I’m bullish on Boeing’s (BA) stock, and the recent settlement of the machinist strike only strengthens my conviction. With 33,000 workers walking out in September 2024, production halts led to over $6 billion in third-quarter losses and a 31% drop in the share price. However, I see the new labor agreement as a pivotal moment that paves the way for operational stability, reinforcing my belief that Boeing is a compelling buy at its current levels.

I’m particularly encouraged by the terms of the settlement – a nearly 43% pay raise over four years and a $12,000 ratification bonus. While these terms will obviously increase costs in the near-term, the 59% approval rate from union members suggests a driven workforce ready to return to production. For a company with a $428 billion backlog, getting planes moving again is worth far more than the increased labor expenses.

Boeing’s Underlying Operational Metrics Show Some Promise

I am optimistic about Boeing’s ability to sustain deliveries even during challenging times, as evidenced by its third-quarter results. Revenue reached $17.84 billion, and while significant costs led to a core loss per share of $10.44, I think the underlying operational metrics show some promise. Boeing delivered 116 commercial airplanes, maintaining steady progress despite the immense labor disruption. The Commercial Airplanes division sits on a massive backlog of $428 billion representing over 5,400 aircraft orders – a testament to sustained demand even through recent challenges.

Looking ahead, management’s guidance of $1.85-1.90 billion in revenue reflects a decent balance of caution and confidence. The 787 program’s planned increase from four to five aircraft per month by year-end represents a key milestone in the production recovery. This measured approach to ramping production, while fairly conservative, should help maintain quality and regulatory compliance over the coming years.

BA Shows Strength in Key Areas

Fortunately, the business operates across a diverse range of growing sectors. Defense, Space & Security has emerged as a bright spot in recent times, securing $8 billion in new orders, bringing its backlog to $62 billion. The recent contract momentum is rather impressive: a $2.39 billion Air Force contract modification, a $1.68 billion Navy contract modification, and an additional $129.19 million Air Force contract. Despite any near term disruption, the U.S. government’s shows continued confidence in the company’s capabilities.

Looking at geographic revenue distribution, Boeing’s 81.7% Americas concentration might seem fairly high, but I see this as a strength in the current geopolitical environment. The 10.6% EMEA and 7.7% APAC revenue mix offers growth potential while limiting exposure to international trade tensions.

The company’s liquidity position remains pretty solid, with $10.5 billion in cash and marketable securities. While total debt stands at $57.7 billion, Boeing maintains investment-grade ratings from all three major agencies (S&P: BBB-, Moody’s: Baa3, Fitch: BBB-). Such debt levels are not exactly rare for aerospace companies, and represent the vast expenses and cyclicality of the sector. With government contracts such a key component of the company’s income, and such a healthy backlog, I’m not particularly concerned about revenues drying up any time soon.

Is Boeing a Good Stock to Buy Right Now?

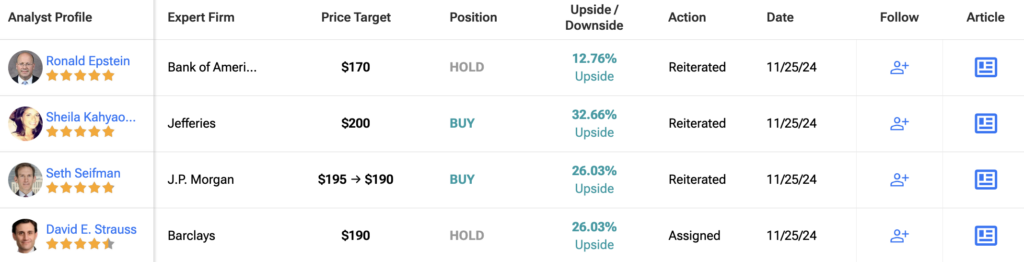

Wall Street’s analysis increasingly aligns with my optimistic outlook. Based on 23 recent analyst ratings, Boeing holds a Moderate Buy consensus with an average BA price target of $193.38, suggesting nearly 30% upside from current levels. Notable bullish calls include Benchmark Co.’s $250 target (67.46% upside) and Citi’s $209 target (40% upside).

Plenty of Risks Remain for Boeing

Despite my long-term optimism, I’d urge potential investors to consider several risk factors. The ongoing workforce reduction, targeting 10% of their 177,000 employees, reflects a necessary but challenging restructuring. A recent $20 billion capital raise, while securing liquidity, has resulted in shareholder dilution, one of my biggest red flags for companies I’m analysing. Quality control and regulatory scrutiny also remains incredibly intense following past safety issues and negative media attention.

Yet at current prices, I find the risk-reward proposition compelling. Boeing is well off its 52-week high of $267.54. The stock has been battered by the strike, program charges, and broader market concerns. But with labor stability restored, strong defense contracts flowing, and commercial production poised to recover, I think that multiple catalysts could drive appreciation toward analyst targets in time.

The company’s institutional ownership structure provides another layer of stability – with 19% held by institutional investors and 20% by mutual funds, with major holders like Vanguard (8% stake) providing long-term support. While retail investors hold 44%, the strong institutional base suggests sophisticated investors see decent value at these levels.

Key Takeaway

In conclusion, while Boeing faces clear challenges, I believe the resolution of the labor dispute marks an inflection point. The combination of a stabilized workforce, strong defense contract momentum, improving operational metrics, and beaten-down stock price creates an attractive entry point for long-term investors. The path to recovery probably won’t be straight, with plenty of risks in play, but with nearly 30% upside to consensus targets, and some analysts seeing as much as 67% potential appreciation, patient investors could be well rewarded as Boeing works through its near-term challenges.

The labor settlement, while obviously expensive, now provides the stability needed to tackle a substantial backlog and restore operational excellence. With multiple catalysts ahead and sentiment near recent lows, I believe now is a pretty decent time to consider building a position in this aerospace leader.