Buying shares at the right moment is a skill investors develop over time. Just as important, however, is knowing when to sell. Even maven investors like Ken Fisher admit that this is one of the most challenging lessons to learn.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

“One of the toughest things in investing is to know when to sell a stock,” says the founder and executive chairman of Fisher Investments. “The reality is, you never really do. You just think you do and you conclude. If you knew, well, knowing implies near perfect information. And in capital markets you never really have even close to perfect information.”

That’s not to say you can’t use indicators that will show it’s time to offload a stock. Fisher, who has a net worth of $11.2 billion, stresses the importance of reevaluating stocks an investor holds. “If you missed something important that was negative, now you need to start thinking about how you get out,” he said.

Fisher has obviously been evaluating some of his own moves, as recently he has been trimming his holdings in two chip giants – AMD (NASDAQ:AMD) and Intel (NASDAQ:INTC). So, let’s take a deep dive into the pair and get an idea why the billionaire has decided to take a step back here.

Advanced Micro Devices (AMD)

The story of AMD’s turnaround is one that shows how significant the right management can be. The chipmaker was on the verge of bankruptcy a decade ago when Lisa Su took over running the business. And since then, under her astute leadership, it has not only become an industry giant, but the company has also delivered massive gains for investors.

This success has been driven by AMD’s ability to close the gap with Intel, the long-time leader in the CPU market, by offering superior products and capitalizing on Intel’s missteps. Now, AMD has set its sights on another dominant player – Nvidia, the leader in AI chips – with many seeing AMD as the most credible challenger to Nvidia’s reign.

On that front, Data Center revenue has certainly been growing at AMD. In its latest quarterly report, the company delivered record Data Center revenue of $2.8 billion, amounting to a 115% year-over-year increase. Overall revenue was up by 9% as the total figure landed at $5.84 billion, thereby beating Street expectations by $120 million. The company also posted a beat on the bottom-line, as adj. EPS of $0.69 edged ahead of consensus by $0.01.

Despite the strong report and AMD’s positioning in the AI space, there are doubts in some quarters regarding its ability to really give Nvidia a run for its money, while a lofty valuation is also seen as a concern to some.

Perhaps that’s why during Q2 Fisher slashed his AMD holdings by 20%, offloading 5,716,366 shares during the quarter.

Deutsche Bank analyst Ross Seymor, while applauding AMD’s performance, also shares reservations about its valuation.

“Despite rising investor concerns across a wide array of AMD’s business (MI300 cancellations, EPYC ramp timing, AI PC competition, Embedded muted, etc.), AMD delivered a solid revenue beat/raise, the largest in over a year,” Seymore, who ranks amongst the top 1% of Street stock experts, said. “Most importantly, AMD’s Data Center segment was the primary area of strength driven by both MI300 DC GPUs and DC CPUs… Overall, we applaud AMD’s strong execution in an otherwise choppy market… However, with little change to our estimates (~$5 in CY25), we continue to believe AMD’s shares are fairly valued,” Seymor opined.

All told, Seymore rates AMD stock as a Hold (i.e., Neutral), while his $150 price target implies shares will stay rangebound for the time being. (To watch Seymore’s track record, click here)

Most on the Street, however, takes a more upbeat view of AMD’s prospects. Based on 24 Buy recommendations vs. 6 Holds, the analyst consensus rates the stock a Strong Buy. Going by the $189.88 average price target, a year from now, shares will deliver returns of ~28%. (See AMD stock forecast)

Intel

While AMD’s fortunes have trended upwards over the past decade, Intel’s fortunes almost act as a mirror image. This year’s price action has been particularly brutal, with the shares down by 58% on a year-to-date basis.

Intel’s decline can be attributed to several factors: delayed transitions to advanced chip manufacturing processes, losing its technological edge to competitors like AMD and TSMC, and struggling to innovate quickly enough in a rapidly evolving industry. These setbacks have led to the loss of market share in areas such as data centers and consumer PCs. Additionally, strategic missteps have further weakened Intel’s competitive position.

Although Intel’s recent foundry plan aims to position the company as a major player in semiconductor manufacturing, competing with giants like TSMC and Samsung, the business continues to face significant challenges in the interim.

This was clearly reflected in its latest quarterly results. In Q2, revenue fell by 0.9% year-over-year to $12.83 billion, falling short of analysts’ expectations by $150 million. Additionally, adjusted EPS of $0.02 missed the mark by $0.08. The guide was no better, with Intel forecasting revenue between $12.5 billion and $13.5 billion, well under the $14.39 billion expected on Wall Street.

So, it’s perhaps not surprising that Fisher decided to offload 460,471 INTC shares in Q2, slashing his holdings by 66%.

Bank of America analyst Vivek Arya also takes a dim view of Intel’s prospects, saying there’s “no quick or easy fix here.”

Citing the myriad issues at the chip company, Arya, who also ranks amongst the top 1% of Street stock pros, writes: “In our view 1) INTC’s IDM structure is just not equipped to simultaneously compete against focused and agile fabless (NVDA, AMD) and foundry (TSMC) rivals, 2) Lack of competitive AI accelerators continues to reduce relevance to critical cloud customers, 3) large-scale restructuring (15% headcount reductions, capex cuts) could create unintended competitive consequences, and 4) suspension of dividend could make stock less attractive to some investors.”

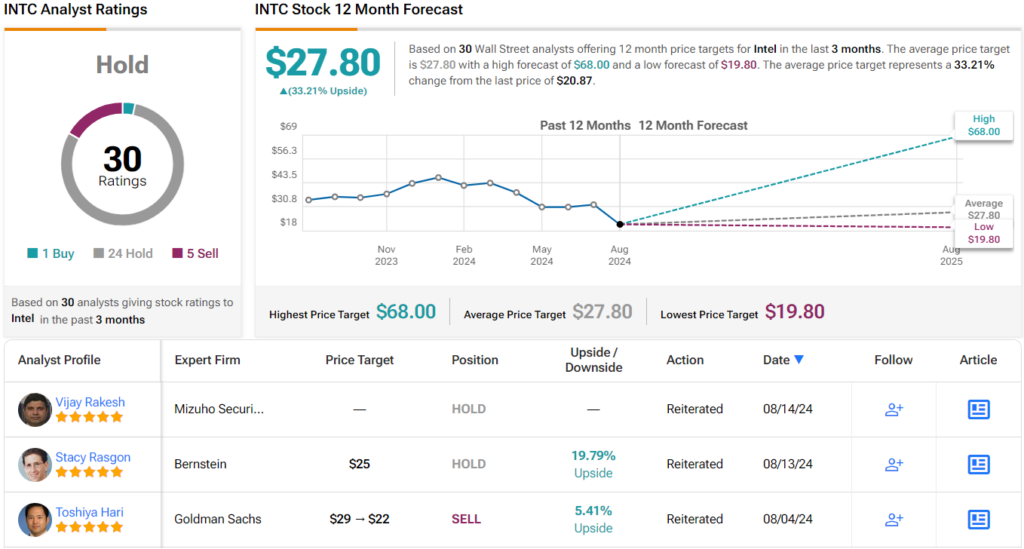

These comments underpin the 5-star analyst’s Underperform (i.e., Sell) rating on Intel shares, although his $23 price objective does make room for 12-month returns of 10%. (To watch Arya’s track record, click here)

Overall, the Street’s current assessment of Intel presents an interesting conundrum. On the one hand, the consensus view is that the stock is Hold (i.e. Neutral), based on 24 Hold recommendations, 5 Sells and just 1 Buy. However, considering how hard the shares have been hit, most seem to think they are now undervalued; as such, the $27.80 average price target suggests the stock will climb 33% higher over the next year. (See Intel stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.