year-to-date. Undoubtedly, before you hop off the horse amid Calgary Stampede rodeo season, you may wish to consider the timely share price drivers that are still ahead. As Boot Barn continues its brick-and-mortar expansion while making smart marketing moves, I find it hard to be anything but bullish on BOOT stock.

Undoubtedly, the return of denim (and Western wear as a whole) is thanks in large part to profoundly popular singers like Beyonce and Taylor Swift. Whether we’re talking about head-to-toe denim and cowboy hats dawned by Beyonce or Taylor Swift’s catchy country music, it’s clear that the two icons have brought Western attire back into fashion in a big way. But it’s not just outside influences that have kicked Boot Barn onto the high road.

Despite the tough macro picture for the discretionary retail plays, Boot Barn seems poised to play the long game with its unit expansion (the long-term target is to hit 500 stores, up from just under 400) and same-store sales growth (SSSG) initiatives.

Most notably, a partnership with country star Morgan Wallen could drive more foot traffic. Combined with favorable fashion trends, BOOT stock may be the best apparel play to buy if you’re bullish on the consumer. With a mere $3.8 billion market cap, the store expansion and SSSG efforts could be a very effective formula to return to high-double-digit growth.

With investment firm Baird recently touting Boot Barn as having a quality growth story in apparel, I’d not be afraid to buy at 25.5 times forward price-to-earnings (P/E), which is on the high side of the past-year historical range.

What Is the Price Target of Boot Barn Stock?

BOOT stock is a Strong Buy, according to analysts, with 12 Buys and two Holds assigned in the past three months. The average BOOT stock price target of $130.92 implies 4.5% upside potential.

Skechers (NYSE:SKX)

Skechers is another apparel play that’s found itself in fashion amid the past two years of inflation. Indeed, Skechers has outrun Nike (NYSE:NKE) in the last two years, soaring an astounding 83% versus Nike’s ugly 31% decline. Skechers aren’t as “cool” as Nike, so why is there such a sudden shift in footwear tastes? Skechers simply has the better value proposition for an inflation-rocked consumer. It has cheaper wear, and they’re just as comfortable and innovative as Nike, if not more so. Either way, I continue to view SKX as a cheap stock and am staying bullish.

At writing, Skechers shares trade at 17.9 times trailing P/E after correcting around 11% from all-time highs. Recently, Bank of America (NYSE:BAC) Securities touted SKX stock as a double-digit earnings grower to buy at a discount.

Indeed, SKX stock trades at a huge discount to the footwear and accessories industry average of 21.6 times trailing P/E. With success in the direct-to-consumer (DTC) platform and innovation that’s stride for stride with Nike, I do see a growth path the firm can easily walk down. Pending a sudden fashionable reversal back to expensive, status symbol-esque brands, I’d stick with Skechers on the dip.

What Is the Price Target of Skechers Stock?

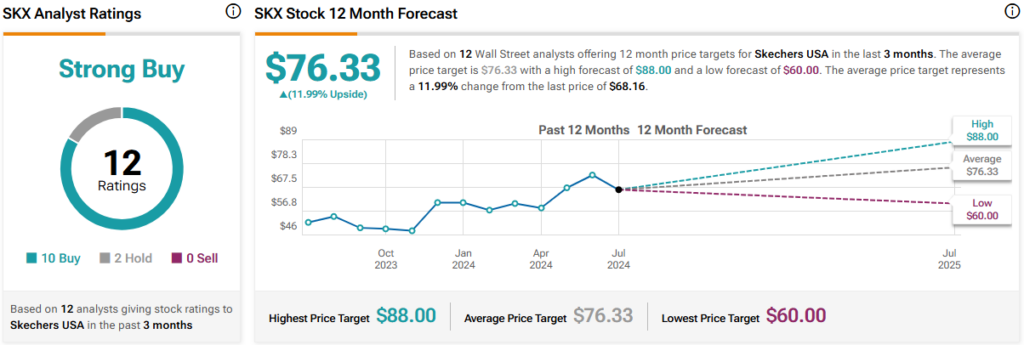

SKX stock is a Strong Buy, according to analysts, with 10 Buys and two Holds assigned in the past three months. The average SKX stock price target of $76.33 implies 12% upside potential.

TJX Companies (NYSE:TJX)

TJX stock has been unstoppable of late, with shares at new all-time highs. After nearly doubling in the past two years, the off-brand retail chain faces a tougher set of expectations ahead. However, Wall Street still has confidence in the name, even as the valuation creeps ever so steadily higher. I’m inclined to stay bullish as the appetite for deals at the discount racks around the world is unlikely to fade overnight.

Most notably, TJX is readying to expand into the lucrative Mexican market, which has also been hurting from high inflation. According to CEO Ernie Herrman, there’s “excellent potential to grow in another region and deliver our value proposition to a growing population of fashion- and value-conscious consumers in Mexico.”

I think the Mexico expansion is a big deal, and I think off-branded goods could fly off shelves in the same way they have been in the U.S. As TJX becomes more of an international story, the 27.8 times trailing P/E mutiple, which is on the high end of the past-year range, seems like it’s still worth paying.

What Is the Price Target of TJX Stock?

TJX stock is a Strong Buy, according to analysts, with 17 Buys and two Holds assigned in the past three months. The average TJX stock price target of $116.18 implies 1.6% upside potential.

The Takeaway

Apparel retail stocks have been faring incredibly well despite consumer-facing challenges. As each firm continues executing its strategies while pursuing unique growth pathways, more gains seem likelier than not for the year ahead.

Whether we’re talking TJX and its expansion into Mexico, Skechers and its low-cost wears, or Boot Barn and its country tailwinds, each firm has levers to pull to power growth. Of the trio, analysts seem to see SKX as having the most room to run. I’m inclined to agree. It’s the cheapest stock, with prospects that can easily power sustainable double-digit growth.